TransMedics (NASDAQ:TMDX) continues to go from strength to strength, with its logistics business performing particularly well in recent quarters. While its core liver market in the US should continue to drive reasonable growth, TransMedics is planning on a number of clinical trials which could increase the penetration of its devices in heart and lung transplants. Given the company’s high valuation, new indications and geographic expansion are probably necessary for investors to see reasonable returns.

I previously suggested that while TransMedics was an extremely strong company with bright prospects, it appeared fully valued. The stock has nearly doubled since then, which is not that surprising given continued momentum in the business.

In the near-term, the stock will probably continue to perform well, regardless of valuation, while TransMedics continues to beat and raise. Caution is warranted, though, as the end market isn’t that large and growth in the core device business already appears to be moderating.

Market Conditions

Organ preservation devices are driving growth in the number of transplants performed and the distance that organs are transported. Heart, liver and lung organ transplant volumes increased 9% YoY in Q1. Only a teens percentage of transplants currently utilize an organ preservation device, which suggests that TransMedics still has a substantial growth runway.

A large amount of growth is already implied in TransMedics’ valuation, though, which, I believe, could be problematic. Including transportation and organ placement services, TransMedics’ addressable market is probably around 10 billion USD at the moment. The company’s serviceable obtainable market may only be around 3 billion USD, though, dependent on the extent that its devices can drive donor organ utilization. TransMedics can create solid returns for shareholders, but this will likely require the company to expand the market while obtaining a large market share with strong profit margins.

TransMedics Business Updates

TransMedics continues to rapidly build its logistics business, and so far, this initiative appears to be going very well. While the margin structure may not be as favorable as the rest of TransMedics’ business, transportation expands the company’s addressable market and strengthens its competitive position.

TransMedics had an average of 9 active aircraft during Q1 and ended the quarter owning 14. This number is expected to increase to 15-20 by the end of this year and 25-30 in the following year. TransMedics also continues to increase its logistics customer count, with 105 US transplant programs now using its service, up from 97 in Q4 2023.

TransMedics is planning on launching three new clinical programs, which could lead to increased adoption of its perfusion devices in heart and lung transplants. TransMedics wants to replicate its liver success in heart and lung and believes these programs will help it to achieve this.

TransMedics has developed a near physiologic OCS perfusion solution, which could lead to longer lung perfusion times. The company is targeting a minimum of 12-24 hours of OCS lung perfusion and plans on demonstrating this through a clinical trial with OCS NOP versus controlled cold static storage.

TransMedics also has 2 heart programs which aim to address different parts of the market. The first is OCS heart therapeutic warm perfusion for DBD hearts, which is targeting 12+ hours of OCS heart perfusion. The clinical trial will utilize TransMedics near physiologic OCS perfusion solution along with a proprietary metabolic enhancing therapeutic agent. The second program is aimed at OCS heart cold oxygenated perfusion for DBD hearts with a target time of less than 6 hours. This is a low-cost solution targeted at a sub-segment of the market. TransMedics anticipates initiating enrollment in all 3 programs within the next year. Given TransMedics current reliance on liver transplants, these trials will be important to the company’s growth in coming years.

Financial Analysis

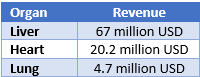

TransMedics generated 96.9 million USD revenue in the first quarter, an increase of 133% YoY, with robust growth across both products and logistics services. Product revenue was 61.3 million USD and service revenue was 35.5 million USD. It is worth noting that excluding the transplant logistics business, growth now appears to be fairly linear, although still currently extremely strong. TransMedics’ transplant logistics business generated 14.5 million USD revenue in the first quarter, up roughly 58% QoQ.

Table 1: TransMedics Q1 Revenue by Organ (source: Created by author using data from TransMedics)

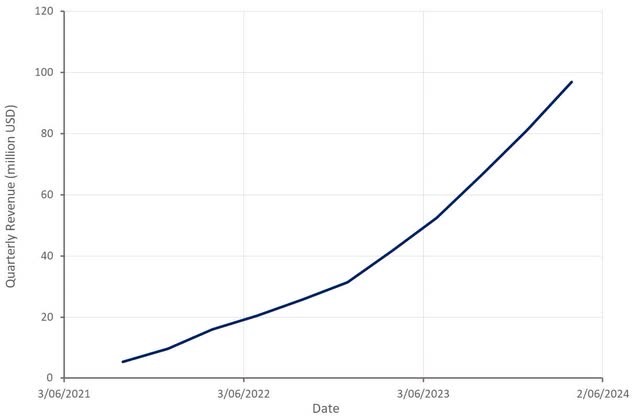

TransMedics now expects 390-400 million USD revenue in 2024, representing approximately 63% growth at the midpoint. This guidance seems extremely conservative though, and I would expect in excess of 450 million USD revenue for the full year. Looking further ahead, TransMedics is rapidly building a dominant position in the market and as a result will see its growth decelerate meaningfully over the next few years.

Figure 1: TransMedics Revenue (source: Created by author using data from TransMedics)

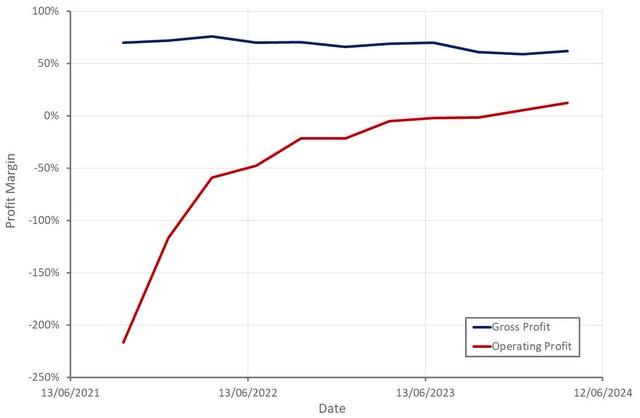

TransMedics’ gross profit margin was 62% in the first quarter, down from 69% in the prior year quarter. This decline is being driven by the rapid growth of the relatively low margin logistics business. TransMedics anticipates an improvement in gross profit margins over the next 12 to 18 months, though, which may imply a rapid deceleration in logistics growth.

Product margin was 77% in Q1, rebounding from 73% in Q4 due to the impact of a one-time expense. Service margin was 36% and continues to improve. TransMedics has not given a breakdown of service margins between aviation and other services but has stated that its aviation margin is lower. For comparison, Blade’s Medical segment profit margin is in the low 20% range.

TransMedics’ operating profit margin was approximately 12.8% in the first quarter, up almost 18% YoY, driven largely by operating leverage. I expect TransMedics’ operating profit margins to continue rapidly improving in coming quarters. This is important as high margins are necessary to justify TransMedics valuation.

Figure 2: TransMedics Profit Margins (source: Created by author using data from TransMedics)

Conclusion

TransMedics should continue to beat and raise in the near-term, supporting the company’s share price. I’m not sure that there is much room for multiple expansion at this point, though. Growth is being supported by the rapid expansion of TransMedics’ logistics business, which likely has far less favorable economics than the core device business.

While the results of planned clinical trials are some way off, positive outcomes will be significant for TransMedics, and could also provide the share price with a boost. Caution is warranted, though, as TransMedics growth rate will likely begin to decelerate meaningfully in coming quarters, which may not be looked upon favorably by investors.

Figure 3: TransMedics EV/S Ratio (source: Seeking Alpha)

Read the full article here