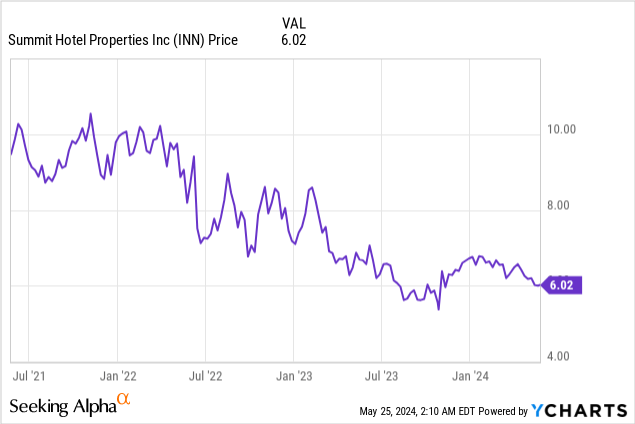

Introduction

I like preferred shares as a portion of my fixed income portfolio and I am keeping my fingers on the pulse of a lot of different issuers and preferred shares to make sure there are no unexpected surprises. I own both series of preferred shares issued by Summit Hotel Properties (NYSE:INN) and as the hotel sector isn’t always the most reliable sector I am following the preferred shares I own in this sector a bit closer than other issues to ensure there are no coverage issues and/or balance sheet issues.

A decent start of 2024 with a relatively strong FFO and AFFO result

When looking at REITs the net income or net loss isn’t very relevant as the FFO and AFFO are more important metrics to determine how well (or poor) a REIT is doing.

INN Investor Relations

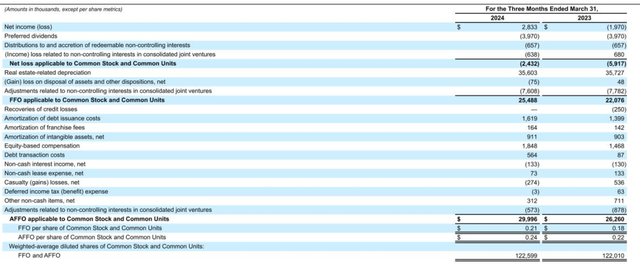

As you can see below, the starting point of the FFO and AFFO calculation was the $2.8M in net profit. After deducting the preferred dividends as well as the distributions to and items related to non-controlling interests, the net loss attributable to the common shareholders was approximately $2.4M. However, as the depreciation and amortization expenses tend to have a major impact on the net income but don’t necessarily represent a decrease to the fair value of the underlying assets, the FFO calculation takes these changes into consideration and looks at the underlying result excluding the depreciation and amortization expenses. After adding the depreciation expenses back to the equation and deducting about $7.7M in other elements, the FFO was $25.5M in the first quarter of the year.

INN Investor Relations

As the image above also shows, the total AFFO was just under $30M as there were a few additional adjustments. Keep in mind the AFFO does not include capital expenditures in the United States. The cash flow statement shows the REIT spent just over $18M on capital expenditures, which is in line with the full-year guidance to spend $65-85M.

INN Investor Relations

This means the AFFO adjusted for capital expenditures was approximately $12M. That being said, there are two important things to keep in mind. First of all, the starting point of almost $30M in AFFO already includes the full impact of the preferred dividend payments. The post-capex but pre-preferred dividend AFFO was approximately $16M which means the payout ratio was approximately 25%.

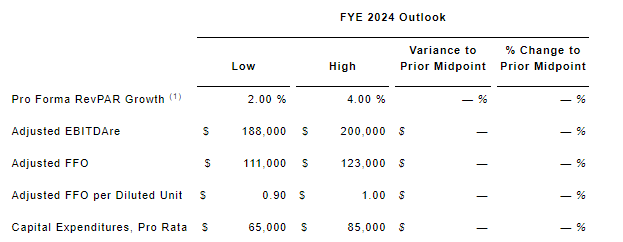

Secondly, seasonality plays an important role. The full-year guidance above also indicates an anticipated full-year AFFO of $111-123M. If I would use the midpoint of $117M and the anticipated capex of $75M, the adjusted AFFO would come in at around $42M, after already taking the $16M in preferred dividends into account. So while the preferred dividend coverage ratio is very strong based on the reported AFFO, it remains relatively strong after also deducting the capital expenditures.

Those capital expenditures obviously also serve a purpose: it helps to retain and boost the fair value of the assets. And that’s important to protect the asset coverage ratio of the preferred shares.

INN Investor Relations

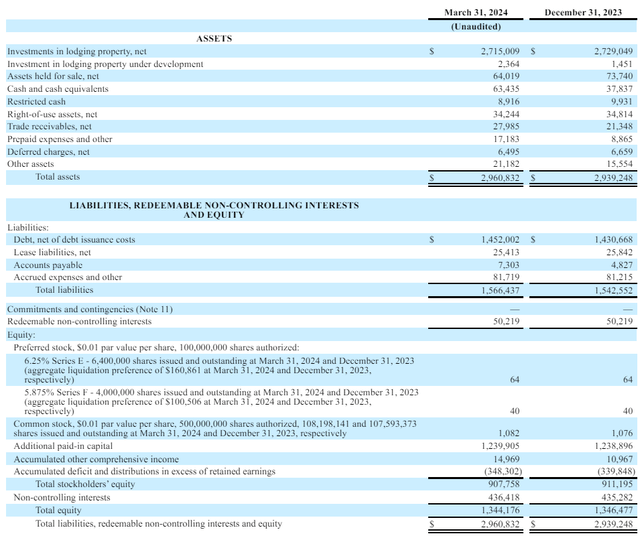

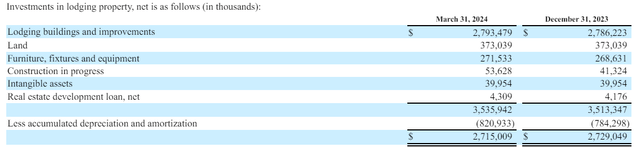

As you can see in the image above, the book value of the assets was $2.72B (excluding the assets held for sale) while the REIT had $63M in cash. This means the net debt was $1.39B, and approximately $1.31B after taking the $84M in proceeds from the sale of two hotels into consideration.

This indicates the LTV ratio is approximately 48.2% based on the book value of the assets, but keep in mind the $2.72B in book value already takes a very considerable amount of accumulated depreciation and amortization expenses into account.

INN Investor Relations

$821M in accumulated depreciation, to be precise. If I would use the acquisition value of the buildings, construction in progress and land of $3.22B into account, the pro forma LTV ratio would be just over 40% which is a very acceptable metric. Considering the book value of the two hotels that have been sold for $84M was just $64M, I have little doubt the fair value exceeds the book value.

That is also important to make sure the preferred shares enjoy a good asset coverage ratio. At the end of the first quarter the total equity value attributable to the shareholders of Summit Hotel Properties on the balance sheet was approximately $908M. We know there are 10.4M preferred shares outstanding for a total of $260M in preferred equity. This means there is in excess of $640M in common equity that ranks junior to the preferred shares. While that already is a decent buffer, let’s not forget this is based on the book value rather than the fair value. If I would use the acquisition cost for the buildings, land and the construction in progress, the ‘common equity cushion’ would be even more comfortable.

I own both series of preferred shares

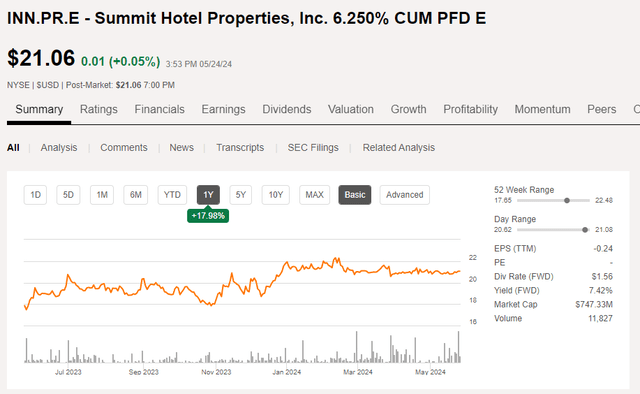

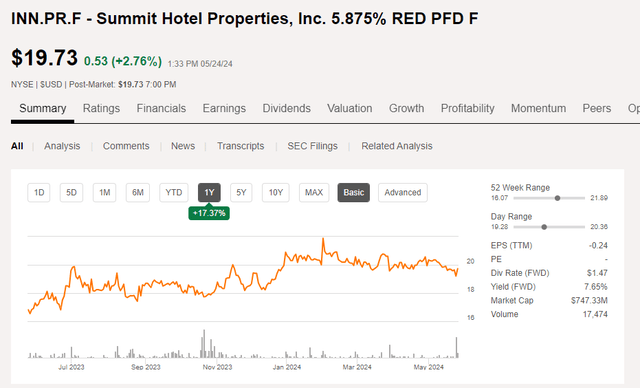

Summit Hotel Properties currently has two publicly traded preferred shares outstanding. As explained in a previous article, it issued 6.4M preferred shares series E (NYSE:INN.PR.E) while there are an additional 4 million preferred shares issued as a Series F (NYSE:INN.PR.F). The E-Series pays $1.5625 per share per year in equal quarterly installments and can be called anytime, while the F-shares can only be called from August 2026 on. The preferred dividend payable on the F-shares is $1.46875 per share, also payable in four equal quarterly payments.

The Series E closed on Friday at $21.06 for a yield of 7.46%.

Seeking Alpha

Meanwhile the Series F preferred shares closed at $19.73 for a yield of 7.44%.

Seeking Alpha

This means it doesn’t really matter which issue of the preferred shares you are buying as the yields are very similar. As both series of preferred shares have the same rights, an investor should always pick the one with the highest yield. The Series E has a slightly higher chance of getting called but as the preferred equity is costing the REIT just 6.25% per year – which is pretty cheap for perpetual equity capital – I don’t expect any of the issues to be called anytime soon.

Both issues are cumulative in nature, and offer protection should a change of control event happen. If the preferred shares are not redeemed upon a change of control event, preferred shareholders are entitled to convert their preferred shares into common shares.

Investment thesis

Is a 7.4% preferred dividend yield the highest yield in the sector? No, and I recently finally started to buy more of Chatham Lodging Trust’s (CLDT) preferred shares which currently yield approximately 7.8%.

That being said, I wouldn’t mind adding to my Summit Hotel Properties on weakness as I do believe the preferred shares offer good value. The common shares could potentially be interesting as well. Not necessarily based on the earnings result (the AFFO per share after capex will likely be just $0.35-0.40 per share) but the current book value per share is approximately $6/share while applying the fair value of the assets would add a few dollars to the pro forma book value of the shares.

I currently have a long position in both series of Summit Hotel Properties’ preferred shares, but I have no position in its common shares.

Read the full article here