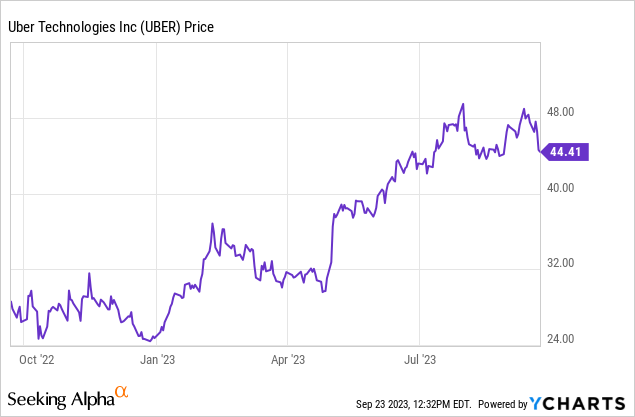

Volatility has returned, and Uber (NYSE:UBER) has fallen roughly 10% from near-term peaks in sympathy with other tech stocks due to rising interest rate fears. From a business standpoint, however, Uber is still chugging along – quite literally. Bookings and profitability are soaring at all-time highs, and Uber continues to take market share from its main U.S. competitor, Lyft (LYFT). In other words: it’s a good time to be greedy while others are fearful.

Though shares of Uber remain up more than 70% on the year, I continue to see this stock as a very long-term play. I last wrote a bullish note on Uber when the stock was trading closer to $50, and am even more bullish now at current lower levels. In the time since, Uber has also released Q2 results, which came in well ahead of expectations and provide additional reasons to be sanguine on the stock’s opportunities.

Uber has grand designs on what its nebulous market opportunity really is. From the humble taxi app came a delivery powerhouse and an enterprise freight solution – the latter of which, by the way, is poised to take share as chief rival Flexport struggles from leadership turnover and lower enterprise spending. Uber Freight can continue to build out operations and sustain minor losses because the company’s other segments are already massively profitable.

News also recently broke that Uber is looking to expand into a task-fulfillment service in the vein of TaskRabbit. Uber is effectively evolving from becoming simply a mobility company and instead pivoting toward becoming the all-in-one app for convenience: getting to places, getting delivery from places, and getting chores done. The pandemic has exposed the fact that we are willing to pay a pretty penny for convenience, and those habits have been deeply ingrained since.

Here’s a refresher on my updated bull case for Uber:

- Huge $13.8 trillion TAM and “other bets” to support continued expansion. Mobility and Delivery each carry $5 trillion market opportunities, and nascent Uber Freight is another massive $3.8 trillion market that is heavily underserved and ripe for tech disruption. Grocery, package delivery, and the potential release of task fulfillment are other nascent ways in which Uber is expanding its dominance.

- Formidable market leadership. In most of the markets that Uber operates in, the company has a leading market share, and usually by a substantial margin. The company has selectively exited markets where it lost share to a local incumbent (Grab in Singapore is a good example), so it can focus on turf where it has the advantage. And in Freight, Uber’s profitable lines of business can support weaker enterprise freight demand while specialist rival Flexport declines.

- The sharing economy is gradually taking precedence over ownership. Even pre-pandemic price inflation caused many to rethink buying cars, many consumers were already questioning the wisdom of car ownership over rideshare. Owning a car comes with maintenance costs, insurance costs, and in urban areas, often hefty parking costs. Gradually, I expect car ownership to decline and for rideshare to become the preeminent form of transportation.

- Uber One. Uber introduced a $10/month subscription membership that offers, among other benefits, free deliveries on Uber Eats and 6% cash back on rideshare. In my view, this move will help to boost rider loyalty and frequency on top of generating a new subscription revenue stream.

- Massive adjusted EBITDA and above GAAP profitability threshold. Driven by the uptick in rideshare volumes plus higher take rates in both the rideshare and delivery businesses, Uber is driving tremendous Adjusted EBITDA growth. In addition, the company recently crossed into profitability from a GAAP perspective, something very few tech companies achieve.

It’s not entirely unreasonable, in my view, to think of Uber as a slightly earlier version of Alphabet (GOOG) – a consumer internet giant that is spreading its venerable brand into a deep array of interlinked services. Don’t pass up the opportunity to buy Uber while it’s trading lower.

Q2 download

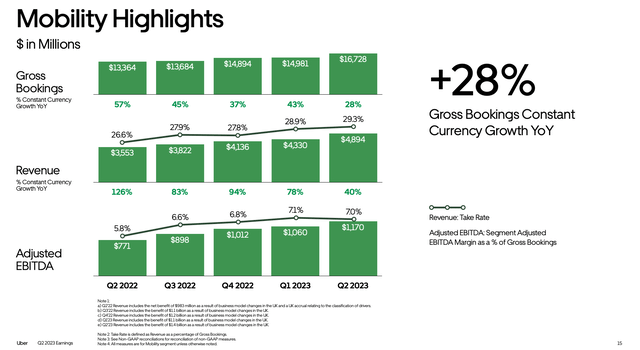

Let’s now cover some of the key highlights of Uber’s most recent quarter in greater detail, starting with the Mobility segment:

Uber Mobility (Uber Q2 earnings deck)

Uber’s mobility segment saw 28% y/y growth in gross bookings to an astonishing $16.7 billion. And driven by higher take rates (higher fees), Uber achieved 38% y/y growth in revenue to $4.89 billion, or 40% y/y on a constant currency basis. It’s worth noting that in the same quarter, despite being at roughly a quarter of Uber’s revenue scale, Lyft only grew revenue at a 3% y/y clip, showcasing how aggressively Uber is taking market share from its primary U.S. competitor.

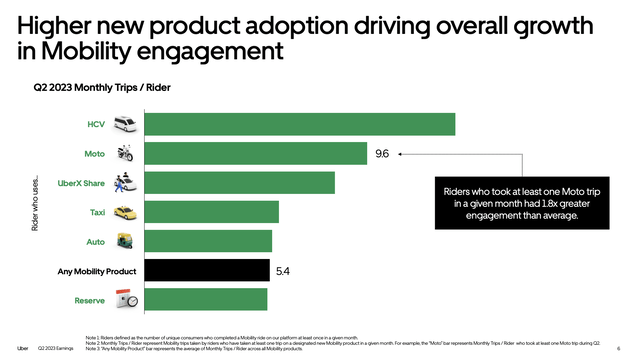

The company has not only rolled out a variety of ride options within Mobility, but rider engagement continues to be incredibly high – as shown in the table below, the average rider takes 5.4 riders per month:

Uber Mobility engagement (Uber Q2 earnings deck)

Speaking on engagement trends during the Q&A portion of the Q2 earnings call, and noting that engagement in some international markets is even higher than the company average (helping scalability for Uber’s overseas operations), CEO Dara Khosrowshahi noted as follows:

And our frequency has consistently increased in terms of transactions per MAPC, 9% year-on-year.

And if you think about audience and frequency, we think that we should be able to grow audience at strong either high-single digits, low-double digits, as we introduce a host of new products out there and as we continue to expand internationally as well, and frequency continues to increase and it’s not quite at all-time highs even at this point in terms of 5.6 uses per month.

And if you look at certain markets like Brazil in Mobility alone, the frequency is over 7 times a month. So, we think we’ve got many, many years of increasing frequency. Again, as we add more products into the service and generally the world goes more on demand.

And then, on top of that, you add inflation or pricing growth, call it, normalized pricing growth as well, we think it — we have a base business that can grow in the double digits. Again, audience, even if you say single-digits, frequency, single-digits plus, price in the single digits, you get to a double-digit growth rate for the base business.”

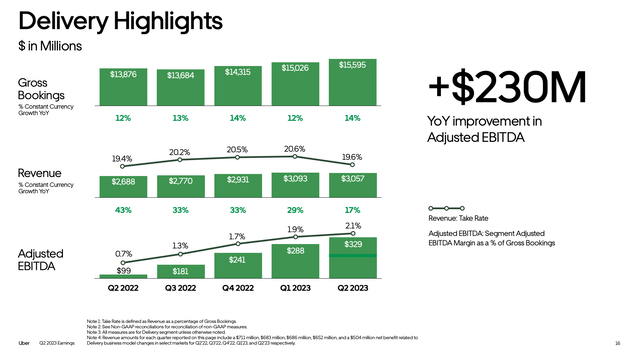

Delivery also continued to grow at a startling pace, with revenue growing 17% y/y on a constant currency basis to $3.06 billion. Note as well here the significant scaling in profitability in this segment: what used to be a loss leader for Uber is now generating a 2.1% adjusted EBITDA margin on bookings (+140bps y/y), and a 10.8% margin on revenue:

Uber Delivery (Uber Q2 earnings deck)

Here, it’s not just sustained post-pandemic takeout trends that are driving growth. Category expansion into areas like grocery is helping Uber expand its delivery muscle, not to mention the potential market opportunity from expanding into task-based services. Overall, Grocery products and other non-restaurant offerings (what Uber refers to as “New Verticals” like retail) have notched a $6 billion annualized gross bookings run rate (which would be roughly 10% of Delivery’s Q2 bookings profile). The company notes that 13% of Delivery users have also used a New Vertical offering.

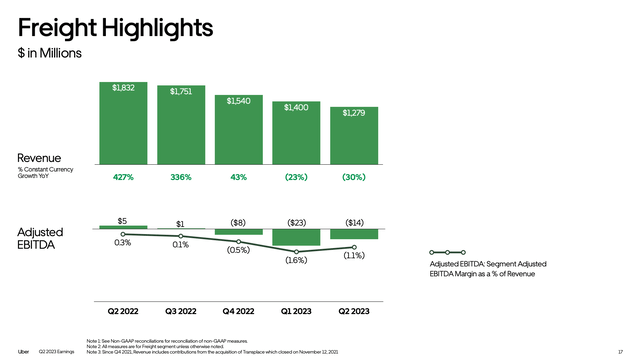

Freight, meanwhile, is the main laggard for Uber – though in terms of company contribution to revenue, Freight is still less than 15% of total revenue. Freight has declined -30% y/y, driven by lower enterprise activity and sharply lower shipping rates since the pandemic-era shipping bottlenecks have faded. Still, we note that Freight is still at a roughly break-even adjusted EBITDA profile, despite sharp revenue contraction (which will be quick to rebound once the macro picture improves).

Uber Freight (Uber Q2 earnings deck)

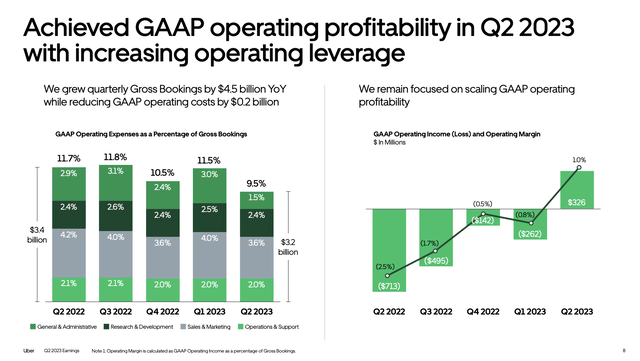

Overall, we note as well that Uber notched a 1.0% GAAP net margin, 350bps better than the year-ago quarter.

Uber profitability (Uber Q2 earnings deck)

The company’s adjusted EBITDA also grew by 2.5x y/y to $916 million, representing a 10% margin. And note that Uber has sliced roughly $200 million out of its quarterly opex base in the left-hand side chart above, primarily by reducing sales and marketing and G&A expenses – which has enabled substantial profitability growth.

Key takeaways

Overall, I see a number of catalysts for Uber to regain lost ground and continue its rally. Uber has designs on becoming an “everything app” – and I continue to view it as an early investment in a future tech mega-cap.

Read the full article here