Muni bonds have historically provided attractive tax-equivalent yields and lower default rates than traditional investment-grade bonds. Our approach to investing in mid-quality revenue bonds results in what we believe are attractive yields and total returns compared to traditional muni strategies.

Outperformance versus higher-quality munis

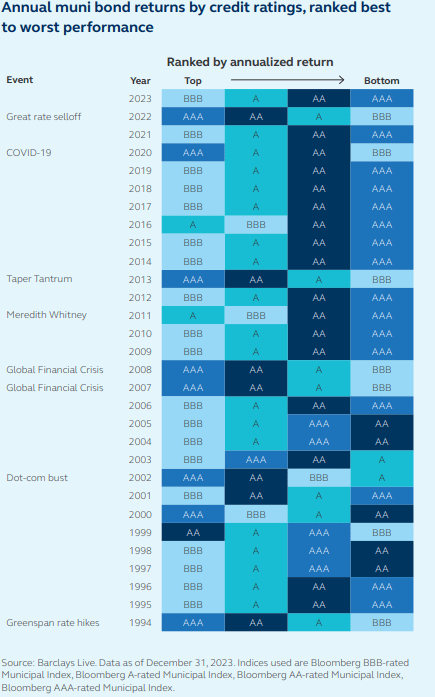

Within the muni market, mid-quality muni bonds have outperformed higher-quality muni bonds. Over the last 30 years, BBB- or A-rated munis have provided better annualized returns than AAA or AA munis, with BBB- or A-rated munis outperforming 21 out of the last 30 years.

Tax-equivalent benefit of mid-quality munis increases with tax rate

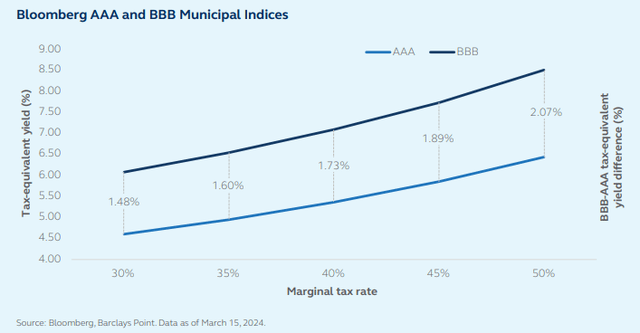

The benefit in additional tax-equivalent yield from mid-quality munis increases with an investor’s marginal tax rate. The yield advantage of BBB-rated munis compared to AAA-rated munis increases from 150 bps to 200 bps as the tax rate goes from 30% to 50%.

Revenue bonds have proven to be more attractive than general obligation bonds

We also have a preference for revenue bonds because they provide less sensitivity over a market cycle, independent rate setting ability, and better seniority than general obligation bonds. Over the last 44 years, revenue bonds have outperformed general obligation bonds 65% of the time.1

We believe this bias towards mid-quality and revenue bonds positions our portfolios to provide attractive relative yield and less sensitivity to business cycles than more traditional muni strategies. So far, 2024 is following historical trends with midquality muni bonds outperforming higher-quality muni bonds and revenue bonds outperforming general obligation bonds.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here