The weak Dell Technologies Inc. (DELL) earnings were a huge red flag for Super Micro (NASDAQ:SMCI). The company has ridden the wave for AI server infrastructure demand, but the market is highly competitive with limited margins. My investment thesis is still Neutral on the stock due to relative valuation, but investors should watch out for a downturn, especially if the recent trading around $750 doesn’t hold.

Source: Finviz

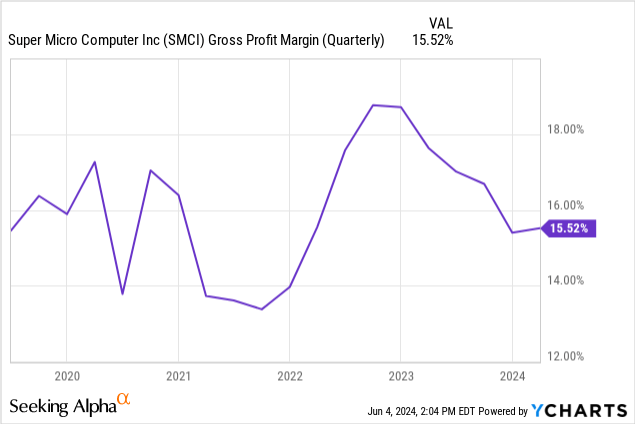

Margin Pressures

Super Micro has a very bullish story of surging AI server demand and customers willing to pay a premium price for direct liquid cooling technology. The only problem is that gross margins are headed lower in an indication of a highly competitive market, with a competitor like Dell possibly lacking access to Nvidia (NVDA) GPUs to effectively compete initially.

Dell Technologies CFO Yvonne McGill said this regarding margins on the FQ1’25 earnings call:

Given inflationary input costs, the competitive environment, and a higher mix of AI-optimized servers, we expect our gross margin rate to decline roughly 150 basis points

The COO highlighted the surging AI-optimized server order and pipeline scenario for a company with limited sales in 2023:

In ISG, our AI-optimized servers orders increased to $2.6 billion, with shipments up more than 100% sequentially to $1.7 billion. We have now shipped more than $3 billion of AI servers over the last three quarters. Our AI server backlog is $3.8 billion, growing sequentially by approximately $900 million. Our AI optimized server pipeline grew quarter-over-quarter again and remains a multiple of our backlog.

Similar to Super Micro, Dell has a huge server backlog estimated at $3.8 billion, but the company saw notable dips in gross margins. Back on the FQ1’25 earnings call for Dell, Bernstein analyst Toni Sacconaghi called out the margin issues as follows:

So really the only thing that changed was you added $1.7 billion in AI servers, and operating profit was flat. So does that suggest that operating margins for AI servers were effectively zero?

The biggest worry with Super Micro has been the margin pressures on the business. The rack servers the company sells don’t appear to have a massive moat, and customers don’t seem interested in paying up after already unloading so much cash for the Nvidia GPUs.

At Dell Technologies World, Dell announced plans for liquid cooled Blackwell servers soon after the Nvidia announcement. The Dell PowerEdge XE9680L server with liquid cooling and eight Nvidia Blackwell Tensor Core GPUs was highlighted as the industry’s densest, most energy-efficient rack-scale solution for large Blackwell GPU deployments. Jensen Huang was present at the conference, reinforcing the claim.

At the J.P. Morgan Technology and Media conference, Super Micro CFO David Weigand again confirmed the move to buy business with lower margins:

Well, we’ve liquid cooling was an opportunity for us to take an early lead. And so we mentioned that we’re going to be shipping 1,000 racks of liquid cooling liquid cooled solutions. So we think that we wanted to establish a beachhead and then build in and out at our customer site. So we think that we will opportunistically take lower margins, but it’s only so that we can attract more customers and more and more design wins.

Lower Margin Impact

Super Micro has a corporate target for gross margins in the 14% to 17% range, while Dell only targets 11% to 14% gross margins in the server group. The company originally saw margins jump for the big ramp in AI optimized servers, but the number is now starting to slump along with AI server sales by Dell.

The guidance for the June quarter would suggest a dip below the long-term target of 14%. Super Micro continues to maintain the goal with lower margins to grab initial market share with the liquid cooled racks, but a market leading and defining product should’ve been able to grab higher margins.

Super Micro only spends 4% on operating expenses, leading to very limited spending on any technology upgrade or operating efficiency to provide a long-term moat. The company has only 11% operating margins, and a dip below 14% gross margins will provide a large headwind to profits in 2024.

The gross profit impact on lower margins quickly hits EPS. Each 10 basis points of gross margin at $5 billion in quarter sales impacts gross profits by $5 million, leading to a $50 million impact for 1 full percentage point dip in gross margins.

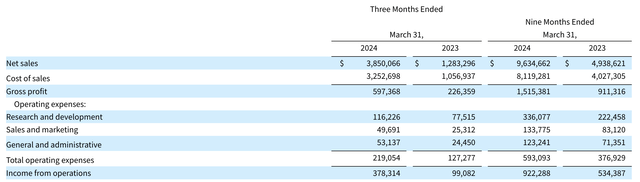

Super Micro guided to a roughly $8 EPS for Q2 with limited tax impacts, leading to ~$520 million in net income. At 14% gross margins, the company would produce only $728 million in gross profits, suggesting ~$208 million in operating expenses.

The company had about $219 million in opex in the prior quarter and just $166 million when excluding stock-based compensation. The R&D costs were just $116 million in the last quarter and $81 million after excluding SBC.

Source: Super Micro Q1’24 earnings release

As noted, Super Micro has limited profits and margin pressures could become a big issue and fast. Dell is aggressively ramping up sales of AI servers, with signs the tech giant is offering such servers at minimal positive margins.

Super Micro isn’t necessarily an expensive stock, trading at just 23x FY25 (June) EPS targets. The concern is that a push to gross margins of only 13% reduces the EPS by at least 10% due to the $50 million impact on gross profits for a company with just $520 million in forecasted net income and limited opex to juggle.

Takeaway

The key investor takeaway is that Super Micro doesn’t appear to have any large moat in AI servers. The company is facing rather large margin pressure when promoting a concept of having leading liquid cooling technology, leading to a 40% energy savings.

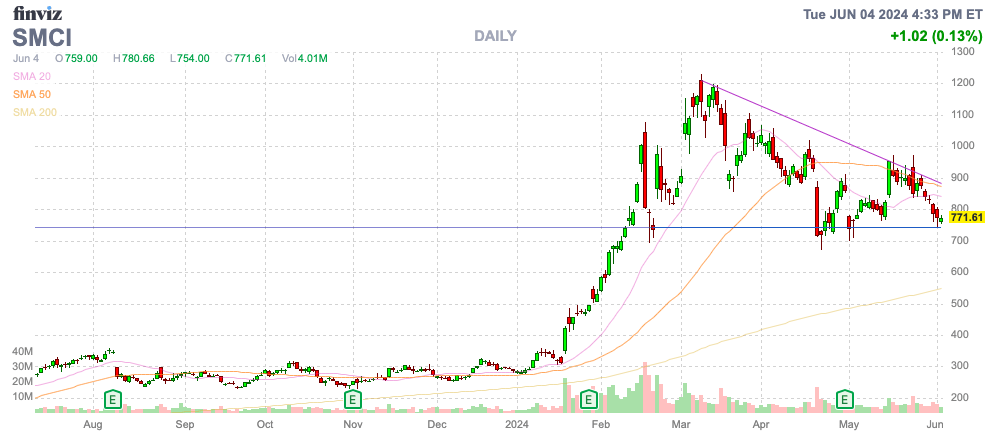

The stock just isn’t exciting here, with a real lack of AI leadership and signs a larger competitor is trying to take share with pricing. Investors must watch out below for any dip of the stock below $750.

Read the full article here