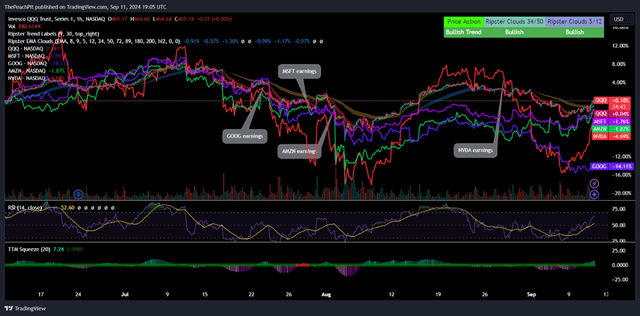

As the market becomes more volatile with the top names in the NASDAQ-100 (QQQ) experiencing a decline in post-CYq2’24 earnings, one has to ask whether it is time to begin considering shorting the market. Despite the immediate investor response, the top-tech names have only modestly recovered from their post-earnings declines. On top of this, economic data has been relatively mixed, with the rate of inflation growing 10bps less than the market expected at 2.5%. One of the biggest catalysts to come post-CYq2’24 earnings season is the Federal Reserve’s interest rate policy, which is expected to begin moving towards an easement. Despite the softening of CPI and the more challenging economic outlook, I believe that the Fed will hold rates steady on September 18, 2024. If this is the case, I believe the NASDAQ Index will react with significant volatility and may sour stock prices as a result. Given the economic outlook and the potential volatility that will follow, I believe investors will have the ability to take advantage of such moves through ProShares UltraPro Short QQQ ETF (NASDAQ:SQQQ). I recommend SQQQ with a conditional BUY rating, which will be explained in the mechanics of the strategy. SQQQ comes with a net expense ratio of 95bps.

TradingView

This report will contain two sections; the first will contain the basic mechanics of SQQQ and the second will entail my economic outlook.

Mechanics of SQQQ

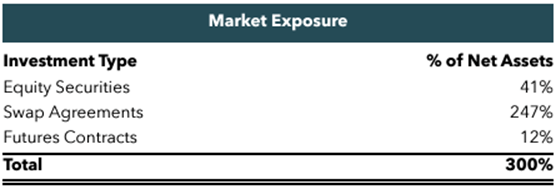

SQQQ is a leveraged portfolio that seeks to return 3x the inverse DAILY returns of the underlying NASDAQ Index (QQQ). Daily is emphasized because this portfolio strategy is meant to be held for no longer than a single day in order to achieve the mandated 3x targeted returns. This feature is executed through the ownership of equities, swap agreements, and futures contracts in order to reach the appropriate leverage to achieve the 3x target.

Corporate Reports

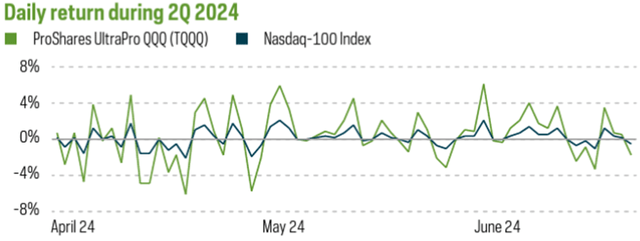

Because of the daily reset of the swaps and futures, holding this strategy for longer than a single day will not reflect a 3x return over the underlying index, especially during days of consecutive appreciation or depreciation and low or high volatility. Each of these factors will play a significant role in the strategy’s performance when held for a duration longer than a single day. During multiple days of a single-direction trend, SQQQ will result in a compounding effect that will provide investors with a higher or lower return than the 3x target.

Corporate Reports

Given the mechanics of the portfolio strategy, I cannot recommend investors hold this strategy for longer than a single day, especially given how resilient the NASDAQ has been given the challenging economic environment. Unless you believe that the underlying index may realize consecutive days of decline, I recommend utilizing this strategy for single-day use. For investors seeking a longer-term strategy, SQQQ may not be appropriate given the daily reset that may result in a compounding effect, especially during volatile markets. Other risks involved include counterparty risks relating to the swap and futures agreements, the use of treasuries and repo agreements, which may add additional liquidity risk, and interest rate risk as it relates to debt securities and the cost of carry.

It should be noted that SQQQ is inherently a high-risk investment strategy. For starters, the portfolio may not achieve the intended 3x target during times of high volatility. Being short an investment is also a high-risk strategy, especially when considering the historical growth trajectory of the underlying index. Though not probable, if the underlying index reaches a 33% gain, SQQQ may lose its entire value. In addition to this, holding SQQQ for longer than a day puts the investor at risk of value erosion as a result of the reset phenomenon.

For example, if the underlying is valued at $10 and drops to $9 the following day, only to return to $10 on the 3rd day, the daily rate of return would be -10% and +11%. When using the leveraged strategy, the investor’s value would decline to $7 and end up at $9 on the final day, short of the underlying value.

Basic Example

The index also holds significant concentration risk in the IT and communications sector, which is reflected in the SQQQ. In addition to this, the top 10 constituents command 49.79% of the portfolio weighting.

SQQQ trades at a relatively high volume, with an average 179mm shares changing hands daily. To reiterate, SQQQ is intended to be traded on a daily basis in order to achieve the 3x inverse target of QQQ performance. SQQQ can also be utilized as a hedge by investors seeking inverse exposure to the NASDAQ Index.

For more information relating to risks, please follow the links provided below:

The Lowdown on Leveraged and Inverse Exchange-Traded Products

Updated Investor Bulletin: Leveraged and Inverse ETFs

FINRA Reminds Firms of Sales Practice Obligations Relating to Leveraged and Inverse Exchange-Traded Funds

Economic Outlook

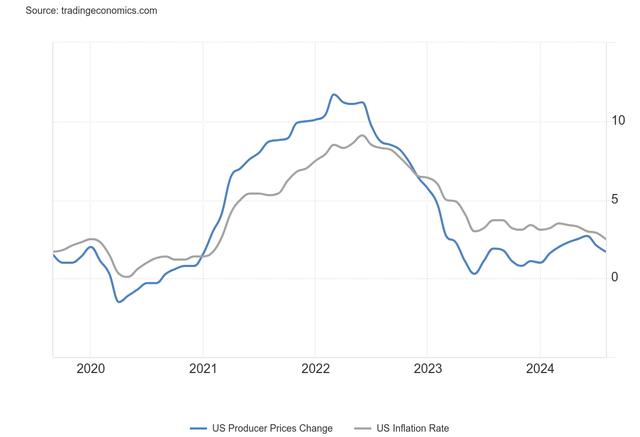

I have reason to believe that the broader economy is softening despite the slower rate of inflation. The recent inflation data came in mixed, with CPI coming in softer than expected at 2.5% year-over-year growth and PPI coming in hotter at 1.7% year-over-year growth.

TradingEconomics

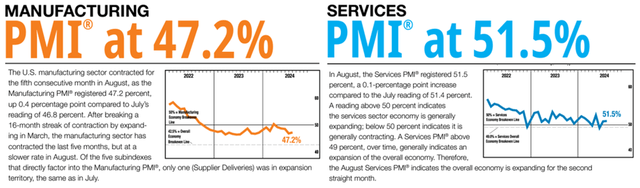

One of the factors that I’m keen on is the monthly ISM-PMI prints, which have told a story of potential future decline as a backlog of orders falls into contraction territory for both services and manufacturing.

ISM-PMI

Though manufacturing has remained in a contraction for a much longer duration, the services PMI has teetered into a broader contractionary state on two occasions in 2024 paired with softer expansions.

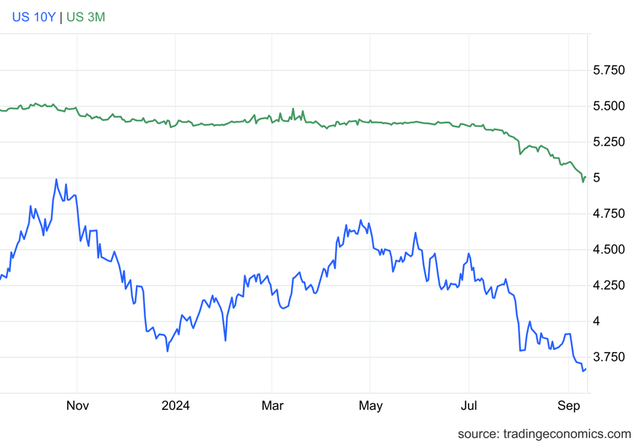

Considering a rate cut during the September 2024 Fed meeting, analysts are expecting 3 rate cuts at 25bps increments throughout the duration of 2024. This has weighed in heavily on the 3-month treasury, which has set the path to decline to 5%, down from around 5.5% this time last year.

TradingEconomics

Though I believe a rate cut is to come, I do not believe the Fed will make the decision to begin cutting come the September meeting, despite inflation easing to 2.5%. I believe that more economic pressure will be necessary before the Fed decides to ease up on interest rate policy. Don’t get me wrong, there are clear signs of the decline coming forth through the recent CYq2’24 earnings cycle; however, I do not expect enough economic decline has occurred to deem a rate cut necessary.

Health Of The Consumer

When considering one of the underlying drivers of GDP growth, consumer spending is taking a turn away from discretionary and more towards staples.

“The nature of spend is evolving, it’s going from discretionary to a more staple-type spend.”

Mark Mason, CFO of Citigroup

Though at the lower end of the curve, consumer spending has turned to rationing. Dollar General Corporation (DG) reported that their core consumers are feeling financially constrained. Though the store caters to the lower band of income, I believe that this tells a broader story of how inflation is challenging consumers’ budgets.

On the discretionary side of spending, PC sales remain challenged as consumers at the broader income bands ration spending. HP Inc. (HPQ) and Dell Technologies Inc. (DELL) each reported softer PC sales in CYq2’24 at the consumer level.

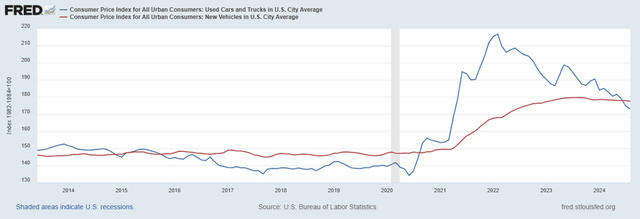

In addition to this, new and used vehicle prices are set declining. Though this is more prevalent in the used vehicle market, Mr. Jim Farley, President & CEO of Ford Motor Company (F) suggested that broader prices are set to decline by 2% in 2024. On top of this, electric vehicles are selling at an even more significant discount to move inventory.

FRED

Business Outlook

I believe one of the biggest driving factors in the economy is AI/ML applications. With companies like Palantir Technologies Inc. (PLTR) automating & optimizing business processes and eliminating redundant costs, I believe there is more room for margin improvement at the enterprise level. Though this may result in fewer headcount necessary to cover administrative tasks that can be automated, or in the case of Tesla, Inc.’s (TSLA) Optimus and the automation of factory floors, I anticipate that enterprises will have the opportunity to manage cash flow if the top line stagnates. This is already happening at CAVA Group, Inc. (CAVA) in optimizing ordering to reduce shrink. McDonald’s Corporation (MCD) is partnering with International Business Machines Corporation (IBM) to accelerate the development and deployment of its automated order-taking technology to manage the challenged same-store sales, as experienced in q2’24.

For the most part, AI adoption should benefit the top constituents in the NASDAQ Index, including the hyperscalers and chip designers. Where the cracks may derive is from broader economic hardship that may create an aggregate pull on the index. Given the investor reaction as seen post-earnings release for the hyperscalers and chip designers, I believe analysts may become more critical when forecasting growth trajectories as it pertains to data center growth and AI application adoption.

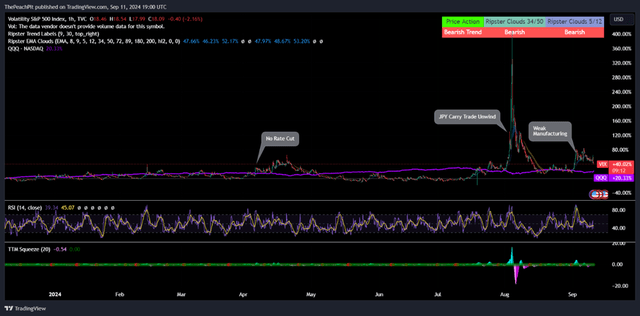

Given that we are coming up on a major economic catalyst, September 18, 2024, the day Jerome Powell will address interest rate policy, I believe there may be more in play than just directional decline. No matter Mr. Powell’s decision, I believe that the broader index will react with heightened volatility, opening up the market for traders to take advantage of the price swings.

TradingView

Lastly, US politics may play a major role in the direction of the broader market with the presidential election coming up on November 5, 2024. I’m not going to pretend to be a political expert and will not discern any opinion of either candidate. What I will mention is that volatility may heighten on election day, given the nature of how pivotal presidential elections are.

Conclusion

SQQQ is a leveraged investment product that targets a 3x inverse return to the underlying NASDAQ-100 Index. This product is meant to be traded on a daily basis in order to achieve the 3x target; however, longer holding periods can compound returns beyond the 3x target as a result of the daily reset. Given my outlook on the market and the economy, I believe SQQQ can make a strong investment candidate for those that hold similar views.

Read the full article here