Summary

This post is to provide my thoughts on The Middleby Corporation (NASDAQ:MIDD) business and stock. I recommend a Buy rating as MIDD exceeded earnings expectations in 2Q with strong results in revenue and margins. Notably, inventories destocking pressure is easing, and sales segment seems to be reaching an inflection point. In addition, I expect revenue to accelerate in 2H23 as backlog normalize in 2H23.

Investment thesis

MIDD reported adjusted EPS of $2.47 per share for 2Q23, surpassing the consensus estimate of $2.35. This better-than-expected performance can be attributed to slightly improved revenue and EBITDA margins, although it was partially mitigated by increased tax rates.

Total sales for the quarter reached $1.04 billion, reflecting a 3% increase, driven primarily by robust results in the Commercial Foodservice [CF] and Food Processing segments [FP], while Residential sales lagged. Regarding cost, raw materials are expected to remain stable or slightly decrease from current levels. For margins, MIDD achieved adjusted EBITDA of $229 million, with a margin of 22.0%, outperforming the consensus forecast of $223 million with a 21.5% margin. This exceptional EBITDA performance was primarily driven by a 220bps expansion in CF margins, resulting from a shift towards higher technology solutions, increased manufacturing efficiency, and favourable price-to-cost dynamics. Additionally, FP margins expanded by 287bps due to the successful execution of larger projects and improved operational leverage.

During 2Q, inventory destocking had an impact on both the CF and Residential Kitchen [RK] segments, with RK being more significantly affected than CF, resulting in production falling behind sell-through levels. However, I hold the expectation that inventory patterns will likely return to their usual state by the end of 3Q. Looking at the broader market perspective, I believe that customers are gradually adjusting their personal inventory levels. This adjustment is driven by a return to their preferred MIDD products, especially considering that earlier COVID-related shortages had forced consumers into a ‘take what you can get’ mindset. Given these factors, I anticipate that sales will see improvements in the second half of 2023, as the headwind caused by the 2Q inventory destocking gradually subsides.

In the RK segment, both sales and EBITDA margin declined by 27% and 45% vs last year, respectively, in 2Q23. However, it’s worth noting that the segment appears poised for a positive shift in 3Q. This expected improvement is driven by a few key factors. Firstly, the return to regular inventory levels is anticipated to play a significant role. Additionally, there has been a noteworthy increase in order activity, especially in the core cooking and electric product categories. Regionally, the RK segment faces ongoing challenges in the US, while the UK, which contributes significantly to Europe’s RK sales, has been grappling with elevated interest rates and inflation. Nonetheless, there are some encouraging signs of stabilization. Looking ahead, I anticipate that RK sales will see a marked improvement in 4Q. Although I expect the margins for 3Q to be impacted by seasonal factors and absorption, they should remain above double digits.

Overall, despite the anticipated headwinds in 3Q, I hold the expectation that MIDD’s various segments are on the verge of reaching an inflection point beyond that period. This should lead to a more general improvement in sales as we move into 2H. In my view, even though MIDD has been dealing with a backlog that’s been higher than what we saw before the COVID-19 pandemic, there’s some optimism that things will start to get back to normal in the latter half of 2023. This should result in an annual decrease as we approach the end of the year. This positive change can be linked to improvements in their supply chain, better access to raw materials, and faster lead times. As a result, I observed that approximately 80% of MIDD’s product lineup is now aligning orders with sales in a more traditional way.

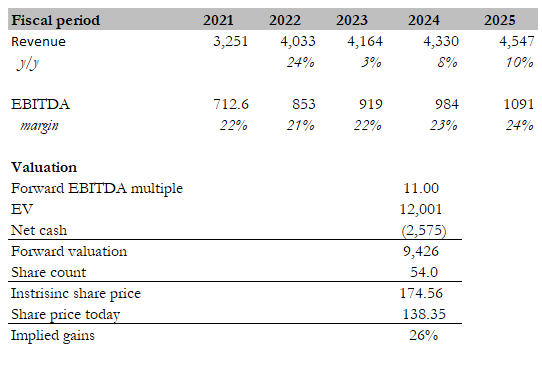

Valuation

Own calculation

MIDD delivered robust results in 2Q, driven by its impressive portfolio of leading brands across three closely integrated business segments. As the company continues its efforts to streamline inventory levels and with expectations of segment sales reaching a turning point in 3Q, followed by backlog normalization in 2H23, I anticipate a positive trajectory in revenue and growth for the latter half of the year.

Regarding profit margins, MIDD has been exhibiting healthy growth, currently standing at an impressive 22%. Given its strong performance in 2Q, the alleviation of supply chain challenges, and the favourable availability of raw materials, I foresee a continued expansion in margins. It’s worth noting that MIDD is currently trading at a forward EV/EBITDA multiple of 11x, whereas its peers, like Illinois Tool Works Inc (ITW), are trading at approximately 17x. Utilizing a conservative valuation multiple, I establish a target share price of $174.62, indicating a potential upside of 26%. In light of these considerations, I recommend a buy rating.

As for other valuation metrics, MIDD’s current forward P/E stands at 12.67x, notably lower than its historical average of 19.82x. In comparison, its peer company, ITW, is trading at a higher 21.78x. When considering the P/B multiple, MIDD is currently at 2.46x, again significantly below its historical average of 4.36x. In contrast, ITW has a P/B ratio of 23.27x.

Risk

The persistence of input cost inflation and ongoing supply chain difficulties might exert more extended pressure on profit margins than initially anticipated, particularly as MIDD strives to fulfil a historically high backlog that cannot be adjusted for higher pricing. While the fundamentals of the RK and FP segments demonstrated resilience during the pandemic, there may be constrained potential for demand growth beyond the existing backlog. Consequently, MIDD could face the risk of delivering underwhelming results if volumes in these segments decline earlier than anticipated.

Conclusion

MIDD demonstrates a promising path to recovery and growth. The company’s strong 2Q23 performance, exceeding earnings expectations, is driven by robust revenue and margin improvements in key segments, particularly Commercial Foodservice and Food Processing. While inventory destocking pressures impacted certain segments in 2Q, the expectation of returning to normal inventory levels by 3Q, along with increased order activity, suggests improved sales ahead. Despite challenges in the Residential Kitchen segment, there is optimism for a positive shift in 3Q and beyond. MIDD’s impressive profit margins, stable raw material costs, and efforts to streamline operations further contribute to its growth potential. With a forward EV/EBITDA multiple of 11x, compared to peers at 17x, there is a substantial upside potential, making a Buy rating compelling.

Read the full article here