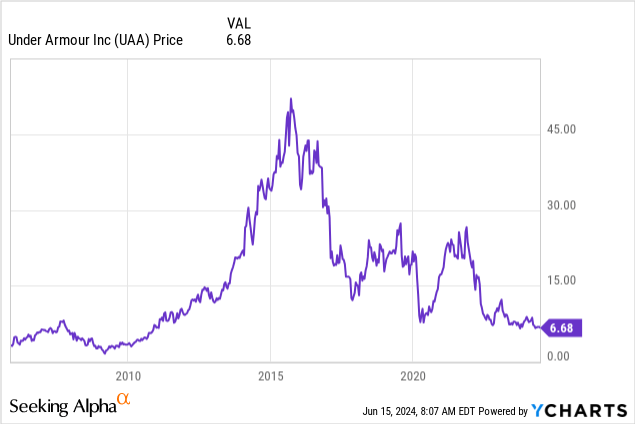

Under Armour, Inc. (NYSE:UAA) (NYSE:UA) saw its stock quote peak above $50 in 2015, following its IPO in November 2005. Rapid growth in its synthetic-fiber sports apparel and shoe business targeting serious athletes helped to transform this equity into a top “growth” name after a decade of public trading.

YCharts – Under Armour (Class A), Stock Price Changes, Since November 2005 IPO

Then, business trends reached their zenith, and the company moved its strategy toward flooding the market with branded products at third-party sellers everywhere. During FY 2024 ended in March, wholesale sales accounted for about 56% of total business, with the rest marketed through DTC company locations and websites. Apparel items represented 65% of sales, with shoes (24%) and accessories (11%) rounding out the retail business model. 1,900 physical stores, with product sold to consumers in 100 countries is the global footprint. North America accounted for 61% of sales.

Today, after years of stagnant sales and income generation, the stock has moved from an extreme in growth-based valuations (investor optimism) to the bottom of the value barrel (investor pessimism). At share prices below $7 in June 2024, investors are basically able to buy the company at its cheapest setup since trading began. Management has downgraded expectations for this year, with a large $70-90 million in restructuring charges coming. Wall Street has reduced projections and price targets dramatically. And, investors have effectively given up on the company’s future.

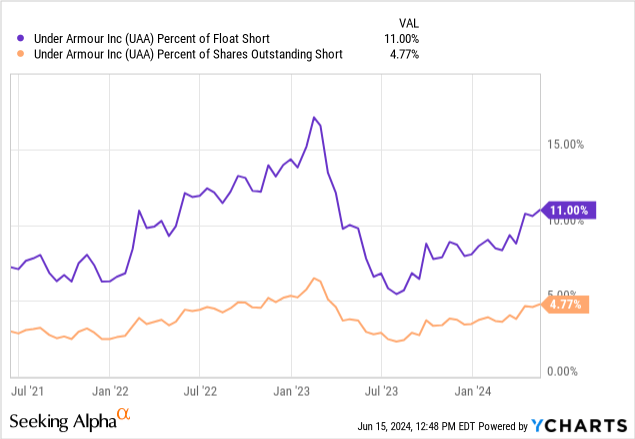

To me, it sounds like any good news from the company (like earnings and sales beats from the current low-balled guidance) could translate into a flood of buying interest. For sure, the large short position (selling borrowed shares in the open market) is betting on bad news remaining the FY 2025 theme. If investor sentiment has hit its low in May-June, short covering could help support price going forward.

YCharts – Under Armour, Short Interest Positioning, 3 Years

When we review Under Armour’s lowest valuation setup of the major apparel and shoe retailers/manufacturers, I am beginning to wonder if all the bad operating news has already been factored into the share quote. The contrarian side of my investment personality is screaming to buy shares, not sell them. What is the upside/bullish argument for ownership?

Restructuring Effort

Last month, Under Armor’s founder and main shareholder Kevin Plank (holding 64% voting control in 2023) was tapped to retake the reins as CEO, with a goal of righting the ship (he left day-to-day decision making in 2019). A restructuring plan away from wholesaling its products to other retailers (with a goal of achieve incremental volume sales increases) will be refocused on returning the brand to more of a premium status with consumers. According to a middle of May article by SA News Editor Amy Thielen,

To close the gap with competitors like On Holdings (ONON) and Nike (NKE) and to address criticism that Under Armour sold too much too cheaply at discount retailers, Plank is repositioning the company and focusing more on brand image by selling higher-priced exclusive products at its own stores and DTC, and reduce the amount of discounted merchandise to wholesale clients, mirroring the marketing strategy of brands like Lululemon (LULU).

The company has three classes of stock, each with different voting power. The two publicly traded are Class A with 1 vote each under the symbol UAA. Class C is the other equity-only share with no voting rights, available to own in your brokerage account. Super-voting Class B Convertible shares are mostly owned by Mr. Plank with 10 votes each. As of May 15th, 2024, 188,802,043 shares of Class A, 34,450,000 shares of Class B and 213,245,598 shares of Class C were outstanding (according to the latest 10-K filing).

I own the Class A shares with somewhat better liquidity in trading of late, historically valued at a slight price premium to Class B (no voting) units.

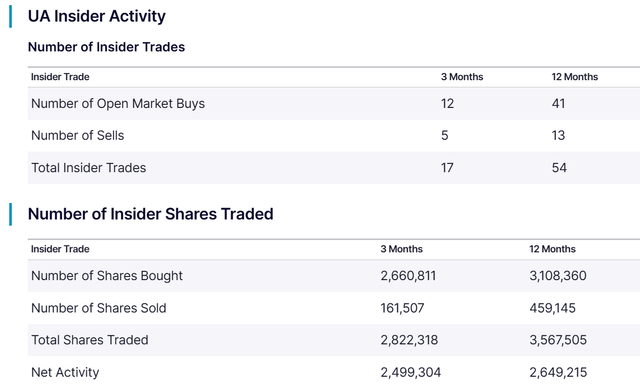

Net insider buying is also present in the stock, mostly through stock grants to employees and directors. If management believed the turnaround situation was hopeless or unlikely to bear fruit, I would expect to see a much greater rate of insider selling.

Nasdaq.com – Under Armour, Insider Transactions, 12 Months

Guidance for FY 2025 from the Q4 2024 earnings call transcript,

…From a channel perspective, we see our wholesale business be down at a low double-digit rate, and direct-to-consumer to be down approximately 10% due to proactive actions to significantly reduce the discounting level within our own e-commerce business. This reflects some of the foundational steps in our ambition to create a more premium stance for our brand.

By product, we expect apparel and footwear sales to be down at a low double-digit rate and our accessories business to remain essentially flat year-over-year. Even with this revenue contraction, we expect a gross margin improvement of 75 to 100 basis points due to the material reduction in promotional and discounting activities through our DTC business and proactive product and costing initiatives.

Turning to SG&A, as we work to streamline our business further, we anticipate our expenses to be down 2% to 4% in fiscal 2025. This includes a Board approved restructuring plan to help strengthen and support additional financial and operational efficiencies. While Dave will provide more detail, we expect to incur a total estimated pre-tax restructuring and related charges of approximately $70 million to $90 million. Excluding the midpoint of this restructuring range, we expect $130 million to $150 million in adjusted operating income, representing $0.18 to $0.21 of adjusted diluted earnings per share…

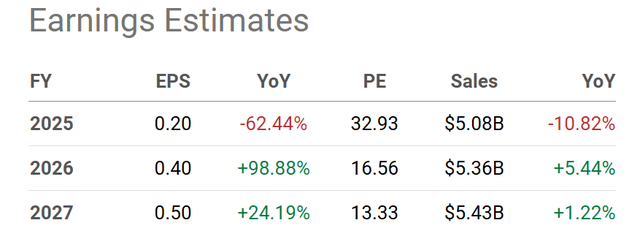

Wall Street analysts are going with management’s guidance for current fiscal year projections, looking at the return of typical sales and margins by the end of 2025 (FY 2026). My view is the estimates pictured below could prove on the conservative side, assuming a major U.S. and global recession is avoided this year and next.

Seeking Alpha Table – Under Armour, Analyst Estimates for FY 2025-27, Made June 14th, 2024

One saving grace for shareholders is the balance sheet at the end of March included $858 million in cash vs. $676 in financial debt and $767 in lease obligations (mostly long-term). With $600 million of debt financed at interest rates of 3.25% into June 2026, and cash earning high rates of yield since 2023, net interest “expense” was actually an income number of +$300,000 over the trailing 12 months.

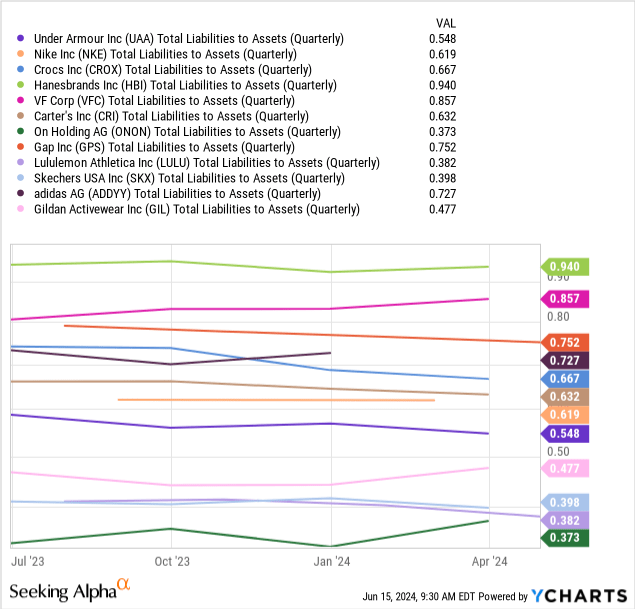

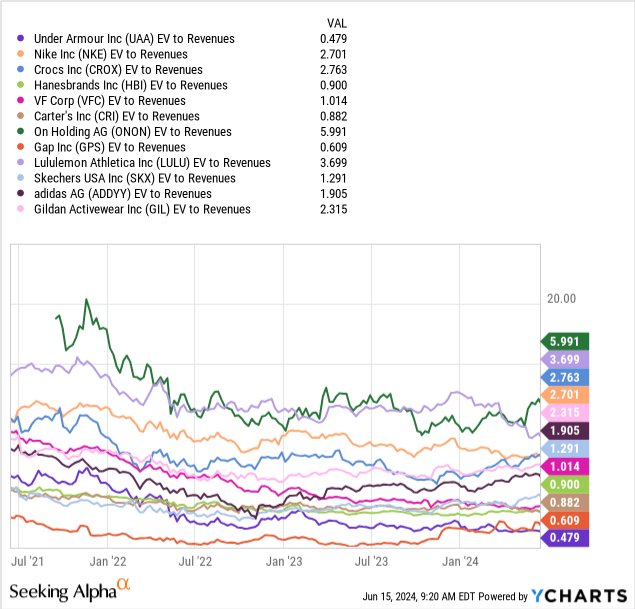

Another positive providing ample time for the restructuring effort is total liabilities vs. assets are sitting at a relatively low 55% level vs. shoe/apparel peers and competitors. You can review this bullish setup below, compared to Nike (NKE), Crocs (CROX), Hanesbrands (HBI), VF Corp (VFC), Carter’s (CRI), On Holding AG (ONON), Gap (GPS), Lululemon (LULU), Skechers USA (SKX), adidas AG (OTCQX:ADDYY), and Gildan Activewear (GIL).

YCharts – Under Armour vs. Major Shoe/Apparel Peers, Total Liabilities vs. Assets, 1 Year

So, if the turnaround effort stabilizes sales while improving margins, what is Under Armour worth?

Bargain Valuation

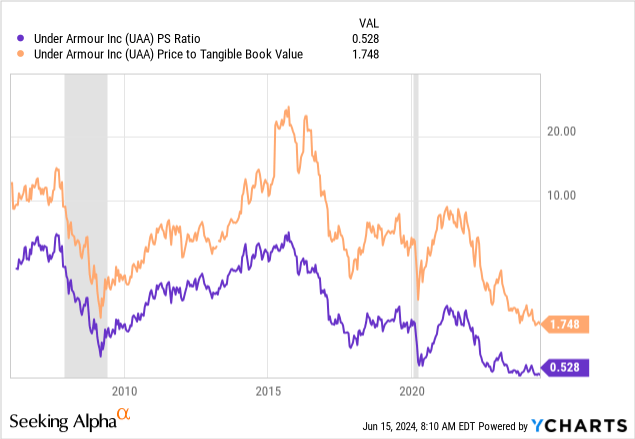

That’s where the share ownership story gets really interesting. I peg Under Armour today as sporting one of the lowest (if not “the” lowest) overall valuation on fundamental metrics in the clothing industry. Below I have graphed the cheapest ever valuation of the business on sales and tangible book value (mostly liquid cash, receivables and inventory). The 0.53x price to trailing sales and 1.75x tangible book value multiples are a good 75% to 80% discount to long-term averages. These ratios are already much lower than either the 2008-09 Great Recession or 2020 Pandemic panic.

YCharts – Under Armour, Price to Sales and Tangible BV, Since 2006, Recessions Shaded

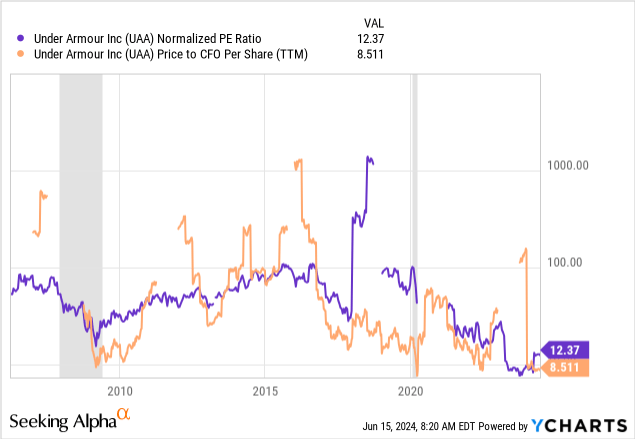

On “normalized” earnings and cash flow generation, Under Armour is priced near record lows also. 12x trailing EPS (which will change on the restructuring effort this year), and 8.5x cash flow are both huge 60% to 70% discounts vs. long-term averages.

StockCharts.com – Under Armour, Price to Trailing Earnings and Cash Flow, Since 2006, Recessions Shaded

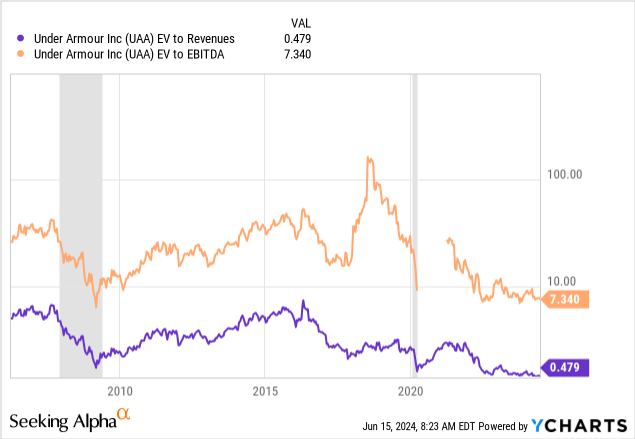

When we include changing debt and cash levels held over the years, the enterprise valuation is equally compelling. EV to Revenues is bumping against its lowest reading ever at 0.48x, and EV to EBITDA of 7.3x is now about the same as the worst levels of the Great Recession in 2009.

StockCharts.com – Under Armour, Enterprise Value to Trailing Sales & EBITDA, Since 2006, Recessions Shaded

Both EV to Revenues and EBITDA are trading at or near the lowest ratios in the peer sort group. The high-volume, low-margin, mass marketer of Gap is even more expensive than Under Armour today on sales. UAA and UA are trading at 60% discounts to the median sector average around 1.4x.

YCharts – Under Armour vs. Major Shoe/Apparel Peers, EV to Trailing Sales, 3 Years

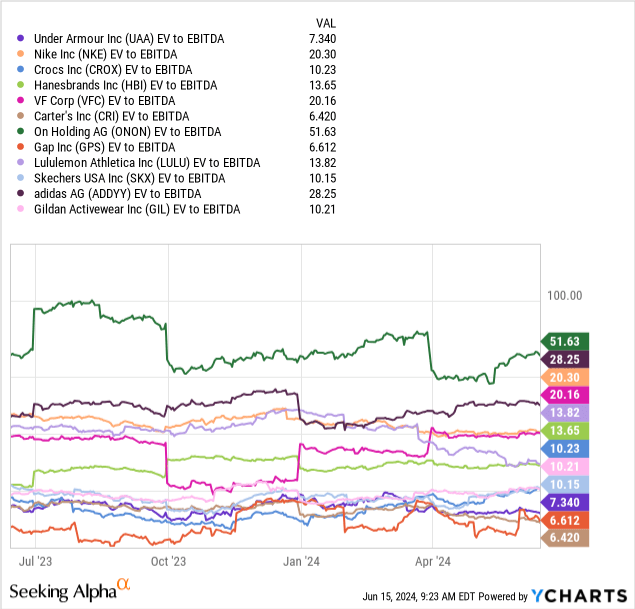

On EV to EBITDA, only peers Gap and childrenswear specialist Carter’s are in the same neighborhood for a valuation. This multiple is still a 35% discount to peer averages.

YCharts – Under Armour vs. Major Shoe/Apparel Peers, EV to Trailing EBITDA, 1 Year

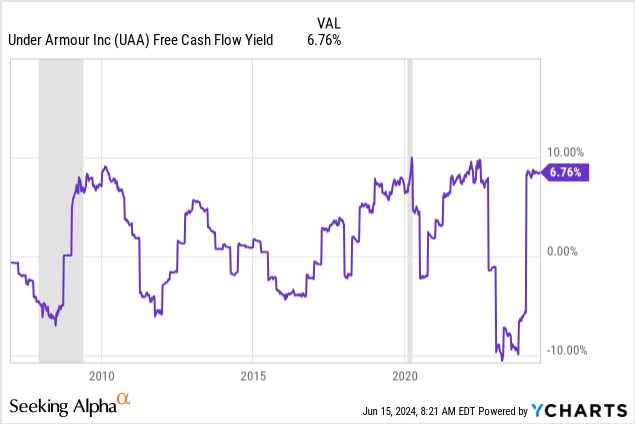

Lastly, plenty of free cash flow generation each day is still available to management for shareholder value creation. The free cash flow yield of 6.76% currently (on trailing results which will turn lower on $40-50 million in anticipated cash restructuring charges this summer) is nearer the top end of the range historically experience by this retailer/manufacturer. What I am saying is the business has room to finance its turnaround without tapping the bond market for added leverage/debt issuance. The board of directors did reauthorize a $500 million share buyback option to support the stock price from its cash hoard (and future cash generation).

YCharts – Under Armour, Free Cash Flow Yield on Investment, Since 2006, Recessions Shaded

Technical Momentum Pattern Improving

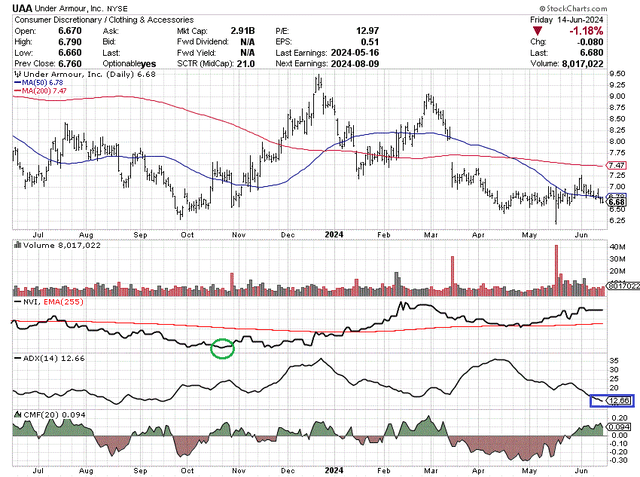

The trading chart looks like it is trying to hold the low-$6 price bottom of September. The Negative Volume Index (something of an indication of overhead supply) reached its worst reading in October, circled in green below. The 14-day Average Directional Index score of 12 is the lowest-volatility mark since September also. There seems to be a much better balance of supply and demand since April, even with high trading volumes. Rounding out my review, the 20-day Chaikin Money Flow calculation has turned positive in recent weeks. Overall, the pattern appears to be in a similarly constructive zigzag to the September-October bottom in price last year, going into a +40% price gain by December.

StockCharts.com – Under Armour, 12 Months of Price & Volume Changes, Author Reference Points

Final Thoughts

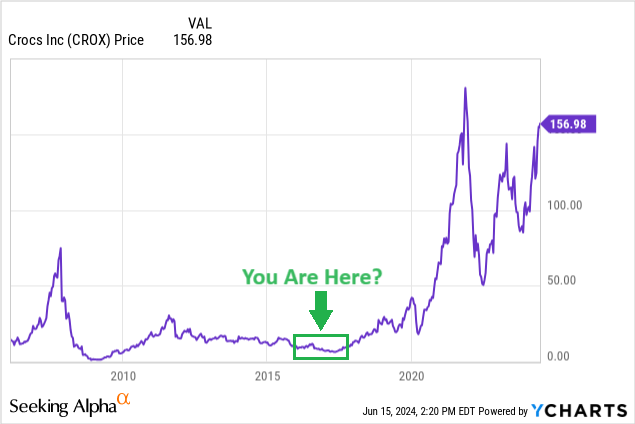

Please don’t say Under Armour can never recover and flourish again. Many said Crocs was dead money years before the COVID pandemic hit. CROX languished for several years in price, at an incredibly low valuation few wanted to own. Then sales and income surged as consumer rushed to purchase comfortable, stay-at-home shoes. Retail tastes do ebb and flow. Sound familiar? Believe it or not, the EV to Revenues multiple at Under Armour is today lower than the 2017 price bottom in Crocs (as are other stats).

YCharts – Crox, Price Changes, Since 2006, Author Reference Point

What are the risks for new investment? Of course, if the economy is slowing into recession, I cannot rule out a drop to $6 or even $5 a share in coming months. Fortunes in the retail business are quite sensitive to consumer spending and changing tastes.

Perhaps the restructuring and refocus on developing its premium brand will not produce the desired results of higher sales and income (on price increases per item, all told). And, it may take 12-18 months to figure out the success or failure of this push.

However, my view is lower share prices could be temporary and may serve to open a stronger buy entry for new investment. Valuations could compress into a truly bullish setup like a spring. Then, when the restructuring pays dividends or the economy recovers from recession, a big price jump toward a normalized valuation gets UA and UAA closer to $10 or $15 rather quickly. For sure, the math gains on purchase prices below $5 could deliver courageous investors +100% to +200% total returns by the end of 2025 (18 months out).

I rate shares a Buy, and recently bought a small position in my diversified portfolio. If prices decline under $6, I may increase my stake significantly. I consider prices under $5 as Strong Buy territory, all other variables remaining the same.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here