It’s been a tough three months for the restaurant industry group, with the AdvisorShares Restaurant ETF (EATZ) plunging ~20% in barely 50 trading days, pushing the index back into negative territory for the year. And while richly priced newer concepts like Dutch Bros (BROS) and Cava (CAVA) have been the primary losers with 30%+ share-price declines, casual dining giants like Texas Roadhouse (NASDAQ:TXRH) and Darden (DRI) haven’t been immune and have seen sharp pullbacks as well. In fact, Texas Roadhouse has found itself down ~20% from its all-time highs set earlier this year despite another exceptional Q2 report. Let’s look at the results below and whether the stock is approaching a low-risk buy zone:

Texas Roadhouse – Company Website

Recent Results & Developments

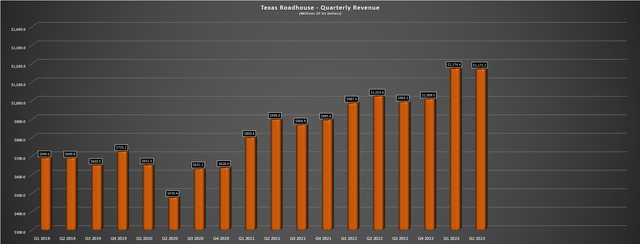

Texas Roadhouse released its Q2 results ended June 27th in late July, reporting quarterly revenue of $1.17 billion, just shy of its previous record reached in Q1. The strong results were driven by impressive comp sales growth of 9.1% and 9.2%, at company-owned and domestic franchised restaurants, respectively, with Texas Roadhouse being one of the few brands not relying solely on pricing (Q2: 5.6%) to drive sales. In fact, the company noted that guest counts were up which bucked the industry average, with 4.7% traffic growth in the period. If we compare this to OpenTable Seated Diners statistics in Q2, these results translated to a 500+ basis point beat, with the company calling out new guest traffic from some people trading up to Texas Roadhouse.

Texas Roadhouse – Quarterly Revenue – Company Filings, Author’s Chart

Looking at the results in a little more detail below, we can see that this contributed to a 14% increase in sales year-over-year, while quarterly earnings per share increased to $1.22, up from $1.07 in the year-ago period (+15% year-over-year). Meanwhile, average weekly sales came in just shy of $150,000 at $146,700 (Q2 20222: ~$135,500) and off-premise sales have remained sticky, with ~12.6% of sales coming from off-premise in the period. Just as encouraging, while traffic ticked up in July for the industry, Texas Roadhouse continued to outperform, reporting ~10.3% comp sales for the first four weeks of Q3 or 8.9% comp sales growth when adjusting for the positive impact from the timing of the July 4 holiday.

Given these strong results and solid development in the period (6 new restaurants and 13 opened year-to-date, plus the first franchised Jaggers restaurant in Jacksonville), the company was confident to reaffirm its view of positive comp sales growth this year. However, there were some negative offsets. The company took its capital expenditures outlook higher to ~$300 million because of new locations and more expensive reinvestments than anticipated. Meanwhile, it expects commodity inflation to come in at the high end of the range (5-6%), while wage/other labor inflation will come in above 6%, with TXRH noting that it saw more wage inflation than it expected in H1. The result was that margins slipped to 15.7% (Q2 2022: 16.6%), with higher food & beverage and labor costs offset by a slight dip in other costs, with the former impacted by higher beef costs.

Texas Roadhouse Offerings – Company Website

Industry-Wide Trends

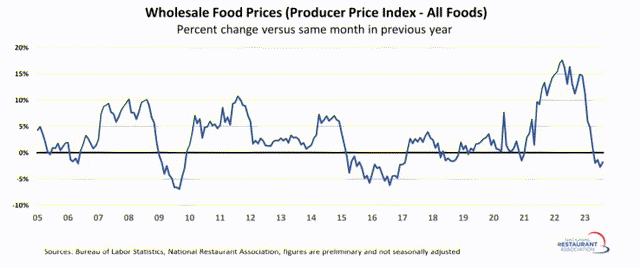

Moving over to industry-wide trends, we can begin with the positives, which is that commodity inflation has cooled off from double-digit levels last year, and Texas Roadhouse noted that chicken and pork are two areas where it’s seeing some deflation. Meanwhile, turnover has may be partially attributed to a significant investment in wages at several brands over the past two years, reducing hiring/training costs vs. the two-year period following the onset of the pandemic where full staffing was a challenge. That said, like BJ’s Restaurants, Texas Roadhouse called out beef as a contributor to higher inflation, offsetting some gains in other areas of its market basket. This is not surprising according to August statistics, with beef and veal costs being one of the most inflationary categories, up 16% year-over-year vs. a decline in the overall commodity basket, making beef/veal a clear outlier with refined sugar.

Wholesale Food Prices – National Restaurant Association, BLS

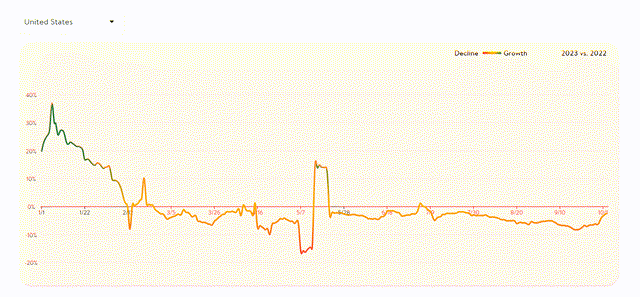

Unfortunately, while Texas Roadhouse had a solid H1 and the softness in commodity prices (ex-beef) helps and it’s exciting to hear that traffic remains strong, there were some negatives. For starters, while most restaurants had relatively positive commentary on their Q2 Calls related to traffic to start Q3, OpenTable data suggests that traffic rolled over shortly after and worsened throughout the quarter. The good news is that Texas Roadhouse has bucked this trend for most of the year and outperformed its peers, suggesting it may not have seen the same hit. However, with traffic remaining deeply negative for most of Q3, it’s hard to be overly confident in the company’s ability to beat Q3 estimates, and the August heat wave in the southern states may not have helped which may have limited outdoor dining in key markets (over 25% of system).

Seated Diners Year-over-Year – OpenTable

The other negative call out from two larger operators (Texas Roadhouse and Darden) is that there appears to be some early signs of check management, with a negative mix related to alcohol. And while it appears to be winning new guests, they may be shopping on the lower end of the menu, even if this is boosting top-line sales. The company noted that the lower alcohol attachment may simply be a normalization of not getting a second drink like last year with some diners indulging more post-COVID-19 and with the benefit of stimulus. Still, this is a minor negative and one thing that will need to be monitored and check management hasn’t been called out to date, and this may finally be a sign that the consumer is weakening and even if they are still visiting their favorite locations, they’re passing on the extra appetizer or drink.

The silver lining for an iconic brand like Texas Roadhouse is that winning guests and growing traffic puts it in rare air, and the company has consistently delivered an exceptional guest experience with high-quality ingredients which has allowed it to grow into the massive company it is today (700+ restaurants). So, if consumers do become more judicious when it comes to dining out, this should benefit proven brands with consistent guest experiences. Hence, although the negative traffic trends that continued into October following a terrible September are not a great sign, Texas Roadhouse might be able to navigate this better than peers as it has bucked these trends year-to-date. Let’s dig into the valuation and see whether the macro headwinds (weaker consumer, rising costs) are baked into the stock:

Valuation

Based on ~67 million shares outstanding and a share price of $96.20, Texas Roadhouse trades at a market cap of ~$6.45 billion and an enterprise value of ~$7.08 billion. This makes it one of the highest capitalization stocks in the industry group, and it sits there for good reason, with it being one of the strongest earnings growers sector-wide and one of the better-run names, evidenced by annual EPS being up ~175% from F016 to FY2023 based on current estimates and an impressive 10-year average ROIC of 14.1%. That said, while TXRH is certainly an example of quality in the space, it’s hard to argue that the stock is cheap, with it trading at ~23.5x FY2024 free cash flow estimates vs. its current enterprise value and ~12.0x FY2024 EV/EBITDA. The latter figure is average EV/EBITDA multiple over the past 15 years of ~11.5x, and its FY2024 free cash flow multiple leaves it trading near a ~4.3% forward free cash flow yield which is not that cheap in the current rate environment with macro headwinds.

Using what I believe to be a more conservative multiple of 13.0x EV/EBITDA using FY2024 estimates and ~66 million shares which assumes continued share repurchases (~214,000 shares repurchased at $109.35 in Q2), I see a fair value for the stock of $108.00, translating to a 12% upside from current levels. However, I am looking for a minimum 25% discount to fair value for mid-cap stocks to ensure a margin of safety, and ideally closer to 30% in the current market. And if we adjust for the low end of this required discount (25%), TXRH’s ideal buy zone to bake in a margin of safety comes in at $81.00 or lower. So, although the stock may be more reasonably valued after correcting sharply from its highs, I still don’t see nearly enough of a margin of safety to justify paying up for the stock here near $97.00. All that being said, the stock is short-term oversold, and could get a bounce short-term to relieve its oversold conditions.

Summary

Texas Roadhouse has had a solid year despite the slowdown in industry-wide traffic and has been one of the few brands to report consistent double-digit revenue growth with solid traffic performance vs. its peer group. However, traffic has worsened further in Q3, with the brief improvement in industry-wide traffic in July being short-lived, followed by a significant deceleration in August and September, with the potential for a further impact because of the August heat wave. Hence, it’s more difficult to be confident in a beat on the upcoming Q3 results given the negatives in the period (rising gas prices, industry-wide traffic slowdown, heat wave in its core market). And when combined with the stock only trading ~10% below fair value and several names being more attractively valued from a relative standpoint, I think there are better bets in the market. Hence, if I were looking to put capital to work with pessimism increasing market-wide, I see Sandstorm Gold Royalties (SAND) as a more attractive option, trading at just ~11x FY2025 free cash flow estimates with ~80% gross margins.

Read the full article here