Investment Thesis

Teradata Corporation (NYSE:TDC) is a cloud data platform for enterprise analytics. Their primary objective is to support various industries, allowing companies to optimize their data, improve decision-making, and promote growth through data-driven insights and streamlined data management.

Undoubtedly, Teradata has an alluring narrative. The problem here is that, beyond its narrative, its growth rates leave much to be desired.

On the other hand, I declare that although Teradata’s growth rates are somewhat mediocre (to put it kindly), Teradata is already making substantial free cash flow and is determined to return excess free cash flow back to shareholders. According to my estimates, Teradata will return 6% of its market cap back to shareholders in 2023.

Consequently, on balance, there are more positives than negatives to this stock.

Teradata’s Near-Term Prospects

Teradata is a company that focuses on data analytics and management. They provide a multi-cloud data platform designed to help enterprises effectively utilize their data resources.

Teradata specializes in assisting organizations with addressing complex business challenges by offering analytics solutions, including digital identity management, and artificial intelligence.

They also facilitate the transition to the cloud by providing tools that ensure consistent software performance across cloud and on-premises environments. Teradata’s services encompass consulting to establish data and analytics strategies.

Teradata has recently made significant strides in innovation and strategic imperatives, setting the stage for further growth. One notable innovation is the introduction of Teradata VantageCloud Lake on Microsoft Azure (MSFT), a cloud-native architecture available globally. This offering provides enterprises with the scalability needed to support AI and ML capabilities, emphasizing Teradata’s commitment to end-to-end support for advanced analytics. The integration of ClearScape Analytics with Microsoft services, such as Azure Machine Learning, enhances customers’ ability to deploy and manage AI and ML, including generative AI and large language models, within their businesses.

Teradata’s strategic imperative extends beyond just AI. Teradata makes the case that businesses today are grappling with increasing data complexity. As a result, Teradata positions itself to help organizations leverage AI to tackle complex challenges and create substantial enterprise value. This strategic vision extends to the promise of AI, which opens up new opportunities for productivity enhancements and innovation.

As I already noted in the introduction, Teradata has a surprisingly seductive narrative. However, its financials and outlook don’t appear to be congruent with its story.

Teradata’s Revenue Growth Rates, Recent Best Was Q2 2023?

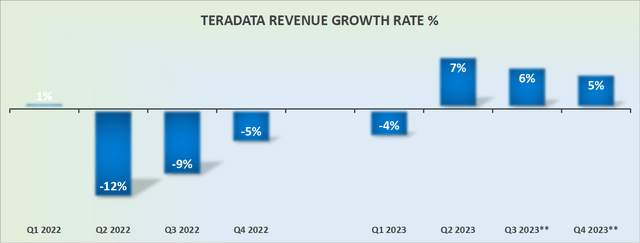

TDC revenue growth rates

The graphic above may not be immediately obvious just how strong its Q2 results turned out to be. More specifically, Teradata’s Q2 2023 delivered 7% y/y growth, or 10% in constant currency, which was its first meaningful year-over-year revenue growth since Q2 2021.

That being said, throughout its earnings call, Teradata acknowledges that in the second half of 2023, may face tougher year-over-year comparisons, primarily due to the substantial growth achieved in the second half of 2022.

This moderation is driven by the challenging comparison to the prior year’s strong performance, where a significant portion of the cloud ARR growth occurred in the second half.

All that being said, I believe it’s safe to surmise that Teradata’s near-term growth rates are likely to moderate and grow its CAGR in the high single digits.

But this isn’t where this story ends, because what Teradata lacks in terms of growth, it makes up with its attractive free cash flows.

A Data Storage Company That Knows How to Make Free Cash Flows

Teradata has continued to return capital to shareholders via share repurchases. More concretely, Teradata repurchased 106% of its first-half free cash flow to shareholders.

Furthermore, Teradata reaffirms its commitment to returning at least 75% of free cash flow to shareholders in 2023.

This means that in practice, this year, Teradata will have returned around 6% of its market cap back to shareholders.

Moreover, Teradata does hold some debt, but its approximate $500 million of debt is offset by around the same cash figure, meaning that its balance sheet will not get in the way of further share repurchases in 2024.

The Bottom Line

Teradata is a cloud data platform that aims to empower various industries by optimizing data utilization. Despite its appealing narrative, the company’s growth rates have room for improvement. However, it’s worth noting that Teradata is generating substantial free cash flow, which balances the equation.

Teradata’s recent financial performance, particularly in Q2 2023, showed positive signs of revenue growth after a period of slower growth. However, the company acknowledges that the second half of 2023 might face tougher year-over-year comparisons due to substantial growth in the previous year.

While growth rates may moderate in the near term, Teradata’s ability to generate attractive free cash flow and its commitment to returning value to shareholders through share repurchases are noteworthy. With a balanced financial position and strategic initiatives in place, I believe that Teradata’s positives outweigh its negatives.

Read the full article here