TransMedics (NASDAQ:TMDX) reported strong second quarter results last week and increased the full-year guidance by $40 million at the mid-point of the range. This was not very surprising considering the company’s beat-and-raise guidance history, but the magnitude of the beat and guidance raise was. The share price has advanced significantly since I initiated coverage last year, but I believe there is still significant upside left in the following years, as the stock is merely catching up to increased long-term growth expectations.

Strong execution and very conservative guidance – again

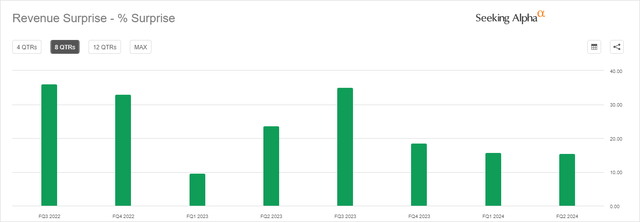

Second quarter results continued a long series of beat-and-raise quarters for TransMedics. Revenues were $15.4 million above the Street consensus, and non-GAAP EPS was $0.15 above the $0.20 consensus at $0.35.

Management continues to downplay expectations each quarter and then proceeds to deliver a big revenue beat and raise the full-year guidance the next quarter. The revenue beat was no less than 9.6% in the last 8 quarters.

Seeking Alpha

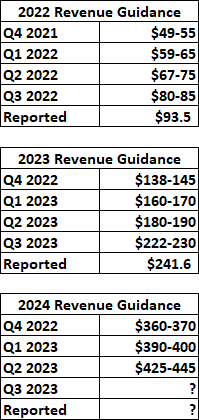

And on the full-year revenue guidance side, in the picture below, you can see the quarterly progression since Q4 2021 and how the actual revenues looked like in 2022 and 2023. The company seems on track to do the same in 2024.

TransMedics earnings reports

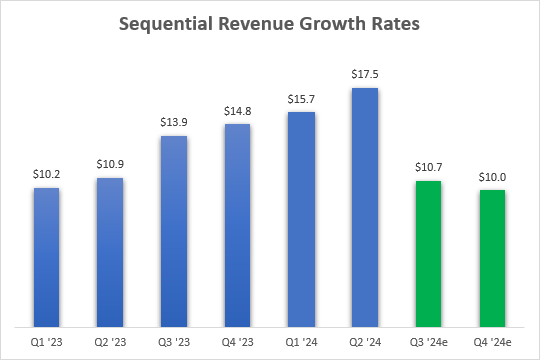

I expect 2024 revenues to exceed $470 million, and I do not believe this is a high bar considering the sequential growth rates since the start of 2023, and they would need to be around $10 million a quarter in the second half of the year for total revenues to exceed $470 million.

TransMedics earnings reports, author’s estimates

On the Q2 earnings call, management noted two factors that added to their conservatism for the full-year revenue guidance range. The first one is the expected routine maintenance for several of the aircraft, which they say could temporarily limit the pace of growth of logistics revenue in the next two quarters. The second but minor one is that the guidance factors some potential ex-U.S. revenue variability. I think this continues to reflect their very conservative nature, and that, considering the increased number of planes compared to the start of the year, that logistics revenues will continue to ramp nicely even if a few planes are down for maintenance during the second half of the year.

Improved uptake in heart transplants and continued strength in liver transplants drove the Q2 performance

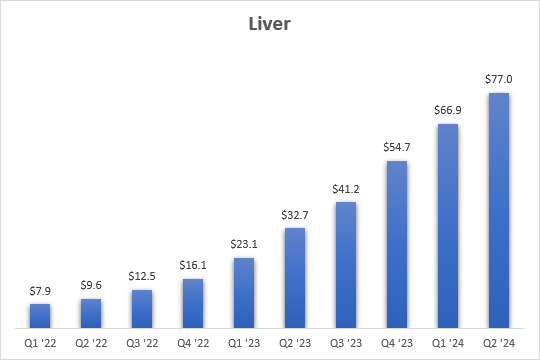

The liver transplant segment continues to be the main growth driver for TransMedics and a steady performer. Q2 revenues of the liver segment grew 136% Y/Y to $77.2 million.

TransMedics earnings reports

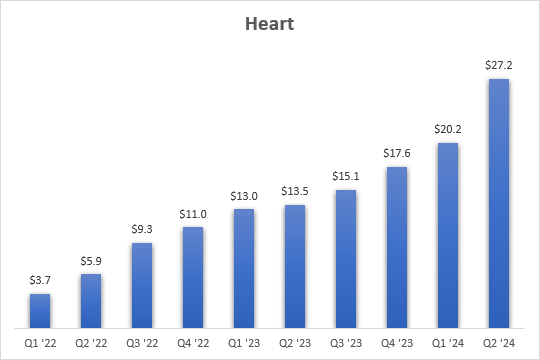

Heart transplant revenues were above trend in the second quarter, with revenues increasing 34% sequentially and 102% Y/Y to $27.2 million.

TransMedics earnings reports

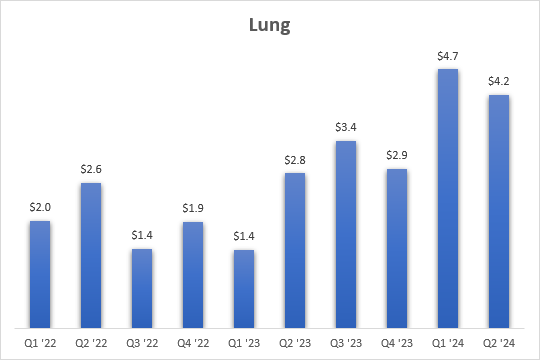

Lung continues to be the weakest and smallest part of the business and while it delivered healthy Y/Y growth of 51% in Q2, revenues declined sequentially from $4.7 million in Q1 to $4.2 million in Q2.

TransMedics earnings reports

The numbers above are for the U.S. business. The international business remains a small part of the total business, and revenues grew 34% Y/Y to $4.7 million.

I have no complaints relative to expectations, and TransMedics is making additional steps that should boost the medium- and long-term growth of the heart and lung business, by planning to start three clinical trials in 2025.

The first two should start in early 2025 with new OCS (Organ Care System) lung and OCS heart, respectively, and include new perfusions solutions and new circuit designs.

The company says that preclinical data demonstrated successful maintenance of donor lungs and hearts on OCS perfusion for more than 24 hours with “significantly lower edema formation compared to controlled cold storage.” Management says that this would be a critical milestone and that it should enable what it already achieved with OCS liver and help move to morning transplants for OCS lung and heart. This was also achieved along with significant reductions in ischemia reperfusion injury for both organs compared to static cold storage, and with improvements in the overall operational performance throughout 24 hours.

Successfully completing these trials should reinvigorate the growth of heart and lung transplants in 2027 (and possibly as soon as 2026) and drive the company toward its 2028 goal of facilitating 10,000 transplants a year.

Logistics business increasingly looks like an excellent decision

The formation of the logistics business a year ago is increasingly looking like an excellent decision. Logistics revenues in the last four quarters were $2.1 million, $9.2 million, $14.5 million, and $19.1 million, respectively, and TransMedics was able to cover 59% of the total transplants in the second quarter with its internal logistics platform, up from 49% in the first quarter and from 0% in the second quarter of 2023.

The company purchased one aircraft in the second quarter and another two in July to bring the total number to 17, and this is already within the targeted range of 15-20.

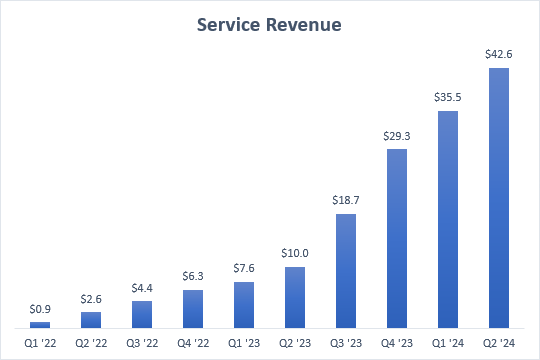

The formation of the logistics business continues to boost the growth rates of services revenues, and they remained in the 300%+ range for the fourth quarter in a row.

TransMedics earnings reports

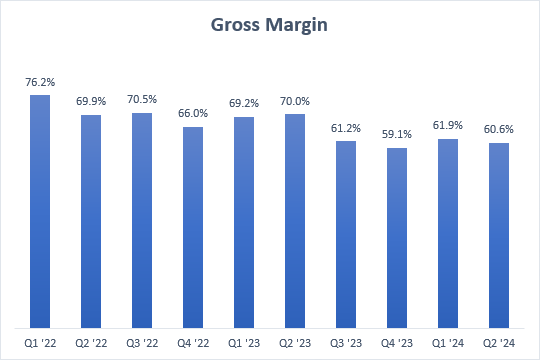

The heavy investments and the increasing contribution of the logistics business continue to weigh on the company-wide gross margin, and it fell sequentially from 61.9% in Q1 to 60.6% in Q2.

TransMedics earnings reports

However, this should not be concerning as the decrease was driven by the significant expansion of the logistics infrastructure to support long-term growth – the pilot crew size doubled sequentially and since it takes 6–8 weeks for them to be fully trained and operational, the positive effects will only be seen in the following quarters. While there should be some sequential gross margin variations in the following quarters, I believe the Q2 gross margin is the lowest we will see this year.

Conclusion

Strong execution and management conservatism are a recipe for success. TransMedics is doing a good job managing expectations since the Street consensus is most often largely in line with the guidance range that management provides, and this leaves room for significant outperformance as the year progresses.

A case in point is the company’s long-term guidance of reaching 10,000 transplants in the U.S. in 2028 and the Street consensus for 2028 being at $1.01 billion. If this goal is reached, U.S. revenues should be above $1.5 billion, assuming modest price inflation and internal logistics covering the majority of the transplants, and there should also be some additional contribution from ex-U.S. markets. And I would not be surprised if the 10,000-transplant goal is exceeded in 2028, especially if the new trials in heart and lung are successful, as I believe they would lead to significant growth acceleration of these two segments.

The stock has more than doubled from my initiation article last year, but it is merely catching up to the increased growth expectations (for example, the 2024 revenue consensus in late July 2023 was $250 million and only $180 million in early 2023) and I continue to see the company as very well-positioned for significant growth in the following years.

Read the full article here