Investment Thesis

Stitch Fix (NASDAQ:SFIX) delivered a surprise earnings report, which saw its stock jump more than 20% premarket.

Investors who had long ago abandoned this name will now be eager to bid it higher in the hope that this fallen stock has been unjustifiably beaten down.

Here, I highlight the bearish argument, that the business’ growth rates paint a picture of a dying business. And then, I progress to remark on the positive aspects of the thesis, namely, that Stitch Fix holds a lot of cash and no debt.

Previously, I was openly bearish on the name. And while I maintain that this stock remains very risky, I recognize that this stock, at this valuation, could see dramatic short-squeezes. Therefore, I’m upwards revising my rating to a hold, even if I remain firmly on the sidelines here.

Rapid Recap

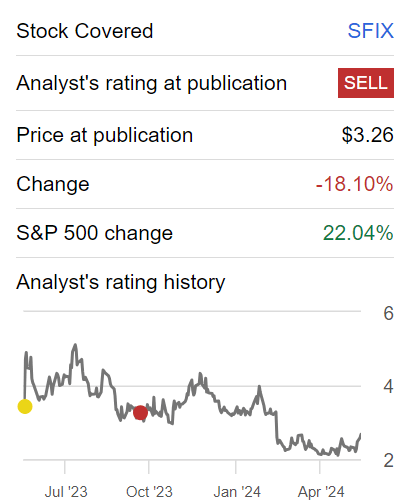

Back in October, I wrote a bearish analysis on Stitch Fix where I said:

The bull case is this, Stitch Fix’s objective is to assist clients in finding fashion choices that align with their unique styles and lifestyles.

However, as we move beyond its narrative, I find little reason to get bullish on this stock.

Author’s work on SFIX

Since that time, the stock is down 18%, while the S&P500 is up more than 20%. In other words, despite a very strong tide that lifts all boats, SFIX has been left behind.

Stitch Fix’s Near-Term Prospects

Stitch Fix is a retail company that combines personalized styling with data science to deliver curated fashion experiences to its clients.

By leveraging client data, Stitch Fix provides tailored recommendations, aiming to meet individual style preferences and fit requirements.

Stitch Fix’s near-term prospects appear fair due to its strategic focus on reimagining the client experience.

Recent changes, such as optimizing the Quick Fix service and refining pricing strategies, have already shown positive results, like a 25% increase in Quick Fix order value.

Also, the deployment of improved inventory management has enhanced the effectiveness of buying decisions, leading to better inventory productivity.

However, it’s not all positive. For one, Stitch Fix faces significant headwinds, particularly in acquiring new clients. Despite efforts to optimize marketing channels and improve conversion metrics, the company continues to struggle with a declining active client base, which decreased by 20% y/y. These are not small losses we are talking about here.

Moreover, the company’s newly found reliance on AI, doesn’t come for free and requires substantial investment.

Given that background, let’s now discuss its fundamentals.

Stitch Fix’s Outlook Improves, Slightly

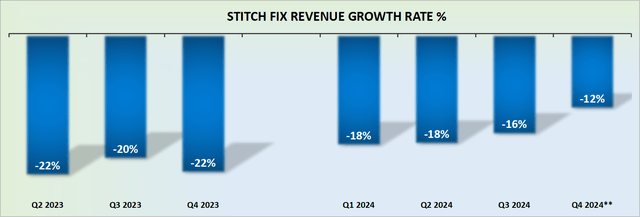

SFIX revenue growth rates

The graphic above should drive home what investors are eyeing up. Investors are looking at a company that has consistently delivered negative y/y growth rates for 8 consecutive quarters (data now shown), while its outlook for the next quarter is once again expected to be negative. More specifically, taking the high end of its guidance, Stitch Fix’s revenues will come in around negative 12% y/y revenue growth rates next quarter, fiscal Q4 2024.

This is not a viable business. This is a business, that is struggling. Pure and simple. And the only reason why its growth rates next year could possibly be even less bleak is simply that the bulk of its strong business has already been lost. Now, Stitch Fix operates as a shadow of its former self. This is a high-risk investment. Given that context, let’s now discuss the bull case.

SFIX Stock Valuation – 12x This Year’s EBITDA

I believe that SFIX is fairly valued. And here’s why.

As it stands right now, including the premarket jump, Stitch Fix’s market cap stands at approximately $350 million. However, nearly 70% of this market cap is made up of cash.

More precisely, Stitch Fix’s balance sheet holds about $245 million of cash and cash equivalents and no debt. Let that sink in. That’s a lot of cash. But that cash is only worth anything, if management does the right thing with that cash.

And this is where this bull case gets more complicated. Stitch Fix is ruthlessly cutting back on its cost structure. Consequently, this has allowed Stitch Fix to guide to as much as $30 million of EBITDA this year. On the surface, this sounds terrific.

Up until last quarter, Stitch Fix’s fiscal year 2024 was expected to deliver around $20 million of EBITDA at the high end. The fact that within 90 days of that report, Stitch was able to meaningfully improve its EBITDA guidance to as much as $30 million at the high end, gives investors hope that the worst of its prospects are now in the rearview mirror.

That, at its core, is the bull case. Nevertheless, I question whether paying up for Stitch Fix truly makes sense. After all, a business can only cut back on its costs so far. After a while, it must start to deliver some growth to support its operations, and bottom-line profitability.

Hence, paying around 12x EBITDA for a business that is made up of 70% cash, and no debt, sounds pretty awesome. This means that on an EV to EBITDA metric, the stock is cheaper than 4x EBITDA.

But there again, this all depends on whether management is able to stabilize its topline.

The Bottom Line

In summary, Stitch Fix’s financial outlook is a mixed bag, prompting a cautious stance on its valuation. While the company boasts a significant cash reserve and has managed to improve its EBITDA guidance, concerns linger over its declining customer base and persistently negative revenue growth rates.

Despite recent cost-cutting efforts and improved profitability projections, the sustainability of Stitch Fix’s business model is extremely uncertain, especially given its inability to reverse the trend of losing customers.

With the market’s recent optimism reflected in the stock’s premarket jump, investors should carefully assess whether paying up for Stitch Fix truly makes sense. For me, I’m sticking firmly to the sidelines, as I know there are easier investments elsewhere.

Read the full article here