A Power Hitter

We have posted mostly positive articles over the last few years assessing the potential of construction and maintenance companies providing mechanical, power, energy, electric, communications, and building services. Comfort Systems USA (NYSE:FIX) stock is the poster child for this sector of the economy. The price skyrocketed +800% over 5 years and +92% over the last 12 months. It closed August a few dollars short of the stock’s 52-week high of $358.89 per share. We rate the stock for retail value investors potentially best as a Hold-to-Moderate Buy opportunity, at this time.

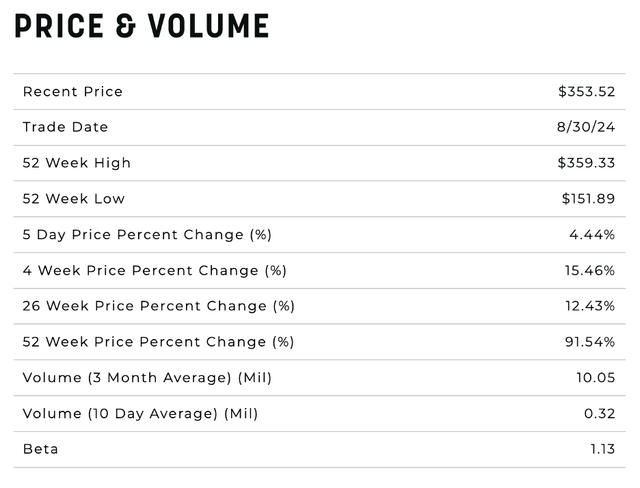

Price & Volume Data (Comfort Systems USA)

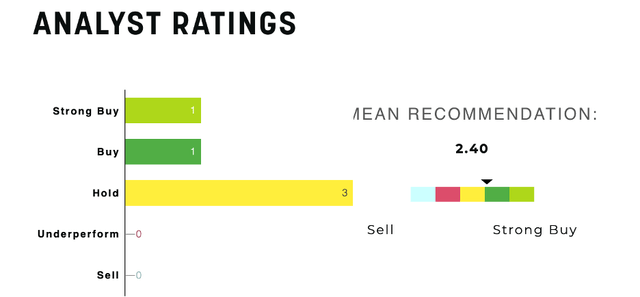

The consensus among analysts like our assessment shifted from Buy to Hold over the last quarter. In our opinion, investors have confidence in management, but the stock appears to be significantly overvalued today. Average share price targets hover over the next six months at around $370 to $400 per share.

Analysts Ratings (Comfort Systems USA)

Growth and Profitability

We believe the stock’s momentum is driving up the price. Comfort’s total return is over 3xs higher YTD (72.34%) than the S&P 500 total return (+19.53%). The S&P 500 5-year total return is 109.29% compared to Comfort System’s 843.57%.

Comfort Systems USA is a relatively young public company, being a little more than a quarter-century old. Comfort Systems USA started with 12 operating companies, and, today, totals 45 firms across America. Management adopted an aggressive M&A strategy, purchasing over 20 facility management and energy-efficient tech firms, including 5 in the last few years. Management points out in their comments to shareholders that the margins for the mechanical and electrical segments were outstanding. This quarterly report spurred momentum.

Here are some other highlights:

- The company foresees 5-year annual and revenue growth at ~20%.

- 5-year EPS growth will be greater, topping 24.5%.

- Net income was $134M in the second quarter of ’24 versus $69.5M Y/Y.

- Diluted EPS in ’24 almost doubled to $3.74 compared to $1.93.

- Revenue was $1.81B compared to $1.3B a year earlier in the second quarter; the revenue is generated mostly from new construction installation and maintenance services for existing buildings.

- Operating cash flow increased by $64.5M to $189.9M from $125.4M in Q2 ’23.

- Net income was $230.3M or $6.43 EPS diluted; both were up from Q2 ’23 by some 45%.

- We expect more new contracts signed, jobs completed, and backorders fulfilled in Q3 ’24 and Q4; margins will hold steady at ~20%.

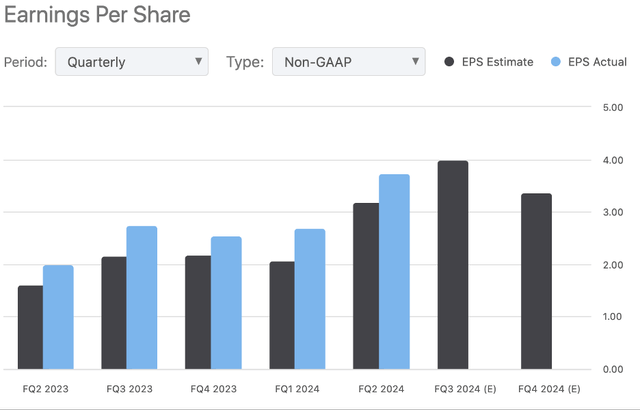

- The Q3 ’24 EPS will significantly top Q2 ’24 by as much as 20 cents (~$3.95 EPS) and over $1 more than Q3 ’23’s EPS of $2.74. The company beat EPS expectations in each of the last 9 quarters.

- The company’s backlog of orders popped to $5.22B from $4.19B between June ’24 and June ’23 a year when analysts anticipated a slowdown in construction equipment sales, labor shortages, and overall weaker conditions in the 2024 construction facilities sector.

- Comfort’s next earnings announcement is due October 24, 2024.

EPS Actual & Est (Seeking Alpha)

Headwinds and Valuation

We contend that most of the good news has already been factored into the share price momentum. There are no titanic or inexorable risks that we or others foresee. Short interest is a mere 1.5%. However, as the share price moved up, we are experiencing a niggling skittishness for several reasons:

- The stock’s volatility (Beta 1.13) raises our eyebrows.

- There are implied risks the construction sector will grow softer in 2024 and 2025.

- A new study reported in Construction News claims inflation in construction projects will hold at 5% to 6% annually over the next 2/5 years; in our experience, this raises costs and eats away at bottom-line profits of contracts yet completed.

- Labor shortages still plague the construction industry, it is taking longer for architectural firms to complete designs, and growing difficulties in permit and zoning processing due to environmental restrictions, community opposition, and cutbacks in state and local budgets are slowing the pace of construction starts and completions.

- YTD corporate insiders have sold significantly more shares than they bought. The number of hedge funds owning shares doubled between 2020 and Q2 ’24, but they decreased their holdings by nearly 100,000 shares over the last three months.

Insider Purchases & Sales of Shares (InsiderScreener)

Comfort Systems is committed to the popular trend of repurchasing stock rather than upping its dividend yield [FWD] which traditionally attracts retail value investors. With little impetus for the share price to move higher, the low yield of the dividend will result in more share sales. The dividend gets high grades for safety, consistency, and growth, but a D- for yield. Compared to the industrial sector metrics of the market, Comfort’s dividend metrics evince a poor showing and the year-end yields have fallen since 2014.

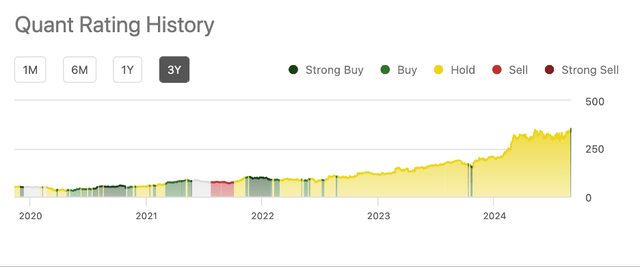

Comfort System’s valuation metrics are weaker than the nation’s industrial sector metrics. Seeking Alpha’s Quant Rating has been at Hold level at least during the last 24 months, with a few short-term exceptions.

Comfort Systems Quant History (Seeking Alpha)

The PE-to-GAAP (TTM & FWD) is graded near failing, as are EV-to-EBITDA, and Price-to-Book. Price-to-cash-flow, price-to-sales, and a few other metrics rate mediocre. Despite the M&A and stock repurchase program, the company’s long-term debt is down, shareholder equity is up and the debt-to-equity ratio is acceptable; management is using debt wisely. But debt can become a worrisome headwind. In 2022, management “amended its existing senior debt facility to increase the credit commitment amount to $850,000,000 and to extend the term to July 5, 2027.”

Comfort’s long-term debt-to-equity ratio (FY) is 3.08 whereas 2 and under is a more satisfactory ratio. Cash outstrips company debt; cash flow from operations covers debt payments, and EBIT covers interest payments. Its quick ratio is 1.07 below the 1.1 threshold. The current ratio of assets over liabilities is 1.11. At a minimum PE of 25.62 times the consensus FY ’24 EPS forecast of 13.20, the fair value per share is ~$338 each, less than the current share price on the momentum run-up. Multiplying Comfort’s peer average PE of 30 takes the share price to $396.

Takeaway

An analyst once lamented it’s not the losses that bother him, but the missed opportunities. Comfort Systems was a missed opportunity for us and other small investors. The lack of a robust dividend yield and growing debt during years of inflation turned us off on the stock. Management’s success was building shareholder equity and slashing debt. Comfort has enjoyed strong growth and profitability with little risk. There may be headwinds, but we are confident management will be able to contend with them. The current share price is on the low side of a fair value for retail value investors, who can generate much higher dividend yields elsewhere. We rate the stock a Hold to Moderate Buy if an investor is willing to bet momentum will carry the shares higher, though insiders are selling.

Read the full article here