Author’s note: This article was released to CEF/ETF Income Laboratory members on April 23th.

Pacer has a suite of Trendpilot ETFs, each of which uses a rules-based strategy to alternate exposure between treasuries and other assets, generally equities. These ETFs have generally underperformed in the past, as they have failed to successfully time the market.

The Pacer Trendpilot Fund of Funds ETF (NYSEARCA:TRND) invests in five different Trendpilot ETFs, and has also underperformed relevant benchmarks since inception, for the same reasons. TRND’s strategy has not worked in the past, and I have no reason to believe it will work in the future. As such, I see no reason to invest in the fund.

TRND – Overview and Strategy

TRND invests in the following five ETFs.

TRND

Each of the ETFs above invests in the underlying holdings of their respective index and / or treasuries. In very simple terms, each ETF tracks their respective index when prices are going up, goes 50% – 50% as these decline, and goes 100% treasuries when losses start to mount. These are explicit, quantitative strategies, with each ETF defining the exact conditions or triggers for switching assets or asset weights. For their treasury holdings, the Pacer Trendpilot US Bond ETF (PTBD) chooses medium-term treasuries, while the other four funds focus on t-bills.

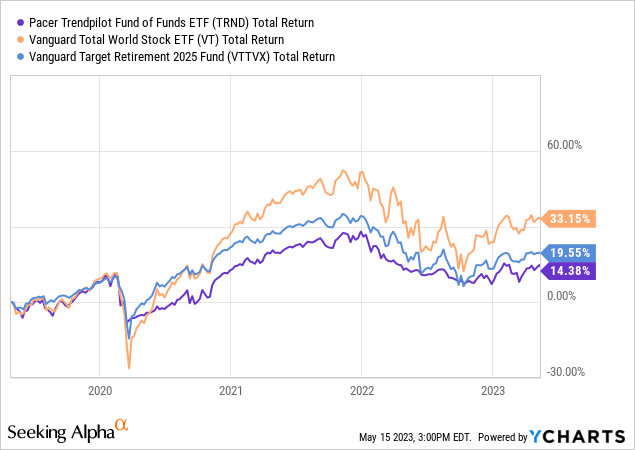

TRND itself focuses on U.S. equities, with these accounting for 60% of fund assets. International equities and bonds account for the rest, 20% each.

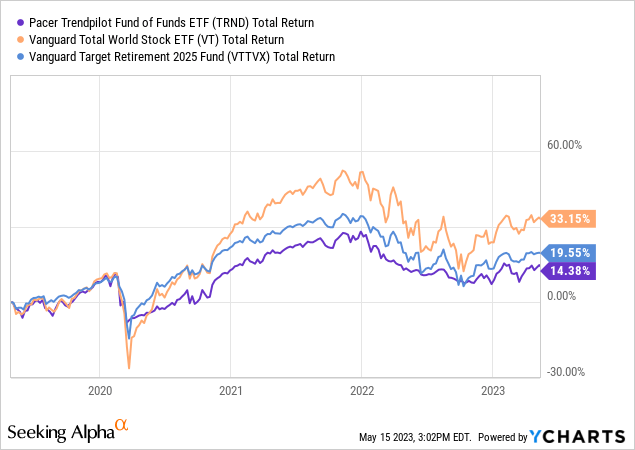

Although I’m unaware of an index or index ETF with identical weightings, some come close. The Vanguard Total World Stock Index Fund ETF (VT) is, roughly, 60% U.S. equities, 40% international equities. VT does lack TRND’s bond exposure, but this only account for 20% of the fund. The Vanguard Target Retirement 2025 Fund (VTTVX) holds an assortment of global and international equities / bonds, with a larger 40% bond allocation. Not identical, but close enough.

TRND has underperformed relative to these two funds since inception, and for most time periods.

Very sub-par results. Let’s have a look as to why.

TRND – Unsuccessful Investment Strategy

TRND’s underlying holdings attempt to time the market, by focusing on equities (or high-yield bonds) when markets are going up, but pivoting towards treasuries when these start to go down. TRND’s underlying holdings get the timing of this wrong more often than right, resulting in losses and underperformance.

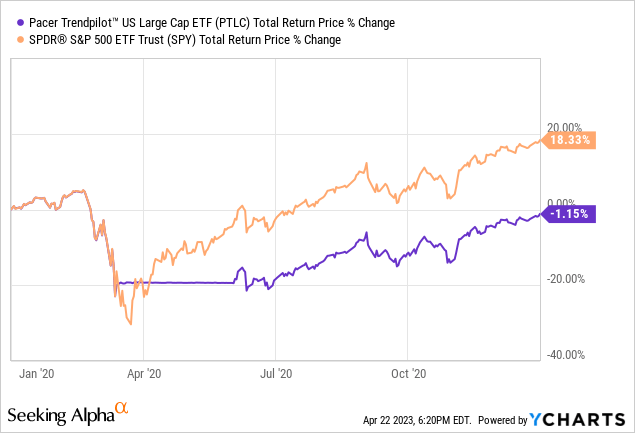

As an example, we have the Pacer Trendpilot US Large Cap ETF (PTLC) in 2020. PTLC was invested in equities early in the year, but swapped to treasuries in mid-March. The swap came too late to prevent most losses, although these were somewhat reduced. PTLC then remained invested in equities until mid-June, missing significant gains as equity markets recovered. PTLC experienced most of the losses but few of the gains of the S&P 500, leading to net losses and significant underperformance.

Data by YCharts

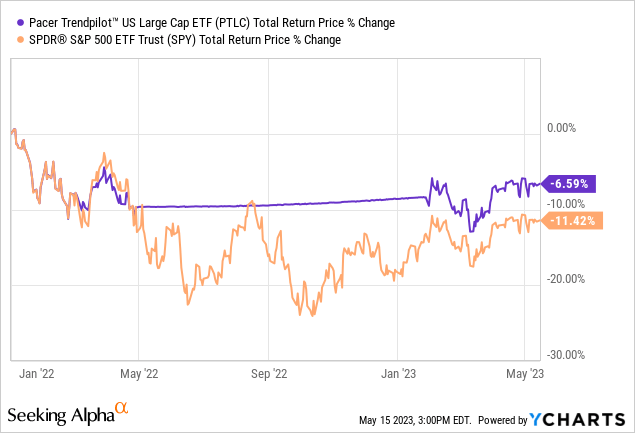

PTLC does sometimes get the timing right, as was the case in 2022. The fund started the year fully invested in equities, but pivoted towards treasuries in late April, avoiding around half the losses experienced by the S&P 500. The fund then swapped back to equities in early 2023, avoiding a moderate percentage of gains. The net effect was positive, with the fund moderately outperforming its benchmark.

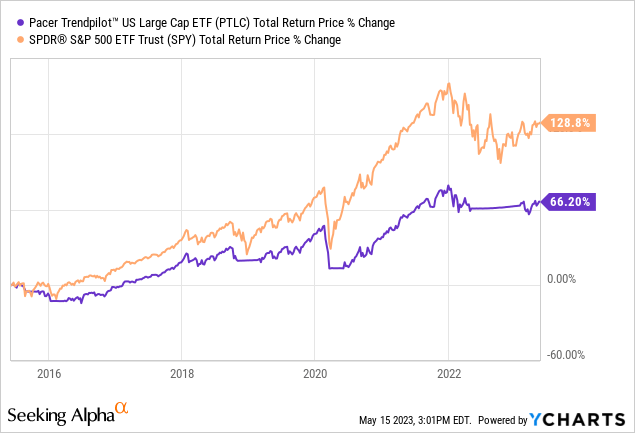

Although PTLC’s strategy sometimes works, it generally does not, leading to significant underperformance since inception.

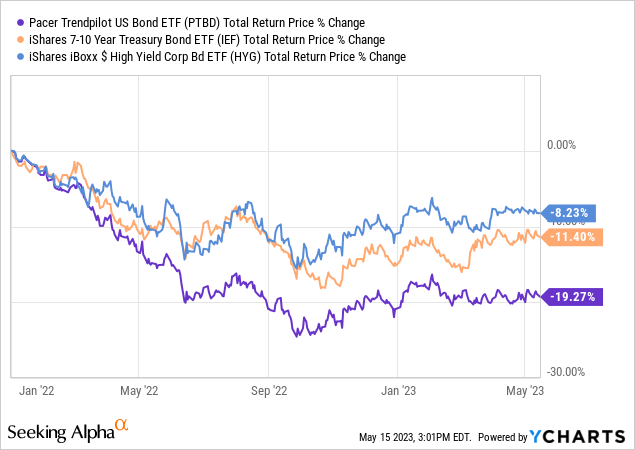

The same is true for TRND’s other holdings. PTBD, which invests in high-yield corporate bonds and / or treasuries, had terrible timing during this last hike cycle, consistently switching to the worst-performing asset class, month after month. Unlike PTLC, which generally avoided some losses and experienced some gains even when though the net impact was negative, PTBD’s strategy was almost overwhelmingly a failure, with few positives.

Although PTBD’s performance was, well, terrible, industry conditions were tough too, and these likely played a role too. Bonds were down across the board in 2022, and prices and rates were incredibly volatile. Few strategies worked, PTBD was not one of these.

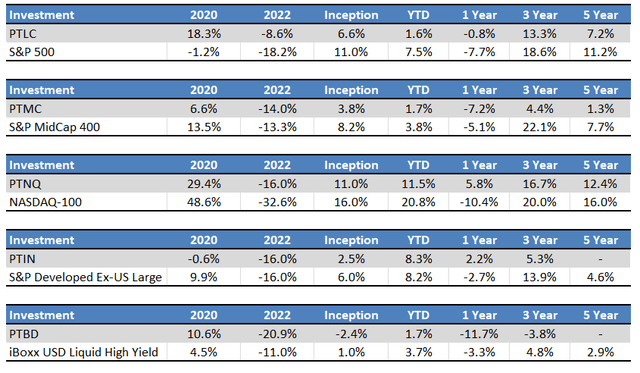

TRND’s underlying holdings all tend to underperform their respective benchmark, with some short-term exceptions. Performance is as follows, I’ve included data for the last two downturns, 2020 and 2022, which seems particularly relevant for these funds.

Seeking Alpha and Fund Filings – Chart by Author

TRND’s underlying holdings tend to underperform their benchmark, as does the fund itself. There are some periods of above-average results and outperformance, including 2022, but losses and underperformance are both more common scenarios.

TRND’s investment strategy has been ineffective in the past, hence the fund’s underperformance. TRND’s investment strategy will, I believe, continue to be ineffective in the future, for two reasons.

First, is the fact that the fund’s strategy is a form of market timing, which is incredibly hard, and rarely works. If investors could easily, mechanically predict stock market movements following a simple process everyone would do it until the process ceased to work. Timing the market is not impossible, but it is difficult to do, and, in my experience, most simple strategies don’t work.

Second, is the fact that Pacer’s strategies are so overwhelmingly ineffective. Each of TRND’s underlying holdings has underperformed since inception. There are periods of time in which they outperform, but these are somewhat uncommon, and somewhat arbitrary. Seems pretty clear that the strategy simply does not work, to me at least.

Conclusion

TRND’s ineffective investment strategy and underperformance since inception make the fund a sell.

Read the full article here