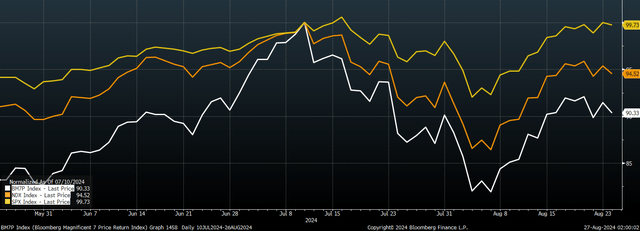

While the S&P500 is back to within a percent of its July 16 all-time high, there has been a stark change in leadership in the market since this peak, with mega cap tech stocks beginning to lead on the way down, as the chart below shows. This is a significant development and while Nvidia’s upcoming earnings release may breathe fresh air into the bubble, it appears to be starting to deflate. I continue to see market valuations as detached from long-term earnings potential as they have ever been, and expect at least a 50% market decline over the coming years as sentiment towards AI sours amid harsh economic realities.

Magnificent 7, NDX 100, and SPX, rebased to July peak (Bloomberg)

Every single reliable valuation metric for the US market puts it within a few percent of its most extreme level in history. Using a simple growth plus dividend yield approach, the current yield of 1.3% means that if dividends grow at the pace of nominal GDP of say 4%, investors can expect 5.3% annual returns relative to around 10% over the long term. For the S&P500 to be considered fair value from a historical returns’ perspective, the dividend yield would have to rise to 6%, requiring a 78% decline.

To many investors, US equity valuations are justified by the strong outlook for earnings growth, driven primarily by the productivity enhancements of Artificial Intelligence. The S&P500 has seen its PE ratio rise 10 points since the release of ChatGPT in November 2022 ignited a frenzy of interest in AI investments, and over half of this increase has been due to the multiple expansion among the magnificent 7 stocks. The earnings of these 7 stocks have grown to a spectacular 24% of total S&P500 earnings, and their market cap has grown to 31% of the market. Their combined market cap is now 9x total S&P500 earnings compared to 6.5x at the tech bubble peak in 1999.

Little Sign Of Significant Real-World Impact

While the AI boom has done a lot for equity valuations, in the almost two years since the release of ChatGPT, there has been very little in the way of results. S&P500 earnings including extraordinary items are actually down over the past two years, as are free cash flows. Even operating cash flows have gone nowhere over this period.

It is looking increasingly likely that a great deal of AI related capex over this period will turn out to be malinvestment as it becomes clear that while the technology is impressive, it may not always be economically viable. When a particularly impressive technological development gets the attention of Wall Street, demand from investors to see this technology adopted by businesses causes a surge in investment. Regardless of the investment case, companies have been encouraged to roll out AI infrastructure to avoid being left behind in the short-sighted race for speculative capital.

The most underappreciated threat facing the AI boom comes from the physical and human resource constraints. Regarding the former, according to this article a ChatGPT text search consumes 10 times the power of a Google search, while other research finds that generating an image using a GenAI model could take as much energy as half a smartphone charge. Regarding human resources, as far as I can tell, while the output of LLM models is often breathtakingly impressive and creative, it still needs to be proofed and fact-checked by capable humans. As these machines have no way of knowing the difference between fact and fiction, this problem is unlikely to go away, regardless of the amount of expensive inputs that are thrown at them.

While it is true that chatbots are increasingly being used by businesses and individuals as a smarter alternative to Google for answering a basic query, in my opinion, they are only marginally better at answering most queries and much worse at answering some. The Global Chatbot Market Size was valued at USD5.4bn in 2023 and is expected to reach USD42.8bn by 2033, according to a research report published by Spherical Insights & Consulting. This 2033 figure is barely higher than Netflix’s annual revenues, and pales in comparison to the tens of billions already invested in the technology.

The Bubble Is Reflected In Economic Imbalances

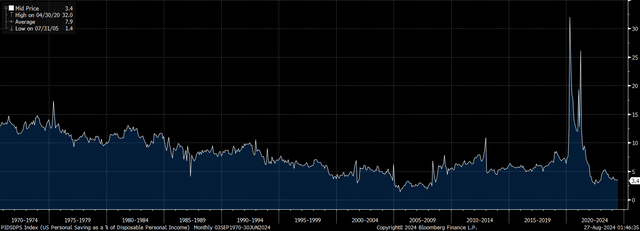

The inflation of the AI bubble has in part been driven by the fiscal deficit which, as I explain here, has created the illusion of abundant savings in the economy. By keeping tax rates low and spending high, consumers have been able to spend more of their wages than they otherwise would have, raising corporate profit margins. Even with the impact of the budget deficit, however, the consumer savings rate is close to the record lows seen at the peak of the housing bubble in 2006.

US Personal Savings Rate, % (Bloomberg)

There is a significant risk that we see a combined rise in the US personal savings rate and a rise in corporate tax rates, acting as a double negative on corporate profits and exposing the extent to which these profits were partly the result of huge and unsustainable economic imbalances. Indeed, presidential front-runner Kamala Harris has proposed raising the corporate tax rate to 28% from 21% currently, while any economic weakness could cause precautionary savings to surge.

What Could Go Right?

The main risk to my bearish view comes from renewed optimism over the impact of upcoming interest rate cuts. The Fed appears ready to delivery at least 100bps of cuts by year-end which seems aggressive given CPI is still at 2.9%, but 2-year breakeven inflation expectations sit at 1.7% and 5 year break evens are back on target at 2.0%, so there is no reason to think that the Fed is embarking on activist monetary policy that should force investors further out onto the risk curve. Monetary policy is objectively tight right now as it was at the 1999 and 2007 market peaks, and it is likely to get progressively looser over the coming years as it did follow these peaks. There is no reason to expect this to ease to have any beneficial impact on stock valuations. Another upside risk comes from the upcoming Nvidia earnings release, which could reignite speculative sentiment, but even a strong beat would shed little light on whether this demand is sustainable beyond the next few quarters.

While the direction of the stock market in the short term is anyone’s guess, the risk-reward outlook continues to deteriorate. For investors to generate even modest returns over the coming years, equity multiples will have to remain at current extremes or even continue to expand if earnings growth does not accelerate. I am often asked, what if I am wrong in my short conviction. My answer is: I will lose money, but I am safe in the knowledge that I am receiving net positive cash flows as interest on cash far exceeds the dividend on stocks and likely will continue to unless there is a sharp fall in valuations.

Read the full article here