August 27th ended up being a really interesting day for shareholders of both First Busey Corporation (NASDAQ:BUSE) and CrossFirst Bankshares (NASDAQ:CFB). Shares of both companies pulled back slightly after news broke that the businesses would be merging into one. I find this interesting, particularly when it comes to First Busey. Based on the data provided by management, as well as historical results for both firms, this transaction should prove positive for shareholders, particularly for those owning shares of First Busey.

This comes down to a number of factors, including improved asset performance, management’s ability to pick up a business that has certain strengths that First Busey has lacked in recent years, and to do so in a way that lowers the overall trading multiples of the business. While shareholders of First Busey are most certainly the winners from this transaction, the picture doesn’t look awful for CrossFirst. At the end of the day, its investors should have ended up with a larger share of the overall pie. But together, the two firms will be stronger, larger, and more operationally efficient.

A look at the transaction

According to a press release issued by First Busey on August 27th, both it and CrossFirst agreed to merge together in an all-stock transaction valuing CrossFirst at $916.8 million. In exchange for each share of CrossFirst that an investor owns, they will receive 0.6675 of a share of First Busey. Upon completion of the transaction, shareholders of First Busey will own about 63.5% of the overall business, while shareholders of CrossFirst will own the remaining 36.5%. Unfortunately, the market did not take this news in a positive light. Shares of CrossFirst are down about 3.4% for the day as of the time of this writing. The picture for First Busey isn’t much better, with shares down about 2.5%.

First Busey Corporation

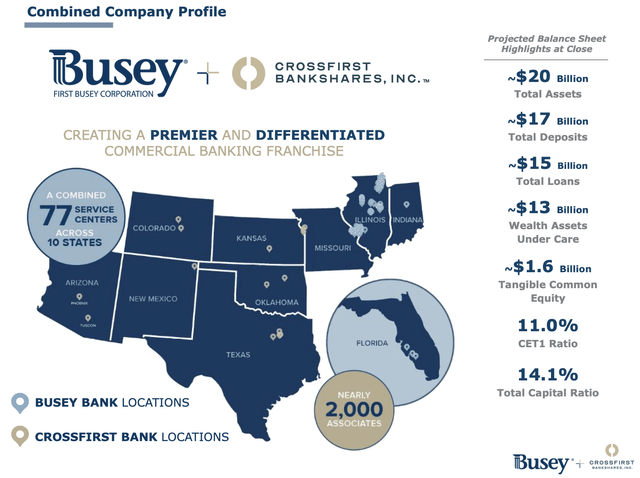

In a lot of ways, this acquisition makes a great deal of sense. The companies have operations that are geographically distinct from one another, so there is little risk of cannibalization. All combined, the enterprise will have 77 service centers spread across 10 different states. Collectively, the two firms have about $19.6 billion in total assets that will be brought under a single umbrella. They also have about $16.7 billion of total deposits. The management team at First Busey sees this as a way for the regional bank to significantly expand its reach, with operations now growing into Oklahoma, Texas, New Mexico, Colorado, and Arizona.

First Busey Corporation

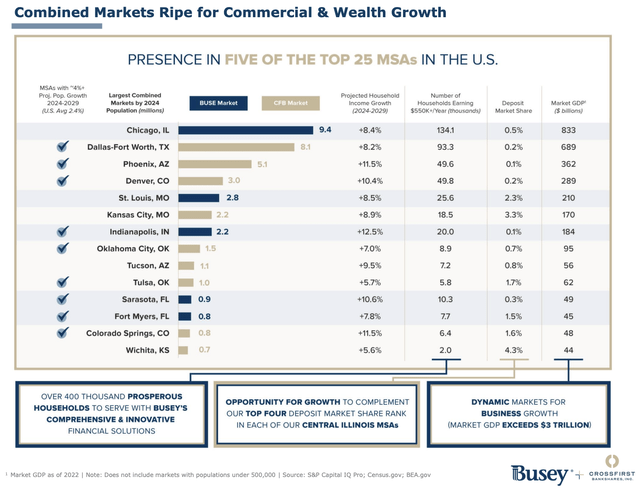

Combined, the business will have a significant presence in certain key markets. This will include in five of the top 25 MSAs (metropolitan statistical areas). Nine of the top MSAs that the combined business will operate in are projected to have total population growth of around 4% or more between 2024 and 2029. This will result in significant projected household income growth during that window of time. As a small institution, the combined business will still have a small share of total deposits in these MSAs. But you have to start off somewhere. Seeing as how the major markets that the combined company will operate in represent over $3 trillion worth of GDP, the opportunities for expansion are significant.

There’s also the opportunity for some cost savings. If everything goes according to plan, savings will amount to roughly $25 million on an annualized basis, with that number expected to grow about 3% annually for the foreseeable future. Half of these savings are expected to be realized in 2025 if the deal closes at the end of March of next year as planned. However, these cost reductions will not be free. Management expects $75.3 million in pre-tax merger related costs associated with the transaction, $42.1 million of which will be recognized at the time of close, with the remainder being recognized through 2028. This is in addition to another $3 million of capitalized expenses.

Even though there are no guarantees that synergies will be realized, the fact of the matter is that First Busey has a solid track record of completing mergers and acquisitions. Since 2015, the company has completed 7 entire bank mergers that had aggregate assets of over $7 billion. This is in addition to one wealth management firm acquisition. This is not to discount the track record that CrossFirst has, with that company having completed two bank acquisitions in the last three fiscal years. Even though most of my emphasis for this article involves the banking operations of these companies, it is also worth noting that the combined firm will have a significant asset base for its wealth management operations. The fact of the matter is that First Busey has around $13 billion in assets under care that generate annualized revenue of about $60 million. Their payment technologies business has also processed around $12 billion worth of payments in the trailing 12-month period leading up to this, with 42 million transactions processed over that time that have generated $23.7 million in revenue for the company.

First Busey Corporation

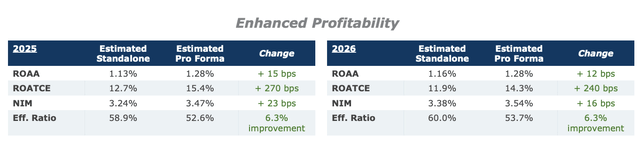

If everything goes according to plan, this transaction should prove to be positive for First Busey beyond any doubt. Using 2025 estimates, First Busey should achieve return on assets of about 1.13%. But as a combined company, this number should be about 1.28%. This might not sound like much, but when applied to the total assets both companies have, this disparity should translate to an extra $29.4 million in profits next year.

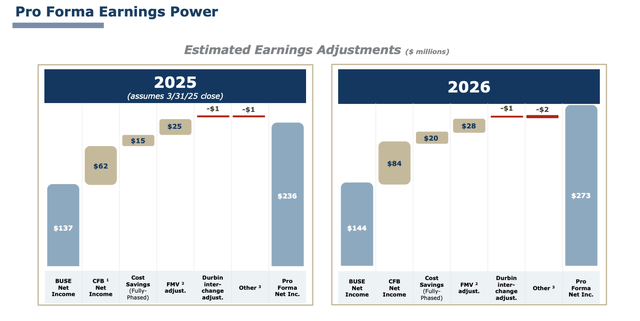

The return on tangible common equity should grow from 12.7% on a standalone basis to 15.4% combined. And instead of the $137 million in net income that First Busey should generate on its own, it should generate about $236 million in net profits next year. This is a little deceiving because this assumes a closing date for the end of March 2025. If we were to instead factor in the entirety of 2025, net profits would be even higher at $257 million. And if management is right, this number should grow further to $273 million in 2026.

First Busey Corporation

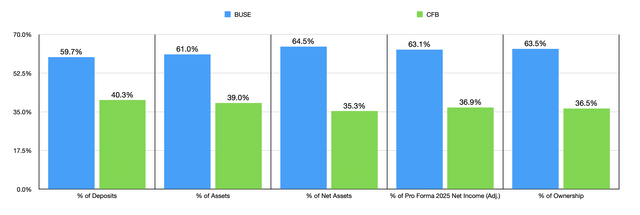

At first glance, this deal seems to be pretty fair for both parties involved. As I mentioned already, First Busey will end up with 63.5% of the combined business. Based on the most recent quarterly figures available, it is bringing only 59.7% of deposits to the table and 61% of total assets. But on a net asset basis, it is bringing 64.5% to the table. This is remarkably close to the ownership breakdown, with CrossFirst bringing 35.3% of net assets to the table while receiving 36.5% to the combined firm. Using the adjusted estimates for 2025, First Busey is bringing about 63.1% of total net profits to the combined business, with the remaining 36.9% of profits coming from CrossFirst.

Author – SEC EDGAR Data Author – SEC EDGAR Data

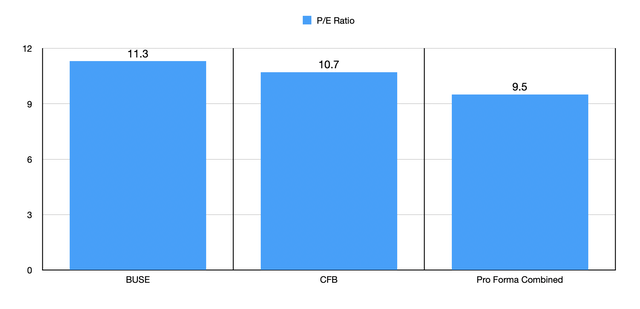

As even as this transaction initially appears, I think that First Busey is ending up with the better side of the deal. For starters, this transaction values CrossFirst, at its current valuation as of this writing, at about 10.7 times next year’s earnings. By comparison, First Busey is trading at 11.3 times next year’s earnings. But when you factor in synergies and other adjustments, the combined company is trading at a forward price to earnings multiple of 9.5. On a price to book basis, the stock is not cheap, but it’s also not expensive, with a multiple of 1.18.

Author – SEC EDGAR Data

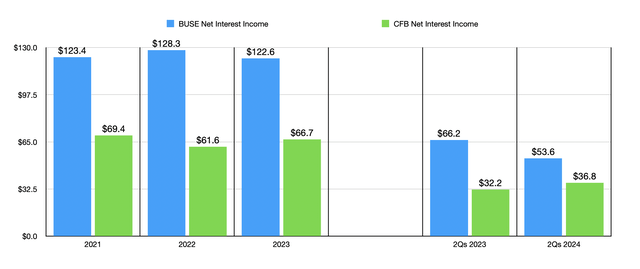

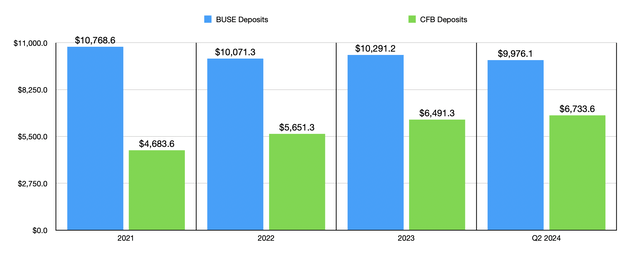

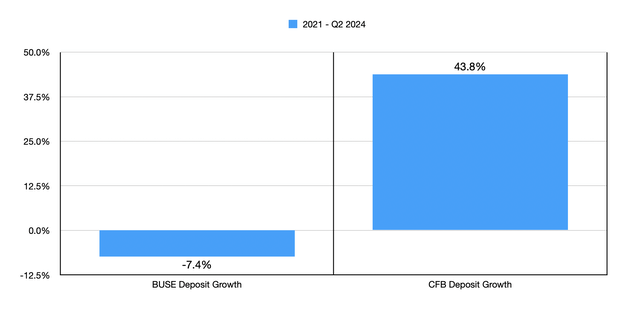

Outside of valuation, the two companies have a meaningfully different operating history. As you can see in the chart above, net profits for First Busey and CrossFirst have remained in a fairly narrow range over the last three fiscal years and into the current 2024 fiscal year. However, in the chart below, you can see a clear difference when it comes to deposit growth. There has been a general downtrend in deposits achieved by First Busey over the last few years. They totaled $10.77 billion in 2021. But as of the end of the most recent quarter, they came in at $9.98 billion. Meanwhile, CFB has been successful in growing deposits rather meaningfully. In the subsequent chart, you can see the total percentage growth in deposits for both companies from the start of 2021 through the end of the second quarter of this year.

Author – SEC EDGAR Data Author – SEC EDGAR Data

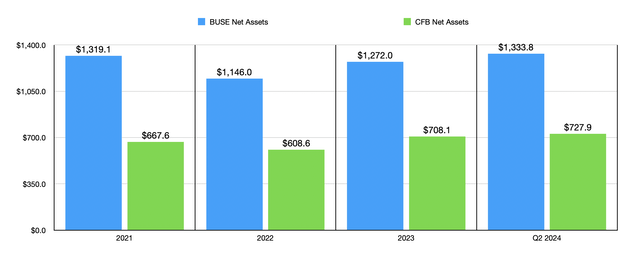

When it comes to net assets, the picture has been quite a bit lumpier. The general trend for both companies has been upward, which is definitely positive. But I wouldn’t say that there has been a meaningful distinction in this. Ultimately, during the window of time covered, CrossFirst has seen more impressive growth, with net assets expanding 9% from $667.6 million in 2021 to $727.9 million in the most recent quarter. By comparison, the increase achieved by First Busey has been more modest at 1.1% from $1.32 billion to $1.33 billion. Neither of these is terribly impressive, but it is clear who the winner is on this front.

Author – SEC EDGAR Data

Takeaway

All things considered, I find this transaction between First Busey and CrossFirst to be very interesting. Ultimately, I think that the winner from this is First Busey, especially when you consider the deposit history of the business over the past few years. However, I don’t think the picture looks awful for CrossFirst. Personally, I think its investors will probably be somewhat disappointed that they didn’t get a larger share of the pie. As a combined firm, I am cautiously optimistic. Because of the deposit issues associated with First Busey, I cannot rate the company anything better than a ‘hold’. However, the combined company would be a ‘buy’ in my book so long as we don’t see any further deposit deterioration, while CrossFirst on a standalone basis deserves a soft ‘buy’ rating.

Read the full article here