Business Development Companies (i.e., “BDCs”) (BIZD) can be a great investment for passive income investors for many of the same reasons why Real Estate Investment Trusts (i.e., “REITs”) (VNQ) are so popular with the same crowd:

- They are exempt from corporate taxation, leaving more profits for shareholders instead of Uncle Sam.

- They invest in well-diversified portfolios of generally defensive, stable cash-flowing investments (in this case, primarily senior secured loans instead of real estate in REITs).

- They are professionally managed, enabling them to access capital at costs that private investors could not achieve, invest in opportunities that individual investors could never dream of getting in on, and deal with problematic investments with a level of skill and resourcefulness that is tough to match as a non-professional individual investor.

- They pay out very large dividends thanks to the requirement that they distribute at least 90% of taxable income to shareholders.

However, in some ways, BDCs are even better passive income investments than REITs. While REITs do benefit from the appreciation of their underlying real estate whereas BDCs generally do not enjoy that benefit since they primarily invest in loans, BDCs benefit in other ways:

- Senior secured loans are oftentimes even more defensive than some types of real estate leases.

- Since BDCs do not get to depreciate their assets, more of their cash flow counts as taxable income, forcing them to pay out even higher amounts of their cash flow to shareholders, leading to higher dividend yields relative to most REITs.

- BDCs all publish their NAV per share, making valuations much more transparent and easier to measure and compare than in the REIT sector.

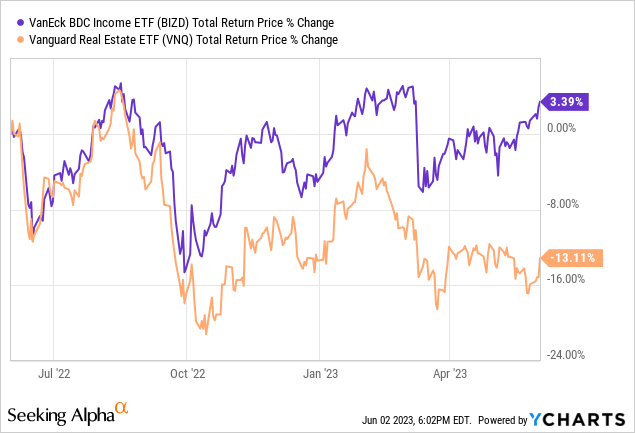

- BDCs primarily invest in floating rate loans, making them much better suited to a rising interest rate environment than most REITs. This has been made painfully obvious for REIT investors over the past year:

Recently, Blackstone President & COO Jon Gray – President & COO of ~$1 trillion alternative asset manager Blackstone (BX) – recently made some very bullish comments on the BDC sector in the context of explaining why they are investing tens of billions of dollars in them and other similar direct lending products, showing how they are in much better shape than banks (KRE)(KBE) at the moment:

if you looked at Credit Suisse (CS) or First Republic or SVB, these institutions were anywhere from 12 to 20 times leveraged. If you look at our nontraded BDC BCRED, it’s 1 times leveraged…[there also] tends to be a mismatch of assets and liabilities. I mean, the unfortunate irony of SVB and First Republic is they didn’t have any credit losses. They owned US treasuries and super prime mortgages, right? But they had a mismatch. We don’t have products with hourly deposits available, we’re very conscious of how we set these things up.

He makes an excellent point here that is often underappreciated about BDCs. In addition to the aforementioned pros of BDCs, another big one – especially relative to banks – is that they have very well-structured balance sheets. In addition to carrying much lower leverage than banks, they also balance their interest rate exposure in such a way that they can make money when interest rates rise and when interest rates fall. Moreover, they are generally set up such that rising rates are a tailwind to profit margins, which helps to compensate for the typical rise in counterparty distress in rising rate environments. This makes them an all-weather investment of sorts.

With this bullish view of BDCs in mind – especially in the current environment where banks are facing distress – we recently sold one of our banks at a huge profit and recycled the capital into one of our favorite BDCs of the moment.

Here are two of our six favorite BDCs right now:

#1. Ares Capital Corp (ARCC)

ARCC recently reported Q1 results. Highlights from the quarter included:

- NAV per share increased by $0.05 sequentially, due to a combination of unrealized gains in the portfolio as well as some retained earnings after paying out dividends.

- The leverage ratio improved considerably sequentially, from 1.26x at the end of Q4 2022 to 1.09x as of the end of Q1. The net interest margin also improved by 10 basis points to 750 basis points, which is 90 basis points better than FSK’s for example. This is largely due to the fact that ARCC has a greater percentage of fixed rate debt on the obligations side of its balance sheet, which means that when interest rate rise, its net interest margin will expand more rapidly than FSK’s will, whereas FSK’s net interest margin will contract more slowly than ARCC’s will if/when interest rates begin to fall again.

- The dividend was well covered (~1.24x) by net investment income, combining with the spillback income to provide a stable dividend outlook.

- Non-accruals continued to creep higher, but remained at a very low 1.3% of fair value, reflecting the company’s quality underwriting ability.

ARCC continues to be a steady-as-she-goes dividend payer and wealth compounder with an excellent track record, top-notch management, and a solid investment grade balance sheet. The current double-digit yield looks sustainable for the foreseeable future as well. While ARCC is only trading at a very slight discount to NAV, its long-term track record of growing NAV per share and its sustainable and attractive double-digit current yield make it an attractive Buy at the current valuation. You can read our full investment thesis here and our recent exclusive interview here.

#2. Blackstone Secured Lending (BXSL)

Given our quotation of BX’s President earlier in this article, it only makes sense that we mention their publicly traded BDC – BXSL – as one of our top picks. BXSL’s recently reported Q1 results were strong, with highlights including:

- Net investment income increased from $0.90 to $0.93 sequentially and by 52% year-over-year, thanks to rising interest rates.

- NII easily covered the regular dividend of $0.70 by 1.33x, combining with BXSL’s conservatively positioned investment portfolio of almost all senior secured debt to make BXSL’s dividend arguably the safest in the sector.

- The leverage ratio at quarter-end was 1.31x, which remains a bit elevated, but given the conservative nature of the portfolio and the $1.2 billion in liquidity, the balance sheet remains in solid shape.

- The company remains very well positioned to deal with higher for longer interest rates, thanks to the fact that 97.9% of the portfolio is invested in first lien, senior secured debt and 99.9% of debt investments are floating rate at a 45.2% average loan to value.

- Underwriting performance also remains very strong, with a mere 0.07% non-accrual rate of fair value.

While BXSL only currently trades at a small discount to its NAV per share, the strength of the portfolio, the well-covered 10.9% forward dividend yield, strength of the portfolio underwriting performance and positioning, and the competitive advantages provided by BXSL’s relationship with BX, it definitely warrants a Buy rating in our view. You can read our full investment thesis here and our recent exclusive interview here.

Investor Takeaway

BDCs can be exceptional passive income investments, especially when done prudently. While not all BDCs are well run, ARCC and BXSL are among the very best thanks to the competitive advantages derived from their affiliation with experienced and large-scale asset managers, their well-diversified portfolios with a focus on senior-secured floating rate loans, their strong underwriting performance, and healthy dividend coverage ratios that imply investors can count on their dividend payments even if the economy hits a bump in the road.

As a result, we are buying shares in these BDCs along with the four others in our portfolio and are locking in attractive double-digit yields in the process.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here