Introduction

Shares of The RealReal (NASDAQ:REAL) have risen 95% YTD. Despite the fact that the company continues to show improved profitability, I believe investors will need to wait for the next quarter’s results before deciding to go long. In my article, I would like to analyze current business trends, make assumptions about future financial results and evaluate the business.

Investment thesis

On the one hand, the company continues to demonstrate to investors the continuation of the trend towards improving the level of operating profitability of the business, which could serve as a significant catalyst for stock growth in the future. However, on the other hand, I believe that the company needs to demonstrate significant optimization of operating costs and improvement in unit economics in order to reach the break-even point, which, in my personal opinion, is one of the key risks for the investment case. In addition, the company continues to generate negative free cash flow and operating profit.

Company overview

The RealReal company operates an online marketplace for the resale of luxury goods (designer fashion apparel, watches, jewelry) for men and women. The main revenue segments are consignment revenue (74% of revenue), direct revenue (16% of revenue) and shipping services revenue (10% of revenue). The company operates in the US market.

2Q 2023 Earnings Review

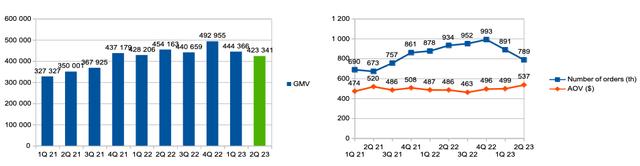

GMV (gross merchandise value) decreased by 6.8% YoY as a result of orders falling by 15.5% YoY, while AOV (average order value) increased by 10.5% YoY. Take rate increased from 36.1% YoY in Q2 2022 to 36.7% in Q2 2023.

GMV and number of orders & AOV (Company’s information)

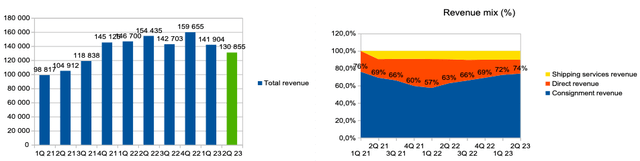

The company’s revenue decreased by 15.3% YoY. The largest contribution to the decline in revenue was made by the “Direct revenue” and “Shipping services revenue” segments, where revenue decreased by 51% YoY and 10% YoY, respectively, while revenue in the main segment “Consignment revenue” decreased by only 0.4% YoY.

Revenue and revenue mix (%) (Company’s information)

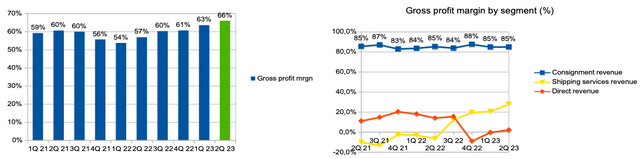

Gross profit margin increased from 56.8% YoY in the 2nd quarter of 2022 to 65.9% in the 2nd quarter of 2023 as a result of: 1) an increase in the share of the “Consignment revenue” segment in the company’s total revenue from 62.8% to 73.8 %, where the level of gross margin is the highest among all business segments 2) stable profitability in the main segment “Consignment revenue” and 3) increase in gross margin in the segment “Shipping services revenue” from -6.5% to 27.9%. You can see the gross margin details for each segment in the graph below.

Gross profit margin & gross profit margin by segment (Company’s information)

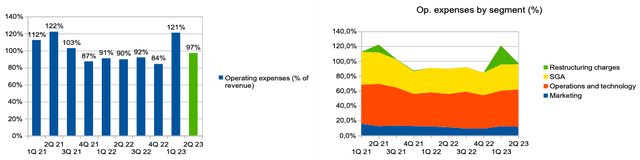

Operating expenses (% of revenue) increased from 89.8% YoY in 2Q 2022 to 97.1% in 2Q 2023 as a result of an increase in expenses for “operations and technology” from 44.9% to 50.1%.

Op. expenses (% of revenue) & op. expenses by segment (% of revenue) (Company’s information)

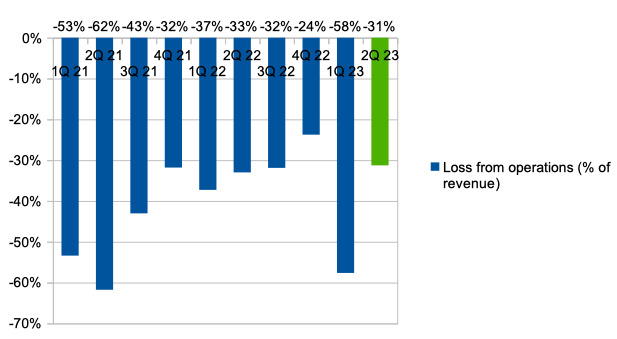

Thus, operating loss (% of revenue) decreased from 33.0% YoY in Q2 2022 to 31.3% in Q2 2023.

Loss from operations (% of revenue) (Company’s information)

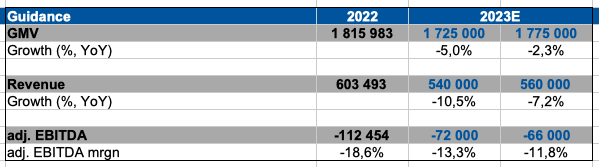

Moreover, the company provided guidance for 2023. Thus, management expects revenue to decrease by 2%-5% at the end of 2023, but the loss for adj. EBITDA (% of revenue) will decrease to 12%-13%.

Guidance 2023 (Company’s information)

My forecast

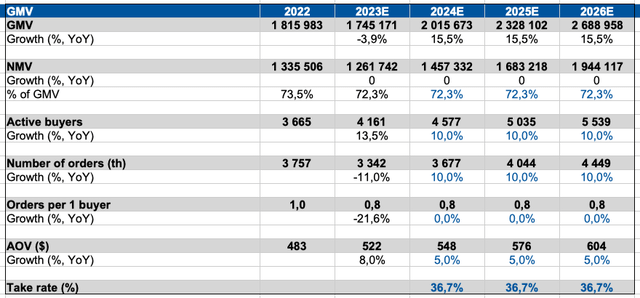

One of the key questions in a company’s investment case is whether the company is even capable of achieving operating breakeven in the future. Based on comments from management, company guidance, changes in business strategy and my own expectations, I made my own assumptions about future financial results. So, in my calculations, I assume that the company will continue to show an increase in the number of orders and the number of customers by 10% until 2026, while the average check will grow at 5%. As such, I believe the company will return to double-digit GMV growth in 2024. I based my forecasts for 2023 on the company’s guidance, the details of which I provided above in my article.

GMV forecast (Personal calculations)

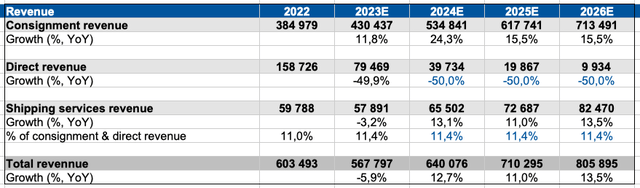

In accordance with the company’s strategy, I believe that the company will continue to actively reduce the share of revenue in the Direct revenue segment, while in the main Consignment revenue segment I expect continued growth due to a stable take rate at 36.7%.

Revenue forecast (Personal calculations)

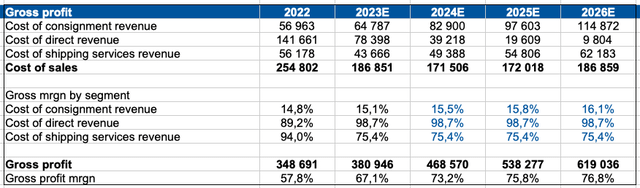

I forecast a gradual improvement in gross profit margin in the Consignment revenue segment, while in the Direct revenue and Shipping services segments I expect gross profit margin to remain at stable historical levels. So, according to my calculations, the gross profit margin could increase to 76.8% by 2026 due to an increase in the share of the “Consignment revenue” segment in the total business revenue.

Gross profit margin forecast (Personal calculations)

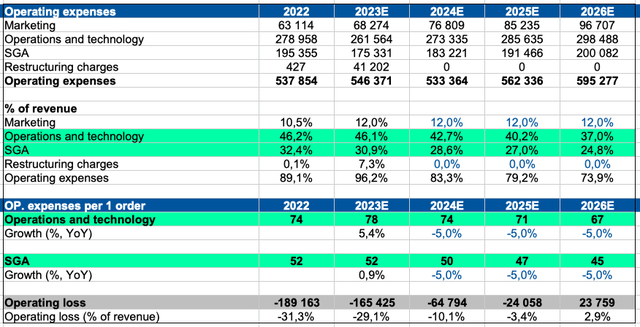

Next, I would like to note that forecasting operating costs is one of the key topics of my article. The largest portion of operating expenses falls on “Operations and technology” and “SGA”. For more accurate forecasting, I base it on unit economics. Thus, I expect that, per 1 order, the company will continue to demonstrate a decrease in costs for “Operations and technology” and “SGA” until 2026 due to an increase in business scale, an increase in the average bill and optimization of logistics processes.

At the moment, it is difficult to say how much the company will be able to reduce operating costs per order, so here I am relying solely on my own expectations. Thus, based on fairly positive preconditions for both business growth and the dynamics of reducing operating expenses, the company’s operating profit will continue to be in the negative zone until 2025.

Op. expenses & op. loss (% of revenue) forecast) (Personal calculations)

Risks

Revenue growth: a decrease in the number of orders, the emergence of new players in the luxury goods resale segment and a decrease in average order value may lead to a decrease in business growth rates in the coming years.

Margin: a decrease in take rate due to increased competition and deleverage due to a decrease in economies of scale may have a negative impact on the dynamics of the operating profitability of the business in the future.

Cash burn: the company’s operating income and free cash flow continue to be in negative territory, so the company may increase its debt load or issue additional shares if it fails to reach the break-even point, which could lead to both increased interest expense and dilution of its share. existing shareholders.

Drivers

Revenue: new revenue segments (advertising of third-party services on the platform), an increase in the number of orders and an increase in take rate may contribute to revenue growth in the coming years.

Margin: reducing the number of non-profitable positions on the platform, increasing the share of revenue from the consignment segment, realizing economies of scale and optimizing marketing costs can help improve profitability in the future.

Valuation

Below I would like to share my assessment of the company. I would like to highlight the fact that despite the high growth potential, in my assessment, I believe the company should demonstrate improved unit economics and significant improvement in operating margins, which could serve as a catalyst for stock growth in the future.

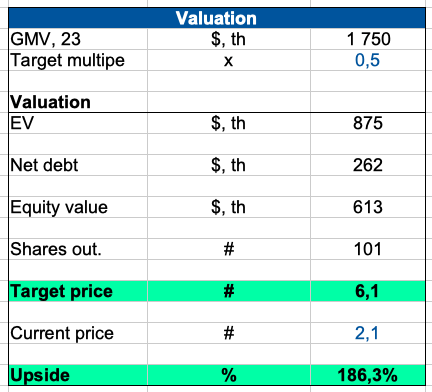

I prefer to use a multiple to value a company because valuation using the DCF model is too sensitive to inputs. Based on management guidance, I forecast GMV at $1.75 billion and use an EV/GMV multiple of 0.5x. On the one hand, the current multiple is relatively low, but on the other hand, I believe the company deserves a discount due to the size of the business, potential competition from large players and negative operating margins. Thus, according to my assessment, the fair price of the stock is about $6.1 with an upside potential of 186%.

Valuation (Personal calculations)

Conclusion

I like the fact that the company continues to reduce the share of direct business, increases the share of the consignment segment and the average bill, and also focuses on consumers who are less sensitive to rising interest rates. I believe that to achieve operating breakeven the company must continue to significantly reduce operating expenses, however, based on fairly positive assumptions, I do not expect the company to demonstrate significant improvements in the next 2 years. Thus, despite the high growth potential, at the moment my recommendation is Hold. I will be happy to change my recommendation to buy if in the next 3-4 quarters the company’s management demonstrates the sustainability of the trend towards improving the unit economics of the business.

Read the full article here