Investment Thesis

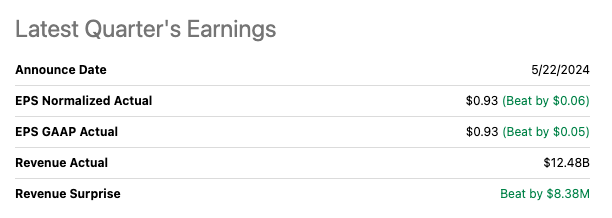

TJX Companies (NYSE:TJX), the parent company of discount retailers like TJ Maxx, Marshalls, and HomeGoods, reported a stellar first quarter for fiscal 2025. Both sales and earnings surpassed expectations, sending the company’s stock price soaring.

Sales grew by 6% YoY to $12.5 billion, exceeding estimates. This positive performance was driven entirely by an increase in customer traffic, with comparable store sales rising by 3%. Earnings per share also impressed, jumping 22.4% to $0.93 per share, exceeding expectations of $0.87.

SeekingAlpha

I believe the company’s strong performance can be attributed to several factors. Inflation is pushing consumers towards value-oriented retailers, making TJX’s offerings more attractive. Additionally, TJX has strengthened its relationships with brands, leading to a wider variety of quality products at lower prices. They’ve also cultivated a shopping experience that is seen as fun and trendy, attracting younger demographics with their “treasure hunt” approach as Ernie Herrman, the company CEO, described during the last earnings call:

I think what gives us a lot of confidence is we are the only retailer right now that I see that is able to take brands and fashion and quality and put all of that together in this treasure hunt format, remember, I’m talking about having good, better, best good, better, best, our range of all income and age groups, whereas all the other retailers, and I know, Matt, we’ve talked about this before, I really don’t know of any other retailer brick-and-mortar oriented that is creating a treasure hunt of this excitement level and entertainment level because they’re trading so broadly as we are.

Looking ahead, TJX expects continued growth in comparable sales and market share. The company is optimistic about its ability to deliver strong financial performance in the earning quarters of fiscal 2025.

In this article, I aim to find if TJX is a solid candidate for my value with potential portfolio. To accomplish this, I will explore various factors like Management effectiveness, corporate strategy, and valuation metrics to determine if its aligned with this investment style.

Management Evaluation

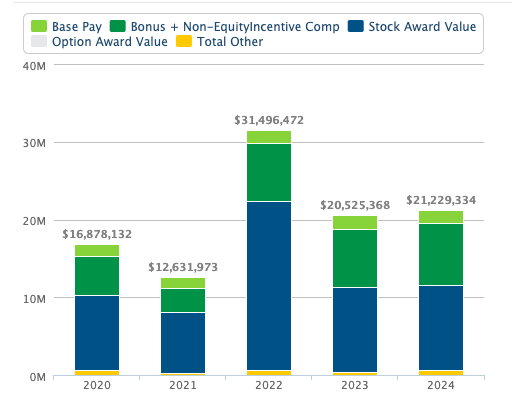

Ernie Herrman, CEO of TJX Companies since January 2016, has a surprisingly high approval rating on Glassdoor considering the nature of the business. This might be due to his long tenure with the company, where he started in 1989. However, his high stock award compensation raises some concerns.

Salary.com

During the last earnings call, Herrman highlighted the following key points:

- Growth Plans: TJX is focused on maintaining its value proposition through a balance of selective price increases and strategic buying to ensure they remain competitive.

- Customer Acquisition: The company is successfully attracting younger demographics while maintaining a healthy balance across age and income groups. This is likely due to their “treasure hunt” shopping experience and emphasis on good, better, best brand assortments.

- Market share: Herrman sound confident in the company’s ability to gain market share due to its flexible business model, particularly in HomeGoods, where they can adjust categories based on demand.

- Competition: While Herrman mention that competition does exist, he believes their strong vendor relationships and focus on value give them an edge.

- International expansion: the company seems to always be looking for expansion opportunities but remains tight-lipped about specifics until announcements are ready.

Glassdoor

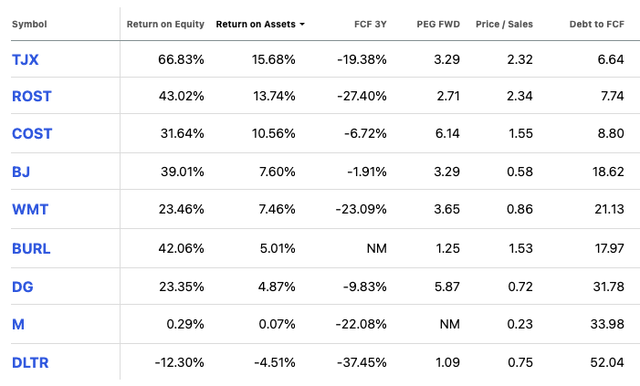

John Klinger, the CFO of TJX, has a long history with the company and has overseen a period of strong financial performance. Despite some recent soft revenue guidance which I believe is due to temporary economic factors, TJX remains profitable with a high ROA of 15%- vs a sector median of 4.20% and an ROE of 66%- vs sector median of around 12%. Their leverage levels are also low at a Debt to FCF of 6x, one of the lowest when compared to other competitors in the industry as highlighted below. During the earnings call Klinger pointed out to the following:

- Customer Growth: across different income levels

- Profitability: through expense management and inventory management

- Expansion plans: international segment is expected to reach its growth target at 8% and core business within Marmaxx remains strong despite weather challenges.

- Customer Experience: focus on remodels and shrink management. Also mentioned that despite not having a large penetration with their credit card like some competitors, they use various data sources besides credit cards to understand demographics and trends.

Overall, I find that TJX team appears well-positioned to maintain their leadership in the off-price retail sector. Their focus on a compelling value proposition, customer acquisition across demographics, strategic expansion, but particularly I find that their commitment to the brick and mortar shopping experience positions them for continued success in this niche sector where physical store sales are still happening.

However, I do believe, that their ability to successfully maintain this trend and balance it with the growing importance of online retail and potential short term economic headwinds will be crucial factors in the coming years.

Finally, I have confidence in the management due to the combination of tenure with the company and experience in the industry and due to their success in the last years I’m inclined to give management a “Exceeds Expectations”.

SeekingAlpha

Corporate Strategy

TJX Companies, known for TJ Maxx, Marshalls, and HomeGoods, focuses on global expansion as the leading off-price retailer. I find that their strategy revolves around:

- Geographic Growth: US, Canada, and Europe (with emphasis in Germany and the Netherlands)

- Treasure Hunt experience: offering a constantly changing variety of brand name apparel and homeware at significant discounts

- Transaction Growth: prioritize customer transactions rather than relying solely on higher spending per visit.

- Focus on value: strong value proposition for broad customer base

TJX Website

Here is a table I created with key differentiators between TJX and some companies in the industry offering similar services:

|

TJX Companies |

Ross Stores (ROST) |

Burlington (BURL) |

|

|

Off-Price Retailer Market Share |

68% |

22% |

10% |

|

Corporate Growth Strategy |

International expansion (US, Canada, Europe). Focus on transaction growth. |

Geographic expansion (US) caters to value-conscious consumers. |

Geographic expansion (US), focus on family shopping experience |

|

Advantages |

Strong brand recognition, diverse product mix (apparel, home goods) higher average customer spend. |

Strong customer loyalty, focus on value proposition. |

Wider variety of family apparel and home goods, focus on promotional pricing. |

|

Disadvantages |

Lower online presence compared to competitors. |

Less emphasis on home goods compared to TJX. |

Lower brand recognition compared to TJX and Ross. |

Source: From companies’ website, presentations, SeekingAlpha, Bloomberg

While TJX dominates the off-price market, competitors like Nordstrom Rack (JWN) and Saks Off 5th (private), which are a pending merger talks, offer distinct experiences by targeting different audiences who are more fashion conscious with a focus on clearance merchandise and more select product mix at a slight higher price. Further Ross Stores has less focus on home goods and Burlington a focus on family shopping. Another important distinction is that unlike its competitors, TJX has chosen to prioritize brick and mortar. Their online presence remains limited; however, their online selection is not as extensive. I believe this strategy is aimed at encouraging frequent visits to stores. However, this is a double edge sword, as it might put them at a disadvantage as online shopping continues to grow and younger generations become a larger part of their customer base.

At the moment, however, I believe their strategy is working as their profit margin remain high to other competitors and have low leverage which means they have the financial resources to spend on new shopping technologies.

Looking ahead, while TJX current strategy positions them well, my view is that their long term success hinges on adaptation. Their focus on geographic growth, “treasure hunt”, and value proposition creates a strong foundation. However, embracing online shopping through a more robust platform is essential to reach younger generations and increase their market share. Additionally, capitalizing on sustainability by integrating responsible sourcing practices can attract environmental conscious customers. By continuously adapting to the evolving retail landscape, TJX can solidify their leadership in off-price retail and expand their reach.

Valuation

TJX currently trades at around $112.21 The stock is up around 12% since its last reported earnings in mid-May and its hitting All-time highs. The stock is also up around 20% TR YTD.

Now, to assess its value, I employed a 11% discount rate, this rate reflects the minimum return an investor expects to receive for their investments. Here, I am using a 5% risk free rate, combined with the additional market risk premium for holding stocks versus risk free investments, I’m using 6% for this risk premium. While this could be further refined, lower or higher, I’m using it as a starting point only to get a gauge using unbiased market expectations.

Then, using a simple 10 year two staged DCF model, I reversed the formula to solve for the high-growth rate, that is the growth in the first stage.

To achieve this, I assumed a terminal growth rate of 4% in the second stage. Predicting growth beyond a 10-year horizon is challenging, but in my experience, a 4% rate reflects a more sustainable long-term trajectory for mature companies that should be close to historical GDP growth. Again, these assumptions can be higher or lower, but from my experience I will use a 4% rate as a base case scenario due to the nature of their business. The formula used is:

$112.21 = (sum^10 EPS (1 + “X”) / 1+r)) + TV (sum^10 EPS (1+g) / (1+r))

Solving for x = 18%

This suggest that the market currently prices TJX EPS to grow at 18%. According to Seeking Alpha analyst consensus EPS over the next 3-5 years CAGR at 8.21%. Therefore, it seems that TJX is overvalued on a fundamental basis and the market might be expecting that it will grow faster. However, this expectation of 18% growth might be unrealistic, that is the stock is overvalued by double the growth rate in EPS with a fair value of $63.55 on DCF basis.

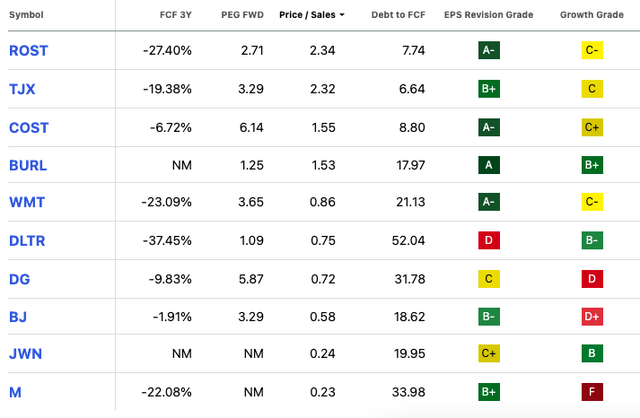

Further, I’ll also look at their forward price earnings to growth (PEG) ratio which sits at 3.29x -versus a sector median of 1.45x- implying the stock price is above the industry. In addition, their forward price to sales (P/S) ratio seems overvalued at 2.25x -vs 0.89x. However, when compared to a select group of companies, highlighted below, that are considered leaders in the industry, these mixed signals make more sense, and the company looks somewhat overvalued:

SeekingAlpha

Despite this overvaluation according to fundamental metrics like DCF and ratios, I believe this overvaluation is justified as TJX is more profitable and less levered than its main competitors. The higher profitability, growth prospects, and strong leadership makes the case for this higher valuation.

However, I do believe that as the company is hitting all-time highs to be more “positive cautious” as many expectations are already built into the current valuation. Therefore, patience might be rewarded by waiting for a weakness. Therefore, I am inclined to start my coverage of TJX with a “Cautious Buy”.

Technical Analysis

TJX has been on a positive momentum since they last reported earnings in mid-May. The stock has been hitting all-time highs ever since. However, the stock looks overvalued by now, on a technical basis, with its 1-year average RSI in overbought territory at 76 and below its 14-day moving average of 74 indicating the stock price might be changing trends.

TradingView

TJX has formed a strong support level at around $100 and the resistance level is hard to tell as the stock is breaking all time highs since its last earnings report and a price correction is possible. This is why I’m starting my coverage of TJX with a “cautious buy” and will consider a good opportunity near the $100 mark. Next earnings report is August 21st.

Takeaway

TJX Companies, impressed with a stellar first quarter. Strong financials, a focus on value, and a loyal customer base make them attractive. However, the stock’s all time high and comparable valuation metrics raises concerns about overvaluation. Experience leadership and a global expansion strategy bode well for the future. Their “treasure hunt” shopping experience is a strength, but a limited online presence compared to competitors is a weakness. Considering the potential overvaluation, I’m inclined to start coverage with a Cautious Buy approach as I will be a buyer on a weakness.

Read the full article here