Twilio Inc. (NYSE:TWLO) is a fairly priced stock. Even though paying 12x next year’s non-GAAP operating profits seems like a bargain stock, particularly when you consider that nearly 15% of its market cap is made up of cash, Twilio’s growth prospects have fizzled out.

A combination of a tough macro backdrop, while the majority of Twilio’s revenues are usage-based (page 12), together with a hyper-competitive environment, has meant that Twilio’s growth rates are now scampering around the double-digit figures, and not much more.

In sum, I don’t see Twilio as a compelling investment opportunity.

Rapid Recap

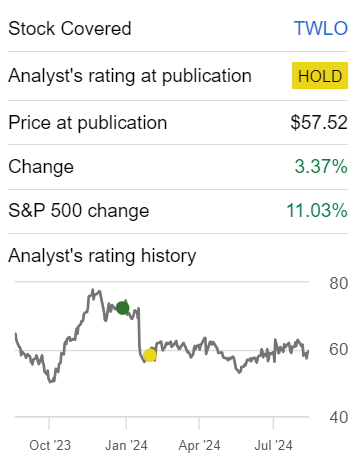

Back in February, I concluded my neutral analysis by saying,

Despite its improving profitability, the stock’s valuation at 16x forward non-GAAP operating profits raises concerns about its appeal to both growth and value investors. In this delicate balance, Twilio appears to be in a challenging position, requiring a careful reassessment of its trajectory. As an investor, the odds seem less favorable at the moment, leaving me on the sidelines on Twilio.

Author’s work on TWLO

In hindsight, it turns out that I made the right call moving to the sidelines on TWLO, as the stock would go on to underperform the S&P 500 (SP500) by mid-single digits over the coming 6 months. Today, as I look forward to next year, I remain firmly on the sidelines as I question its upside potential.

Twilio’s Near-Term Prospects

Twilio provides cloud-based communication services that enable businesses to connect with their customers via messaging, voice, email, and video, through APIs (Application Programming Interfaces).

Its key value proposition is simplifying how businesses integrate communication tools into their apps without needing to build the infrastructure from scratch. Twilio’s platform helps businesses offer personalized, real-time customer interactions while lowering operational expenses and increasing businesses’ customer engagement.

In the near term, Twilio’s prospects seem stable as it focuses on driving profitability and operational discipline. However, its growth has been slowing, with revenue increases in the single digits compared to its previous higher growth rates.

This deceleration reflects a maturing market, alongside macroeconomic uncertainties affecting its usage-based revenue model. To this end, as I’ve discussed on numerous occasions, I have yet to find many pure-play consumption business models that are a success.

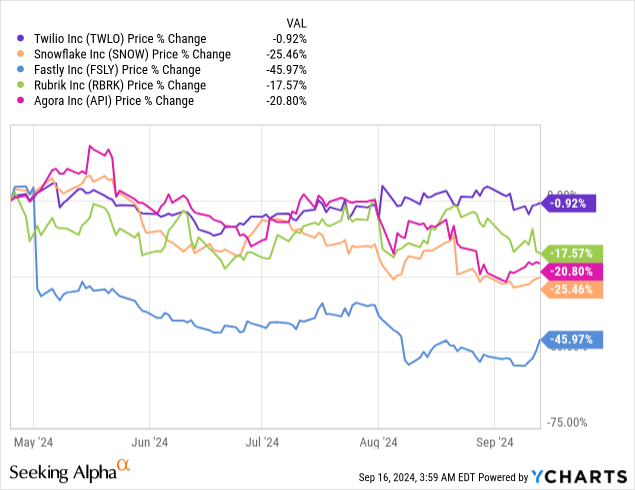

Data by YCharts

This is not an exclusive list of similar comparable consumption-based business models, but rather a handful of peers, all showing how their prospects have moderated of late.

What’s more, Twilio operates in a highly competitive space, where many companies with enough means are now considering using AI to build their own Software as a Service, or SaaS, platforms in-house.

Given this background, let’s now discuss its fundamentals.

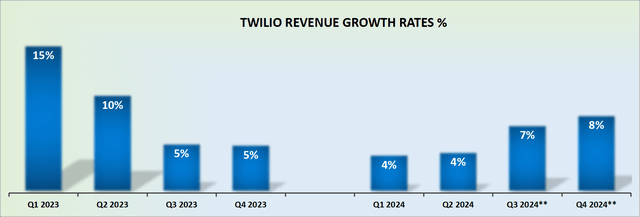

Twilio’s Revenue Growth Rates Leave Much to be Desired

TWLO revenue growth rates

Twilio is no longer a growth business. It’s now a business with a “high-tech narrative” but none of the fundamentals to support that narrative.

Investing is a game of probabilities. And it’s important to understand that there’s no such thing as a risk-free return.

It’s all about looking at the company, striving to make assumptions about its future prospects, and pricing in those prospects relative to what the market is expecting.

Furthermore, when the investors appraise Twilio and consider its potential outcomes for 3 years down the road, I suspect few investors would seriously consider Twilio as returning to mid-teens growth rates.

Indeed, I suspect that the most likely scenario for Twilio is that its growth rates stabilize around the mid-to-high single-digit growth rates, but not much more.

With this framework in mind, let’s now discuss its valuation.

TWLO Stock Valuation — 12x Forward non-GAAP Operating Income

The most positive aspect of Twilio’s investment thesis is that it carries about $1.3 net cash. This is clearly a positive consideration since this amounts to nearly 15% of its market cap being made up of cash. As an Inflection investor, this is something I contend is noteworthy and supportive of the bullish argument.

That being said, let’s make an estimate of Twilio’s 2025 non-GAAP operating income.

If we take the high end of Twilio’s guided $675 million of non-GAAP operating income, and assume that in 2025, Twilio’s non-GAAP operating income improves to approximately $780 million or a 15% y/y increase relative to this year’s non-GAAP operating income, this leaves Twilio priced at 12x next year’s non-GAAP operating income.

On the one hand, I don’t believe many investors would call this an exuberant valuation. And yet, a tech business is either disrupting and taking market share or is slowly fading away.

To retain top talent, executives typically meander towards winning companies, where their stock-based compensation is going to accrete in value over time. And I’m not convinced that top executives are going to flock towards a business that is delivering around double-digit growth rates.

Altogether, I’m very much on the fence with Twilio.

The Bottom Line

Paying 12x next year’s non-GAAP operating income for Twilio seems like a reasonable valuation given the current market environment.

However, the company’s growth prospects have cooled off significantly, with revenue growth slowing to the single digits and increasing competition. While Twilio’s cash position is strong, making up a substantial portion of its market cap, the macroeconomic challenges and competitive landscape make it less attractive for high-growth returns.

At this price point, I believe Twilio Inc. stock is fairly valued, and there are likely better opportunities elsewhere with more promising growth trajectories.