Business Model Overview

U.S. Physical Therapy (NYSE: NYSE:USPH) operates in two business segments: physical therapy operations and industrial injury prevention (IIP) services. Within the physical therapy segment, USPH has established itself as a significant player in the industry, with 662 clinics spread across 41 states, with a particular presence in Texas and Tennessee with 86 clinics and 83 clinics, respectively.

The physical therapy segment represented most of USPH’s 2022 revenue and gross profit at 87% and 86%, respectively. With approximately 150 active partnerships, USPH continuously expands its operations and enhances profitability by growing patient volume, adding new products and services, and making strategic acquisitions. Recently, USPH announced the acquisition of two physical therapy practices in Alaska and Colorado.

Acquisitions remain a key growth driver for USPH as they have completed more than 50 acquisitions in total since 2005. These acquisitions are structured as partnerships with clinics where the owner continues to operate in exchange for limited partnership interests ranging from 3 to 5 years. USPH believes that the clinic owners should maintain equity interest as it keeps them engaged and shares the same vision. This partnership allows USPH to leverage its scale to reduce the administrative costs on the clinicians, allowing them to focus on patient care.

Diversification has been another key strategy for USPH, evidenced by its expansion into the IIP sector in 2017 following the acquisition of Briotix. Since then, USPH has completed four additional acquisitions in the IPP segment, with the most recent acquisition of Progressive in 2021.

USPH’s IIP services, offered mainly to industrial sector clients, encompass a spectrum that includes onsite injury prevention, rehabilitation, performance optimization, and ergonomic assessments. The IIP segment has demonstrated notable growth and slightly higher margins than the physical therapy business, providing an avenue for the company’s future expansion and revenue diversification.

Industry Tailwinds

USPH forecasts the U.S. rehab market is $30 billion today and will exceed $40 billion by 2025. The market opportunity within this space is large and highly fragmented, with no company having more than 10% of the market share. Additionally, the physical therapy industry has favorable demographic tailwinds, such as an aging and obese population and a focus on cost-effectiveness within the healthcare industry.

August 2023 Investor Presentation

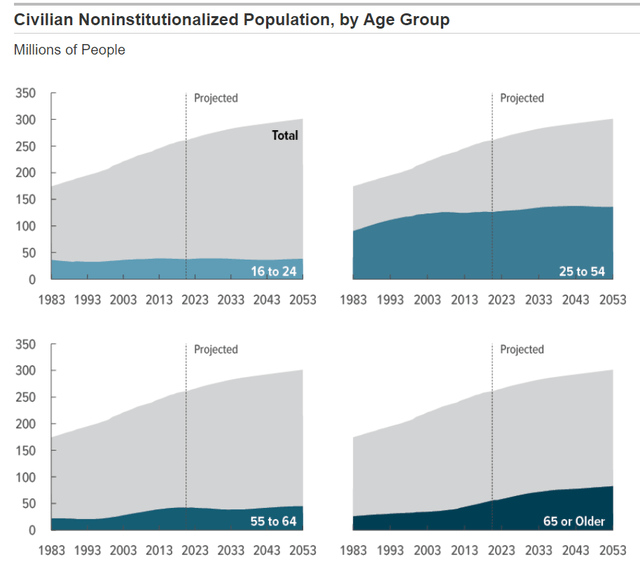

The physical therapy segment will continue to see increased demand, which is strongly correlated with demographic shifts. Notably, the aging population, projected to average 73 million people aged 65 or older from 2023 to 2053, is about double the average from 1983 to 2022, which indicates a larger patient pool with a higher likelihood of requiring rehabilitative services like lower back pain, knee disorders, and other orthopedic issues.

Congressional Budget Office

Obesity is another catalyst for physical therapy demand, as there is a discernible correlation between obesity and the probability of undergoing joint replacement surgeries, especially for the knee. Physical therapy services can help obese individuals in preventive and rehabilitative ways to help them live healthier. Obesity has been on the rise in the U.S. and is predicted to reach 58% by 2035, and this demographic trend signals a potentially escalated demand for physical therapy services.

There has been a focus on cost-effectiveness and high-quality outpatient providers within the healthcare industry. Patients and clinics increasingly prefer care that is accessible and cost-effective. Physical therapy, particularly in localized clinics, solves this problem by concurrently enhancing patient outcomes at lower costs than alternative treatments.

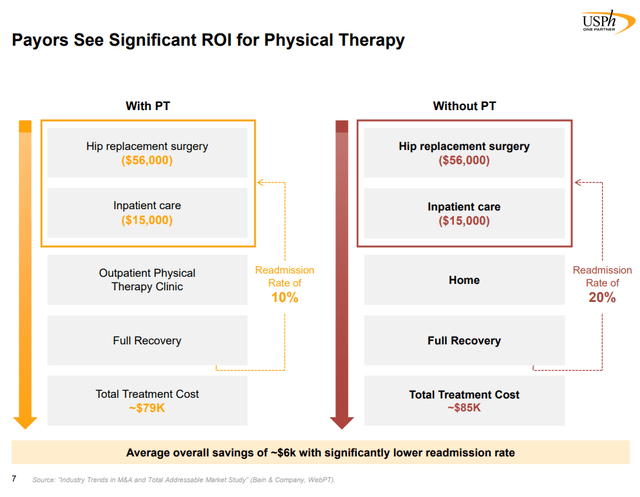

USPH conducted an internal study demonstrating that physical therapy can result in faster hospitalization release, avoiding surgical procedures, preventing chronic conditions, and eliminating the need for pain medication. The study highlights the benefits of patients who went to physical therapy after surgery compared to those who did not. The results showed that patients with physical therapy reduced their readmission rate by half and saved an average of $6k in total treatment costs.

August 2023 Investor Presentation

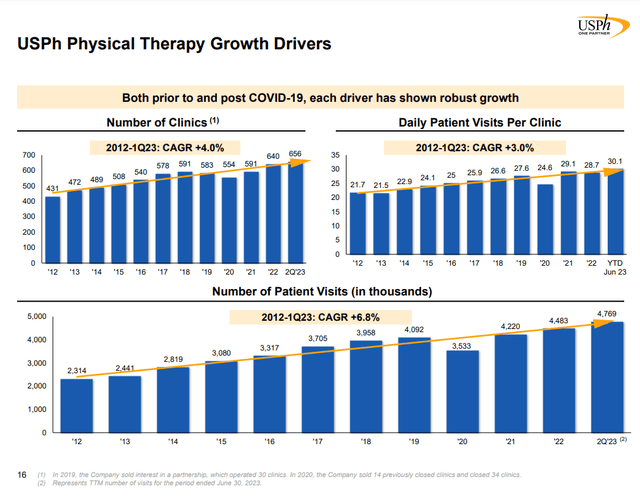

The graphic below shows how these tailwinds have been growth drivers for USPH’s key operational metrics. Since 2012, USPH has seen steady growth in the number of clinics, daily patient visits, and total patient visits, albeit they were negatively impacted in 2020 due to the pandemic lockdowns. The compounded growth rates over a decade suggest a robust business model and the potential for continued growth in the coming years, given the current health and demographic trends.

August 2023 Investor Presentation

Risks

Investing in USPH comes with potential risks that investors should be aware of.

Firstly, the looming pressure on Medicare reimbursements poses a significant challenge. The Centers for Medicare & Medicaid Services has proposed a decline in reimbursement for outpatient rehabilitation services by 3.5% for the upcoming year. This trend is projected to persist through 2025, with continued implementation of multi-year cuts proposed back in 2020. Considering Medicare’s history of program revisions, there’s a real concern that future reimbursement rates may not adequately compensate USPH for its services. In some scenarios, these rates might not even cover operating costs. This is particularly concerning, given that Medicare represents one of USPH’s primary payment sources.

Another concern is the risk of recession. Economic downturns can unfavorably impact both of USPH’s operating segments. In the physical therapy segment, a recession might lead to a drop in patient volumes. As individuals face the loss of employer-sponsored health coverage or diminishing discretionary income, they might postpone or forgo care altogether. While enacting the Affordable Care Act might buffer USPH against extreme impacts like those experienced during the 2007-09 recession, the company could still face challenges. The primary repercussions might be a shift towards payors with lower reimbursement rates, such as Medicaid, negatively affecting revenues and margins. As for the IIP segment, a recession could decelerate or reverse top-line growth. Employers grappling with financial constraints might delay expansions or cut back on employee services.

Final Thoughts

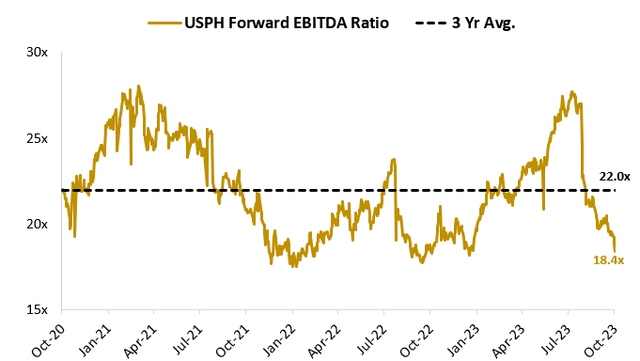

The stock is trading around $85 with an enterprise value of $1.5 billion. Analyst consensus estimates NTM EBITDA to be $84 million, translating to a forward EBITDA ratio of 18.4x. While the company trades at a premium relative to its peer average of 10.7x, USPH’s forward EBITA ratio is compressed and below its long-term average of 21.9x.

Capital IQ

This gap creates a good entry point as the stock has been unnecessarily punished about the implications of GLP-1 adoption. The market is discounting the stock, healthcare industry, due to the rise of weight loss drugs like Ozempic, which is expected to lower obesity rates, thereby reducing the number of patients needing physical therapy. Simply put, I don’t buy it. In my opinion, the new weight loss fad will not materially impact the need for physical therapy services. These drugs are costly due to their high demand and will be limited to fewer users than the forecasts estimate. Additionally, production capacity is likely to constrain near-term adoption.

Obesity is only one of many growth drivers for the physical therapy industry, and the market is discounting the growing focus on cost and quality of services. USPH has created a scalable business model that allows them to limit costs and improve operational efficiencies due to their centralized structure. Furthermore, the stock trades at an attractive valuation, so I rate USPH a buy.

Read the full article here