Standard Chartered (OTCPK:SCBFF) represents an interesting investment opportunity in the global banking sector, in my view, particularly considering the bank’s strategic focus on high-growth regions like Asia, Africa, and the Middle East. Moreover, the thesis’ attractiveness is compounded by a robust capital position, as well as expanding profitability in wealth management and global banking. From a valuation perspective, I view shares as cheap, with equity trading at <10x P/E and ~0.6x P/B. Indeed, based on a residual earnings model, I estimate that Standard Chartered stock should be valued about ~40% higher.

For context, since the start of the year, Standard Chartered shares have slightly outperformed the broader market: YTD, Standard Chartered stock is up about 21%, compared to a gain of approximately 18% for the S&P 500 (SP500)

Seeking Alpha

Strong June Quarter…

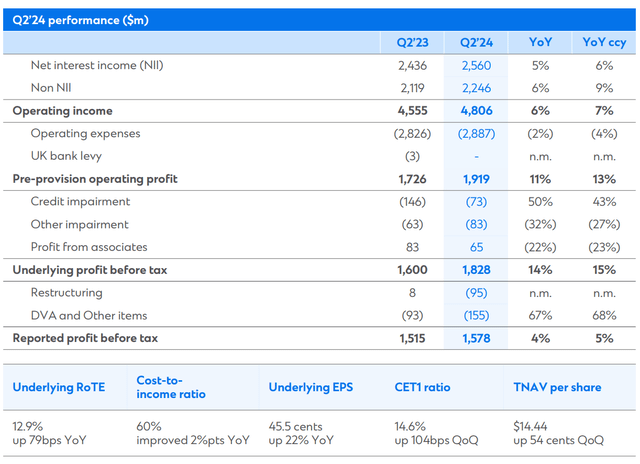

Standard Chartered’s Q2 2024 results highlight the bank’s strong financial performance and operational resilience, building on the solid momentum established in the first quarter. For the second quarter of 2024, Standard Chartered reported revenues of $4.8 billion, slightly lower than the $5.2 billion achieved in Q1 but representing a 6% YoY vs. the same period one year earlier. This brings the total revenue for the first half of 2024 to $10 billion, positioning the bank well to meet its full-year growth target.

Solid net interest income contributed notably to a strong Q2, with NII increasing by 6% QoQ with a corresponding rise in net interest margin by 17 basis points, 12 basis points above consensus expectations. On that note, the bank benefited from a positive mix effect due to Treasury optimization and the roll-off of a short-term hedge, which contributed an $84 million or 6 basis points QoQ boost to NII.

Standard Chartered Q2 2024 results Standard Chartered Q2 2024 results

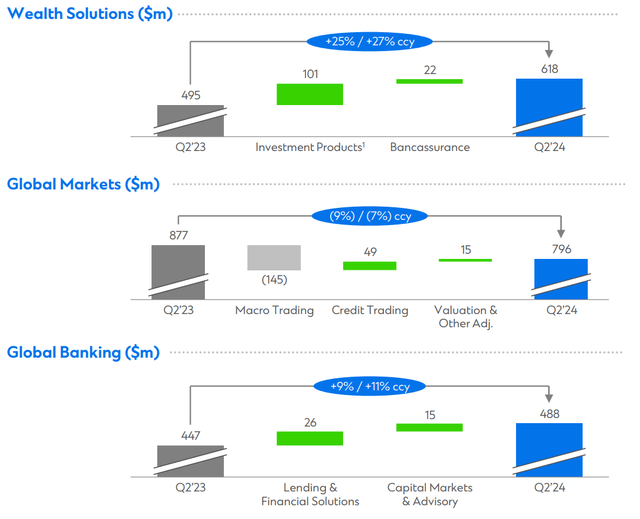

Within its business divisions, Wealth Management was a standout, achieving a 25% YoY increase in income, supported by strong growth in assets under management. Global Banking also performed well, with a 9% YoY revenue increase, while Global Markets revenue fell a bit by 9% YoY.

Standard Chartered Q2 2024 results

From a profitability standpoint, Standard Chartered continued to benefit from lower provisions and effective cost control measures: On the cost front, Standard Chartered demonstrated disciplined expense management with a modest 2% YoY increase in operating expenses, which contributed to positive operating leverage of 4%. The bank’s underlying profit before tax for Q2 2024 came in at $1.83 billion, which was 12% above consensus estimates. This strong performance was largely driven by lower credit impairments, which were 69% better than consensus expectations, reflecting sovereign credit upgrades and minimal impairments in the Corporate & Institutional Banking (CIB) division. Additionally, the Common Equity Tier 1 ratio improved to 14.6%, up 60 basis points from the previous quarter.

In my view, capital return to shareholders is the key metric that shows a bank’s investment value. And Standard Chartered shines bright in this regard: Indeed, with Q2 results, Standard Chartered announced a $1.5 billion share buyback (about ~5% of market cap), following $3.5 billion of payouts (dividends and buybacks, ~12% of market cap) for the trailing twelve months.

Growth Potential in Emerging Markets

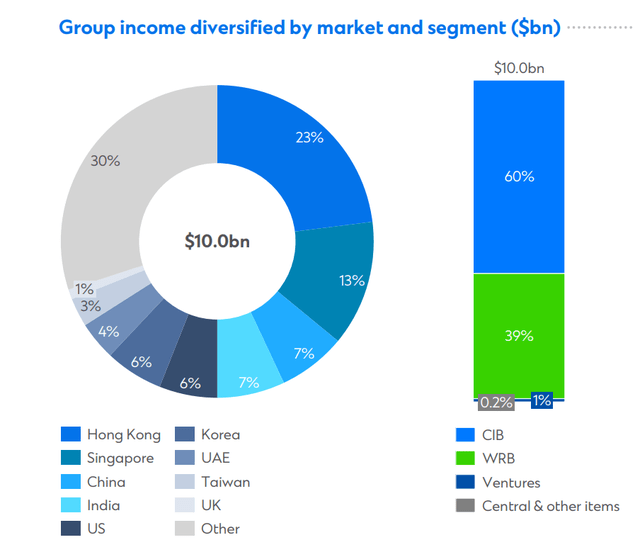

Looking beyond the Q2 print, I like StanChart’s presence in regions that present significant long-term growth opportunities. While its concentration in Asia, particularly Hong Kong (23% income exposure) and China (7% income exposure), has drawn some scrutiny due to current economic uncertainties, investors should note that Standard Chartered China exposure is mitigated by the bank’s presence in markets across SEA, Africa and the Middle East mitigates this exposure. In my view, as these “emerging market” regions are set to benefit from continued economic expansion, increasing financial inclusion, and rising urbanization, StanChart is well-positioned to capture economic value for shareholders. From a product perspective, I like StanChart’s potential through its thriving wealth management segment (~40% of income) where income surged 25% YoY in H1 2024, driven by rising assets under management and strong deposit inflows, particularly in markets like Hong Kong. This growth is partly due to a shift in savings preferences, as customers move away from Chinese property investments toward more diversified financial products. Even with concerns around its market exposure, this pivot toward higher-margin, fee-based income lines ensures a steady revenue stream that is less sensitive to short-term interest rate fluctuations.

Standard Chartered Q2 2024 results

Valuation: Set TP At $14.2 Per Share

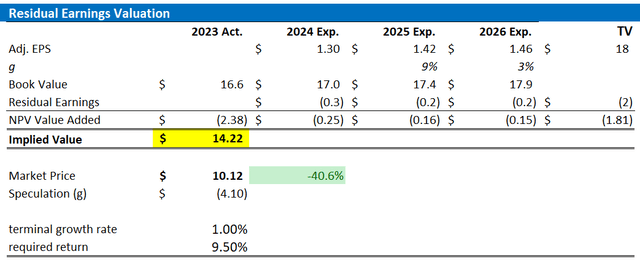

For Standard Chartered, I propose using the residual earnings valuation framework, which, I believe, is well-suited for valuing mature businesses – such as banks. That said, I have structured my valuation framework based on the consensus analyst forecasts for EPS through 2026, a cost of equity of 9.5%, and a terminal value growth rate of around 1%. Notably, the assumption of a one percent terminal growth rate is intentionally conservative, reflecting a prudent approach given the competitive uncertainties in the banking sector, as well as rate dynamics. Under these assumptions, my valuation points to a fair share price of $14.2, suggesting an upside potential of approximately 40%, based on accounting fundamentals.

Refintiv; Company Financials; Analyst Consensus; Author’s Calculation

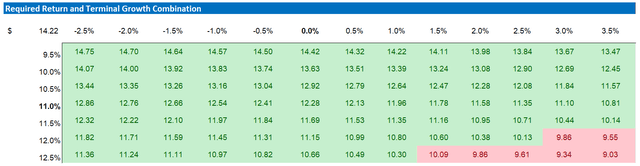

For investors seeking to explore a different perspective on rates, I have also included a sensitivity analysis that evaluates various combinations of cost of equity and terminal value growth rates. In this analysis, red cells indicate scenarios where Standard Chartered is overvalued, while green cells denote situations where the stock is undervalued relative to its current market valuation. Notably, every combination tested points to the stock being undervalued under all scenarios.

Refintiv; Company Financials; Analyst Consensus; Author’s Calculation

Investor Takeaway

Standard Chartered offers a compelling investment case, underpinned by its strong growth potential in high-growth regions, robust financial position, and diversified income streams. The market’s concerns, primarily focused on its exposure to specific markets and interest rate fluctuations, are mitigated by a diversified income portfolio – both on geography and product. From a valuation standpoint, I consider Standard Chartered’s shares to be undervalued, currently trading at less than 10 times earnings (P/E) and approximately 0.6 times book value (P/B). In fact, using a residual earnings model, I estimate that the stock is worth around 40% more than its current price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here