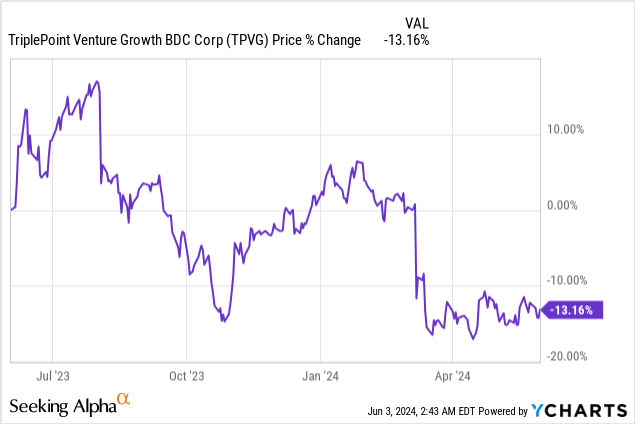

TriplePoint Venture Growth BDC (NYSE:TPVG) is most likely headed for a dividend cut in the near term as the company’s net asset value and balance sheet quality continued to suffer in the first fiscal quarter. Although the BDC supported its dividend of $0.40 per-share quarterly with NII, there is practically no dividend safety left for TriplePoint Growth at this point. For those reasons, and considering the fact that the BDC continued to report investment losses in Q1’24, I believe the risk profile is skewed to the downside, and I am changing my rating to sell!

Previous rating

I rated shares of TriplePoint Venture Growth a hold in March as the company reported a drop in its non-accrual percentage (due to realized losses) and because the BDC supported its dividend with net investment income: Should You Be Worried About The Dividend In 2024?

Since then, however, the fundamental situation for TriplePoint Venture Growth has deteriorated further: the non-accrual percentage increased significantly in Q1’24 and the BDC suffered further investment losses. As a result, the dividend safety eroded and TPVG just barely managed to support its dividend with net investment income in the last quarter. As a result, a dividend cut in the next 1-2 quarters is my expectation. For those reasons, I am down-grading TriplePoint Venture Growth from hold to sell.

Why a dividend cut seems likely in the next 1-2 quarters

TriplePoint Venture Growth is a niche BDC with a core focus on a few sectors, such as technology and life sciences. The BDC continues to suffer from bad investment decisions of the past, which caused a spike in the non-accrual percentage and in the amount of non-performing loans.

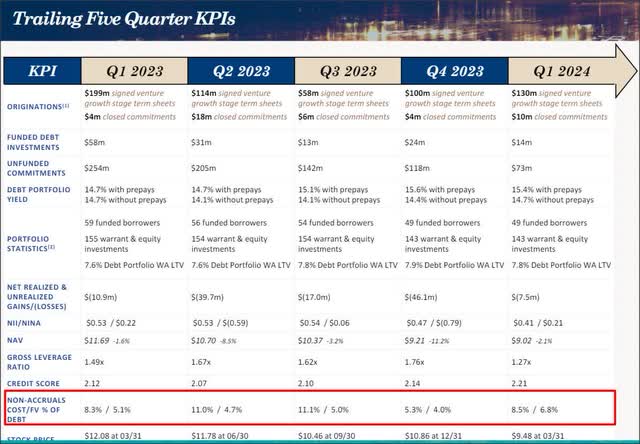

As a result, TriplePoint Venture Growth is facing considerable pressure on its net investment income, and the company continues to charge off investments at a fast pace. In the first fiscal quarter, TriplePoint Venture Growth’s non-accrual percentage surged to 6.8%, showing an increase of 2.8 PP quarter over quarter. At the same time, the BDC realized another $7.5M in investment losses, which caused a drop in the company’s net asset value as well.

TPVG

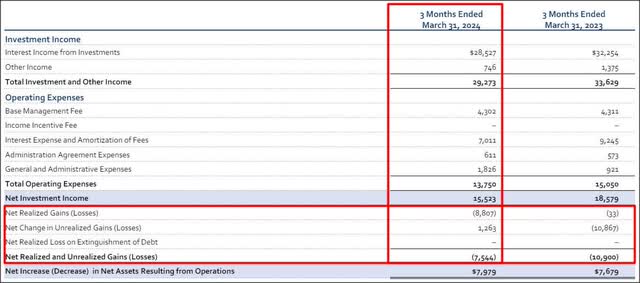

TriplePoint Venture Growth’s net realized investment losses of $8.8M were chiefly linked to two portfolio companies. According to the company’s 10Q, it had investments in 5 portfolio companies on non-accrual, representing a fair value of $47.1M. Because of the sharp increase in non-performing loans in the last year, TriplePoint Venture Growth suffered a significant contraction in its net investment income… and which therefore explains the declining safety margin when it comes to the BDC’s dividend. In Q1’24, TriplePoint Venture Growth generated $15.5M in net investment income, showing a decline of 16%. These problems are not driven by market factors, but by the company’s previous investments and the resulting surge in the non-accrual percentage.

TPVG

Weakening distribution coverage profile

In addition to concerns about TriplePoint Venture Growth’s loan quality and investment losses, there is one more pressing issue that indicates that shareholders will see a dividend cut in the near future: weakening distribution coverage.

TriplePoint Venture Growth’s portfolio assets (those that are performing) generated $0.41 per-share in net investment income compared to $0.53 per-share in the year-earlier period. This (22.3%) decline in NII is attributable exclusively to investment underperformance of TriplePoint Venture Growth’s loans.

Since the BDC is paying $0.40 per-share quarterly in dividends, the BDC only had a distribution coverage ratio of 1.03X (compared to 1.29X in FY 2023). TriplePoint Venture Growth did not yet fail to support its dividend with NII, but it is very close. Only one more underperforming investment (which is not that unlikely to happen given TriplePoint Venture Growth’s non-accrual trajectory) and the BDC would no longer cover its dividend with NII. Currently, shares of TPVG yield 17%, which in itself is a clear sign of distress.

Deteriorating net asset value trend for TPVG

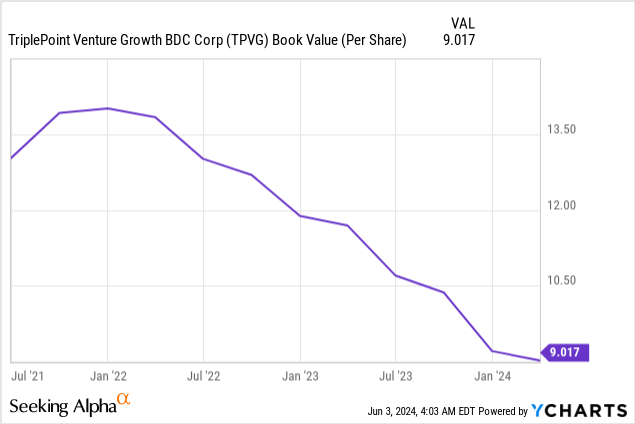

TriplePoint Venture Growth’s bad investment decisions of the past have led to a significant number of losses for shareholders in terms of net asset value as well. As of the latest quarter, TriplePoint Venture Growth had a net asset value of $9.02 per-share, showing a massive 23% decline compared to last year. The longer-term book value per-share growth record is also not exactly looking great…

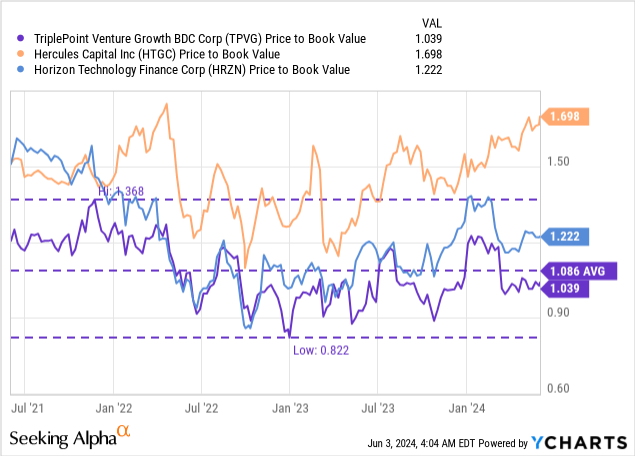

Given this track record, I am actually surprised that shares are not trading at a (large) discount to net asset value. Shares of TPVG currently trade at 1.04X book value, below the 3-year average price-to-book ratio of 1.09X, but still at a premium. Hercules Capital (HTGC) and Horizon Technology Finance (HRZN), close rivals in the tech-focused BDC niche, are priced at higher P/NAV ratios, largely because they don’t have TPVG’s non-accrual problems. Hercules Capital especially is flying above the entire BDC market due to strong business performance, strong dividend coverage and exemplary balance sheet quality: Solid 10% Yield, But Sky-High Valuation.

Given the risk to the dividend for TPVG, I would not be a buyer here at this point, but if I were I would surely ask for at least a 10% discount to net asset value in order to be properly compensated for the elevated dividend risk. This is a subjective discount that I apply here, given the large amount of loan problems in the BDC’s portfolio. A 10% discount to NAV, given TPVG’s sky-high non-accrual percentage, implies a potential buy price of $8.11 per-share.

Risks with TriplePoint Venture Growth

The risks here are obvious: a combination between persistent investment losses due to poor underwriting, a higher non-accrual percentage (an indicator of future loan charge-offs), a falling net asset value and evaporating excess distribution coverage are all reasons to suspect that TriplePoint Venture Growth will cut its dividend in the next 1-2 quarters.

Closing thoughts

TriplePoint Venture Growth has been a promising investment for dividend investors in the past when the BDC’s portfolio was performing much better and when the company offered investors a high degree of excess distribution coverage. These times are over now, obviously, and it is only a question of time until the dividend gets cut, in my opinion. With just 1.03X distribution coverage, it is highly likely that the BDC will soon cut its distribution, which may negatively affect the company’s valuation factor. The odds at this point, I believe, are stacked against TriplePoint Venture Growth and dividend investors should avoid the BDC’s massive 17% yield at all costs.

Read the full article here