Suzano (NYSE:SUZ) has been seeing pressures on EBITDA in line with expectations from following the pulp price data. We see a new inflection upwards that gives us some immediate confidence in the coming results. But much more importantly (as focused on in our previous coverage), we see that Suzano is starting production at the Cerrado facility which should increase production of pulp by around 25%, and contribute more than that to underlying EBITDA as Cerrado’s per ton cash costs should be considerably lower than Suzano’s current average. This will suddenly come into effect starting in the coming quarter, and the impact should be very noticeable on increasing EBITDA particularly towards the end of 2024, maybe by Q3. Despite this clear growth angle for the business, at the tail end of major CAPEX already outlaid, the stock price is trailing back to the low side of trading ranges. The only concerns on our mind are of course the inherent cyclicality of the business, with the last couple of years breaking normal rhythms due to supply chain disruptions globally, and the fact that the new capacity from the Cerrado facility could actually globally affect prices as Suzano is a major producer. Then there is the perennial but still remote ESG concern that the eucalyptus that they are using at their Cerrado facility, currently not in the rainforest, may one day encroach on the rainforest if demand for pulp rises too quickly. We do not think that ESG concerns are a legitimate source of any discount at this point in time. In all, at a 9x TTM PE, Suzano is very cheap considering its economic profile and imminent incoming growth in operating results that we believe will accelerate debt repayment and support dividend growth.

Latest Earnings

We’ve been covering Suzano for some time now. The business is very simple. They produce pulp, and due to their location in Brazil, they do so at some of the lowest costs in the world. For industrial plays, low cost assets are the most important moat. Suzano is the global leader in this regard. Pulp is used as an input for paper and cardboard production, as well as tissues and other pulp based consumer staples. There is a secular angle that plastic will be replaced by paper products which underlies demand as a megatrend. Suzano is upstream in the value chain so it’s not obvious for them day to day, especially as the shift to paper-based rather than plastic-based products is punctuated and uneven, but it still is a positive force for Suzano in the long-term.

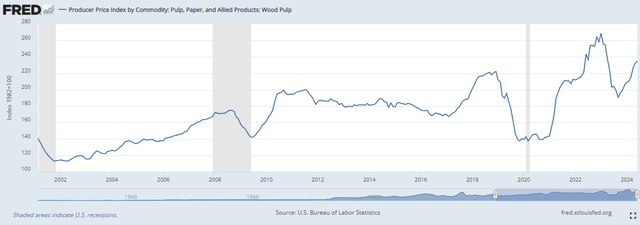

Pulp prices are quite easily tracked, for example with the FRED data. This gives quite a bit of visibility for how earnings of Suzano will end up looking quarter to quarter.

Wood Pulp Price (FRED)

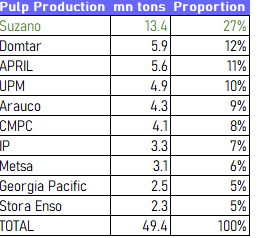

Pulp prices rocketed with the COVID-19 spurred goods boom, but have also stayed high for some time after that due to the general supply chain disruptions in global markets, and the very substantial reliance of pulp producers in Europe on Russian timber. This has meant that even after the turnaround in the goods boom of 2021-2022 pulp prices were also strong in 2023. While Europeans talked big on sanctions, it was ultimately the Russians who themselves retaliated and eliminated export of Russian timber to the Baltic and other European nations that used their timber as a fiber source. Suzano has an advantage in that Brazil is politically non-aligned and will sell to and source from almost anyone, and Suzano would also not need Russian timber since they have massive amounts of their own. Where Suzano already had the lowest cost assets, the geopolitical environment grows the divide and helps ensure their advantage secularly. In fact, some competitors have been closing down plants, both before and after the Ukraine invasion, due to their inability to compete. Their production, including Cerrado volumes, as well as related market shares can be found below.

Market Shares (Statista, VTS)

While competitors would be struggling, Suzano is expanding production and share, now at 27% of the global pulp production, and should also be benefiting from growing EBITDA sequentially just on account of the wood pulp price evolutions since last quarter close.

EBITDA (Q1 Pres)

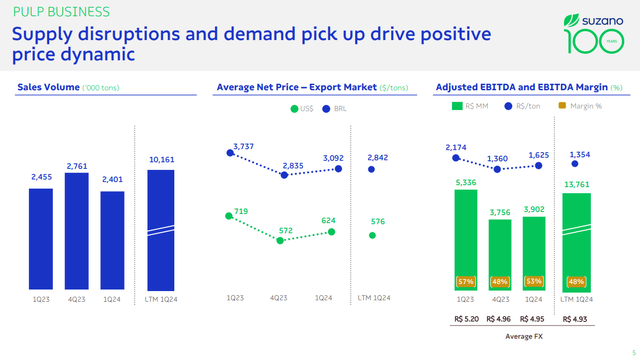

Since the close of the last books, net prices will have increased. Average prices are below marginal prices as of the latest earnings disclosures, and in the coming quarter we should see price realization considerably ahead of the latest quarter’s levels based on the FRED data. Sequential growth should be expected, even if prices of pulp are still lower YoY. Suzano will also start benefiting from Cerrado volumes starting in the coming quarter.

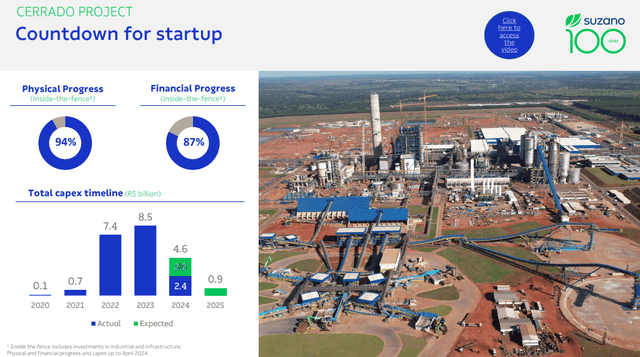

Half of the CAPEX for 2024 has been disbursed as of April for the Cerrado project, with the remaining 2.2 billion BRL to be paid out in the remaining 8 months of the year. Production there has just started a day or two ago.

Moving to the next slide, we are focused on the final sprint of the Cerrado project, which has already reached 94% physical completion and 87% of physical execution by April. The project’s CapEx guidance for 2024 is maintained at R$4.6 billion, with more than half having already been disbursement by April, therefore reducing cash flow consumption in the remaining eight months of the year.

Aires Galhardo, Executive of the Pulp Operations in Q1 Earnings Call

Besides growing production by around 25%, Cerrado will also reduce average cash costs. Cash costs should be reduced by around 5% structurally for the business on average, as Cerrado’s cash costs will be around 30% lower than that of Suzano’s pre-existing facilities located elsewhere (500 cash cost per ton vs 700 cash cost per ton for Suzano pre-Cerrado on a normalized, structural basis). One of the main reasons for Cerrado’s low cash costs for pulp production is proximity to the eucalyptus forests that border the Amazon Rainforest that will be the source of fiber.

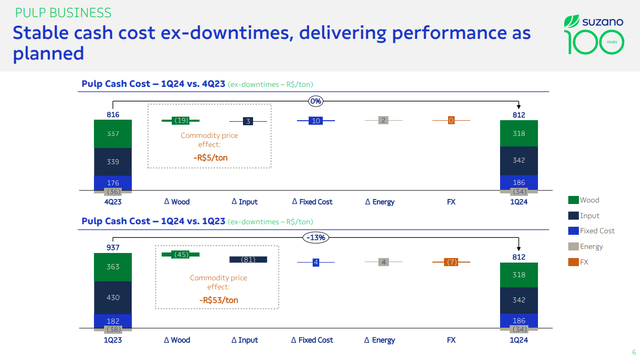

On the cost side it also helps that the abundance of wood, but also the fallen commodity chemicals prices, are reducing cash costs by around 13% YoY. Sequentially cash costs are flat supporting the case for significant sequential EBITDA growth.

Cash costs down (Q1 Pres)

Valuation and Forecasts

At the same average prices of last year, sales on run-rates would be increasing 25% in line with production increases. Analyst average estimates are for a 15% increase in sales for 2024, with Cerrado beginning operations now, which is consistent with a view that prices will still be quite strong in 2024, similar to in 2023. This is not a crazy assumption with the upticks being seen now in Chinese pulp import prices, despite Cerrado capacity additions to global supply.

2024 will not be a full year of Cerrado being fully operational; therefore, base effects will help in 2025 to support more EBITDA growth achievement.

Costs for the overall business are going down by around 5% based on Cerrado’s lower per ton cash costs. At around 45% EBITDA margin before Cerrado, EBITDA margins should grow by 5%. Consequently, EBITDA growth could be as high as 25% in 2024 with more in store in 2025 which will have a full year of Cerrado.

Net income growth will catch up to the EBITDA growth once the debt sourced for funding Cerrado gets paid down and no longer requires interest. OpCF (operating cash flow) is 2.5 billion BRL in Q1 against around 12 billion BRL in net debt. Once exceptional CAPEXing for Cerrado is done, OpCF will be higher thanks to Cerrado’s addition to the mix and investment outflows falling. High underlying OpCF will start making a dent in that debt every quarter.

25% is the growth in run-rate EBITDA you get from a company whose TTM PE is 9x. Incorporating the outstanding CAPEX which will increase net debt by around 10% (net of that period’s cash generation), as well as the average rate situation in Brazil likely by the end of 2024, the forward PE for Suzano should be around 8.5x for 2024, which again is absolutely low for a growing business, starting investors off with around 12% in earnings yield.

In terms of EV/EBITDA, forward multiples for 2024 are around 5.6x. For a comment on relative valuation, there are no other pulp pureplays but UPM (OTCPK:UPMKF) could be used as a comp as it has a relevant pulp manufacturing business at around 30% of revenues. 10% of UPM is energy generation probably with 20% EBITDA margins based on Endesa (OTCPK:ELEZY) which also does nuclear, which means a European utility multiple of around 9.5x EV/EBITDA forward could be used to crudely unblend the multiple, as well as a multiple of a not-vertically-integrated pulp and paper product play like Essity (OTCPK:ETTYF) at 9.4x for the remaining business.

UPM’s overall multiple is 9.5x. Assuming that UPM’s pulp business has the same margins as Suzano’s (although it would be lower) and assuming the energy business is at around 20% EBITDA margins, the residual businesses probably have a multiple of around 9x based on UPM’s average forward EBITDA margin of 19% or so. Using a simple goal seek analysis tells us that the implied multiple for the pulp business is probably close to 10x within UPM, which is twice Suzano’s multiple rendering it considerably undervalued on a relative basis, which is not surprising when just looking at the low PE. The only good reason for that difference in valuation would be leverage (differences in tax jurisdictions would not explain it), where Suzano’s leverage multiple is 2.69x on a forward basis while UPM’s overall leverage is closer to 1x. That gap would close on deleveraging eliminating leverage as a reason for Suzano’s discount.

In addition to deleveraging, profit growth is a great way to get the stock price headed in the same direction. With the stock coming down despite imminent profit increases, the chances here look quite good for capital appreciation, and the margin of safety is high with the multiples for Suzano already being at low levels.

But more fundamentally, Suzano offers tangible return potential in that the company already reinitiated the dividend in advance of the falling CAPEX burden as Cerrado neared completion. The dividend started again last year. With a larger asset base, they’ll be able to start deleveraging again but at a quicker pace than before (of around 10% per quarter of the net debt), which was not possible while debts grew with the bulk of Cerrado CAPEX coming in last year and in 2022.

Cerrado progress (Q1 Pres)

Risks

Additionally, we looked further into other potential overhangs on the business. ESG and deforestation concerns were one of them, particularly with the left-wing Lula government in Brazil which may have made problems where right-wing Bolsonaro wouldn’t have. However, Suzano’s forestry practices are sustainable, and there’s been no sign of the Lula government coming after them with any sort of tax or other government action. Importantly, Cerrado will use eucalyptus, which is not grown on rainforest lands but in Atlantic forests outside of the Amazon Rainforest. There aren’t really any concerns here that we see imminently. The closer proximity to the forests with Cerrado also reduces petrol usage for transporting fiber sources to the pulp mills.

The other thing is that with Suzano being a major producer, the new Cerrado capacity could have downward pressure on prices, or limit the rise of pulp prices. China is quite a big factor in the global pulp market. In general, we’ve been seeing bottoming out of Chinese industrial activity in some of our coverage, and for pulp there has been the first sign of an inflection upwards in import prices to China. There are some upwards pressures from a slow but likely China recovery, so we are comfortable with what is implied by the average analyst estimates. Nonetheless, price pressure is possible – although some competitors have been closing pulp plants as they cannot achieve the low costs of Suzano. Supply may not grow too much.

Absent considerations around this specific change in global supply from Suzano’s own Cerrado, the industry is of course commoditized and generally cyclical. Macro declines would impact pulp prices.

There is also the matter of leverage. While comfortable at 2.69x according to us and in light of imminent cash generation from Cerrado and the large operating cash flows relative to net debt (B$2.5 bn OpCF to around B$12 bn ND), it is higher than some of the less commoditized pulp operations who also run larger paper and packaging businesses downstream.

Final Remarks

We are confident in long-term sources of demand in end markets such as tissue paper and of course for other paper products which are poised to secularly replace plastic, as paper can be produced sustainably as long as forestry practices are sustainable. Forests are very abundant. There are never really any problems with wood and fiber prices as supply is more than enough. Therefore, unless massive and sudden demand increases occur, which would also have positive effects on Suzano’s business, there should be no reason for sustainable forestry practices to be broken and for any concerns to appear on the sourcing side, ESG or financial.

We also note that while in an uneven way, important parts of the Chinese economy are seeing a bottoming in activity. Indeed, Chinese import pulp prices have started to rise again, which will support the overall global pulp price, even in the face of new capacity.

Other than Cerrado, there were also some announcements of facility investments that are a small consolation for the major International Paper (IP) acquisition not going through and no longer factoring into the story. $870 for 420k metric tonnes of paperboard production means $365 million in revenues from a newly acquired facility. EBITDA margin is probably around 13% based crudely on International Paper margins, so around $47 million in EBITDA, which is not much more than 1% of Suzano’s overall EBITDA expected in 2024. The $870 is the price per tonne of linerboard as of February. The acquisition was for $110 million. They also made a 230 million EUR investment in a supplier of cellulosic fibers. The contribution should be of similar and small scale to the paperboard production facility.

In sum, Cerrado is just about to start increasing quarterly production by 25% of run-rates, with incremental production happening at 30% lower unit costs. EBITDA will benefit meaningfully in 2024, and in 2025, which will be a full year of Cerrado in the mix, where 2024 only gets Cerrado’s contribution halfway through. You only pay a 9x PE multiple for that growth, or a little over 5x EV/EBITDA, which is half the implied multiples of peers. With the business being very high margin and cash generative (around 2.5 billion BRL in OpCF with debt at around 12 billion BRL as of the Q1), deleveraging should occur comfortably, and erase leverage as one possible reason for valuation differentials.

Deleveraging will be even more comfortable as margins rise, with Cerrado entering the mix. Interest is around 4 billion BRL every year starting from 2024, or almost 20% of EBITDA. That will go down as deleveraging occurs and see the net income growth eventually mirror operating profit growth. Suzano has already started flirting with being a dividend payer, which should grow as leverage falls and be a tangible return in case multiple expansion doesn’t occur. Growth at a reasonable price with tangible deleveraging, profit and dividend growth return angles makes Suzano a clear buy at these fallen prices, likely to be redressed by earnings direction and reduction in leverage.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Best Growth Idea investment competition, which runs through August 9. With cash prizes, this competition — open to all analysts — is one you don’t want to miss. If you are interested in becoming an analyst and taking part in the competition, click here to find out more and submit your article today!

Read the full article here