For nearly a year and a half, I have dedicated a good portion of my time to analyzing and understanding financial institutions better. For the vast majority of the 16 years that I have spent investing, I largely shied away from those firms. But because of the banking crisis that occurred last year, I could not resist the allure of them any further. Two banks that I have analyzed previously that I took rather neutral stances on were Independent Bank Group (NASDAQ:IBTX) and SouthState Corporation (NYSE:SSB). In the case of Independent Bank Group, shares of the business have seen upside of only 4.5% since I wrote about it in February of this year. That’s below the 7.2% increase seen by the S&P 500 over the same window of time. And since I originally wrote about SouthState Corporation in September of 2023, shares have seen upside of only 4.2% at a time when the S&P 500 has jumped by 20.9%.

This underperformance is obviously disconcerting, but not terribly surprising given the rating that I assigned both businesses. In May of this year, however, the management teams at both businesses agreed to a transaction that would see SouthState Corporation acquire Independent Bank Group in an all-stock deal that was initially valued at about $2 billion. The hope here is that, as a combined enterprise, additional opportunities can be had and value can be created. But looking at the big picture, I don’t have a great deal of hope of this coming to fruition.

While it is entirely possible that cost savings will come as a result of this maneuver, the downside for SouthState Corporation is that it is buying a bank that is, fundamentally speaking, quite a bit inferior to itself. This might seem like a blessing for shareholders of Independent Bank Group. At the end of the day, I maintain SouthState Corporation still warrants a ‘hold’ rating. Right now, Independent Bank Group offers only a 1% spread between its current price and its implied buyout price, which may seem to some a reason to justify a ‘sell’ rating. But given that its fortunes are tied to SouthState Corporation’s fortunes, keeping the firm a ‘hold’ makes sense as well.

A big bet on the south

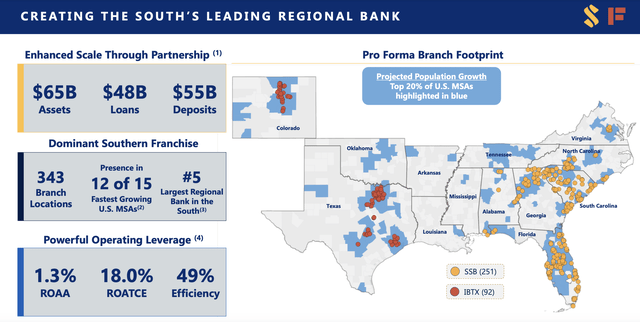

On May 20, the management teams at Independent Bank Group and SouthState Corporation announced that the two companies will be merging in an all-stock deal valued at nearly $2 billion. In short, for every share of Independent Bank Group that an investor has, they will receive, upon closing of the deal, 0.60 shares of SouthState Corporation. All combined, the institution will be quite large. Total assets of the combined enterprise, as of the date of the announcement, came in at $65 billion. This included $48 billion worth of loans. These are backed by $55 billion of deposits.

SouthState Corporation

Operationally speaking, the combined enterprise will be quite large, with 343 branch locations and a physical presence in 12 of the 15 fastest growing metropolitan statistical areas in the US. In fact, the combined firm will be the 5th largest regional bank in the southern portion of the country. Primarily, SouthState Corporation has operated in Florida, Georgia, and South Carolina. However, it does also have operations in other places like Virginia, North Carolina, and Alabama. By comparison, Independent Bank Group operates largely in Texas, though it does have locations elsewhere such as Colorado.

SouthState Corporation

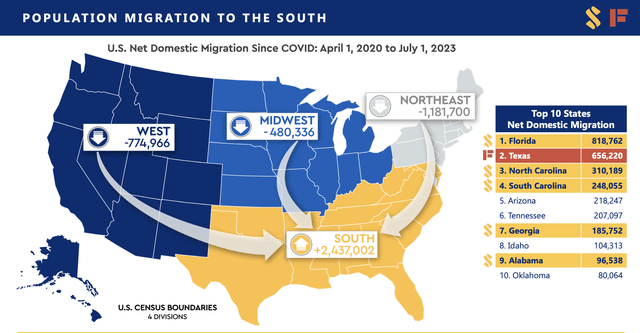

This transaction is a big bet on the southern portion of the country. And there is a good reason to be bullish about that in general. According to the management teams of both businesses, from April 1, 2020 through July 1, 2023, a net 2.44 million people have migrated into the southern portion of the country. Most of these have come from the northeast, though some have come from the Midwest and the western portions of the nation. The biggest beneficiary has been Florida, with net domestic migration of 818,762 people. However, Texas, where Independent Bank Group has a sizable presence, was the second largest beneficiary of this, with net domestic migration of 656,220 individuals.

The combination of these two businesses is expected to bring some pretty significant cost savings. If everything goes according to plan, total annualized savings should be around 25% of the non-interest expense that Independent Bank Group generates. This is based on projected non-interest expense for the year 2025. Management assumed, in this case, that annual non-interest expense would grow at about 3% per annum. If we remove certain one-time costs that Independent Bank Group incurred in 2023, and apply that 3% annual growth rate for two years, we get potential annualized savings of about $77.3 million on a pre-tax basis. Approximately half of these savings should be realized in 2025, with the rest sometime thereafter.

This won’t come without some meaningful costs. For starters, SouthState Corporation expects to incur around $175 million in pre-tax merger expenses. In addition to this, it expects to see write downs of certain assets, such as loans, securities, and debt, of roughly $438.8 million on a pre-tax basis. If we assume a 21% tax rate, the net pain will amount to approximately $346.7 million.

Author – SEC EDGAR Data

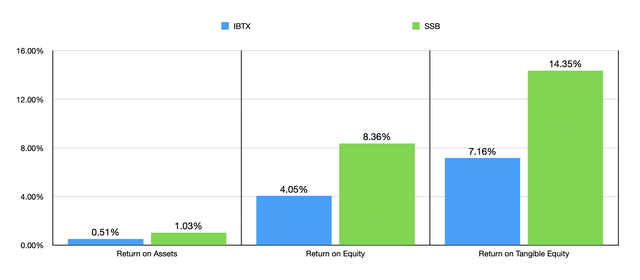

To be very clear, this transaction is not one of equals. For starters, SouthState Corporation is quite a bit larger than Independent Bank Group at this time. This is why shareholders of Independent Bank Group will only receive 24.7% of the combined business. The other 75.3% will be retained by current shareholders of SouthState Corporation. The companies are unequal not only because of size, but also because of overall quality. In the chart above, you can see the most recent calculations for their return on assets, return on equity, and return on tangible equity. Overwhelmingly, SouthState Corporation is the superior business.

SouthState Corporation

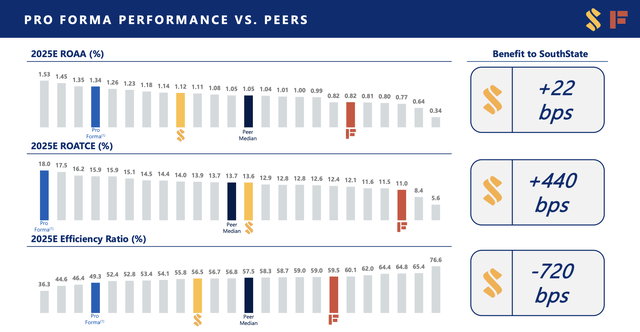

Now it is important to keep in mind that, when it comes to two of these metrics, return on assets and return on tangible equity, the firms have provided some alternative estimates. These estimates, as shown in the image above, factor in certain adjustments and project out to 2025 instead of using the most recent data provided by management. But even in this case, there’s a clear difference in quality. Overwhelmingly, SouthState Corporation remains vastly superior to Independent Bank Group on this front.

Author – SEC EDGAR Data

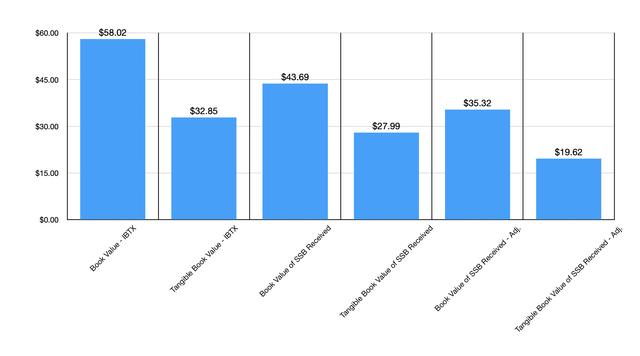

There is another way to gauge whether or not this transaction makes sense. This is to look at how much in equity and tangible equity Independent Bank Group is bringing to the table relative to what price SouthState Corporation is paying for it. For instance, as of the end of the most recent quarter, Independent Bank Group had a book value per share of $58.02. However, shareholders of SouthState Corporation are giving just $43.69 worth of book value for that. Even if we strip out the estimated $346.7 million in after tax write downs from the equation, Independent Bank Group would have a book value per share of approximately $49.65. This means that shareholders are still getting a haircut on a book value per share basis of 12%. In the chart above, you can see how this works out on a tangible book value basis as well. The bottom line from this, however, is that SouthState Corporation is getting a discount on the net assets that Independent Bank Group brings to the table. And this almost certainly is because of the lower quality of assets that we already talked about.

SouthState Corporation

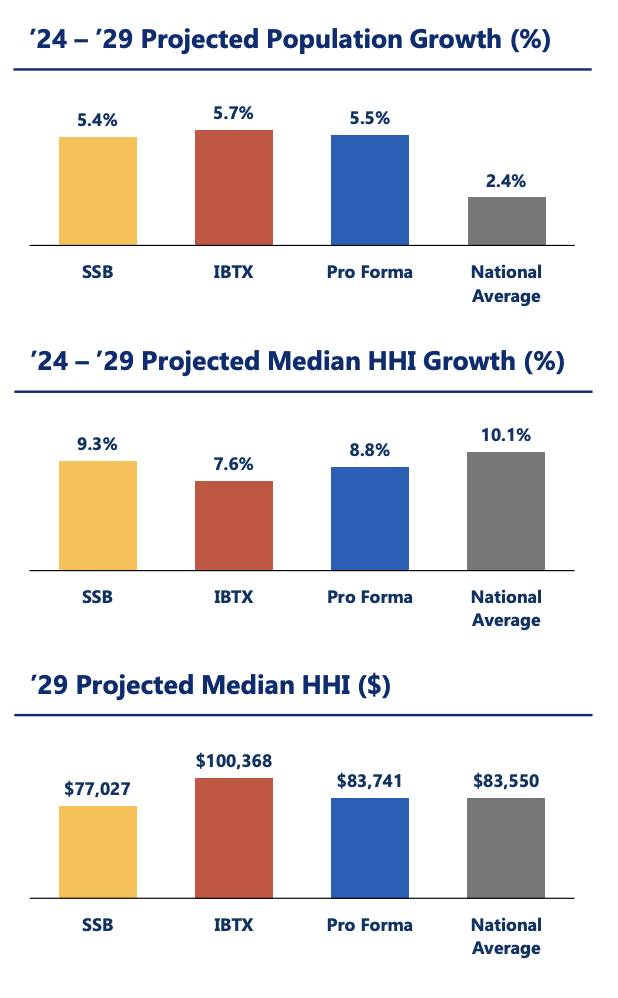

This is not to say that everything about this transaction is bad. For starters, the discount that SouthState is getting is a positive. In addition to that, Independent Bank Group does have some positive things going for it. It is projected, for instance, that from 2024 through 2029, median household income in areas in which Independent Bank Group operates will grow by about 7.6% annually. That is down from the 9.3% forecasted for SouthState Corporation. However, even by the end of that forecast period, Independent Bank Group will be operating in areas where the median household income of $100,368 is comfortably above the $77,027 that SouthState Corporation is exposed to. With higher median household incomes should, by definition, become greater opportunities.

Takeaway

The way I see things, while this is an interesting acquisition, it is one that puts all of the risk moving forward on SouthState Corporation. Fortunately, the business is getting net assets at a discount because of this risk and because of the lower quality of those assets. At the end of the day, this is not enough to change my own opinion of SouthState Corporation. Given the lower quality that Independent Bank Group brings to the table, it may seem odd that I’m not rating the business a ‘sell’. However, since it now seems tied to the performance of SouthState Corporation and offers a 1% spread between its price and the buyout price, keeping it a ‘hold’ as well makes sense.

Read the full article here