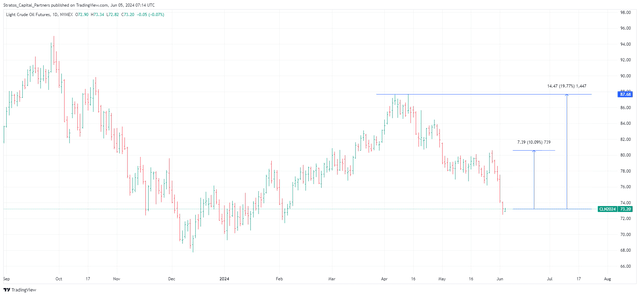

Concerns building up to The Organization of the Petroleum Exporting Countries Plus’s (OPEC+) decision to unwind production cuts have driven prices for WTI crude oil futures down to near a 4-month low. OPEC+ members reached an agreement on June 2 to extend existing output cuts into 2025. The group will, however, allow voluntary cuts for some of its members to be unwound gradually beginning in October.

WTI crude oil prices per barrel (US$/bbl) fell by more than $3 to trade as low as $72.50/bbl after the news. Traders fear that the unwinding of output cuts by some OPEC+ members will put downward pressure on crude oil prices, especially given that demand is already starting to show some signs of weakness.

TradingView.com

Following the sharp sell-off over the past two trading sessions, we now see an imminent technical rebound in WTI crude that should present an attractive trading opportunity.

The ProShares Ultra Bloomberg Crude Oil ETF

The ProShares Ultra Bloomberg Crude Oil ETF (NYSEARCA:UCO) continues to be our favourite tool for fully capitalizing on our high-conviction views on WTI crude.

According to fund information provided by ProShares, UCO is leveraged to seek a return that is 2x the daily performance of the Bloomberg Commodity Balanced WTI Crude Oil Index (target index), as measured from one NAV calculation to the next. The target index tracks the performance of three separate contract schedules for WTI Crude Oil futures with different roll dates. To maintain the long position of the futures basket, contracts are rolled from the expiring futures contract to a new contract further down the curve with a longer expiry date.

UCO is ideal whenever we wish to position for a tactical rebound in crude oil prices with a relatively short trading window of just 1-3 months. Taking advantage of UCO’s 2X leveraged exposure to WTI crude, we have previously demonstrated how we were able to amplify returns on our bullish view back in December 2022 and again in June 2023.

Once again, we see current levels on WTI crude as a compelling opportunity to re-establish our bullish view. We expect prices to rebound forcefully over the next 1-3 months.

Accordingly, we are upgrading our rating on UCO from “Hold” to a “Strong Buy”. We see the potential for a 10%-20% rebound in crude oil prices within this time frame, and we target a 2x amplified return through a leveraged exposure using UCO.

TradingView.com, Stratos Capital Partners

Our 10%-20% WTI crude target implies an initial 10% move back up to around $80.60/bbl (resistance last recorded on May 29), followed by a potential move back up to around $87.70 (resistance last recorded on April 12).

Fundamentals For Crude Remain Robust

Our reassessment of the crude oil market suggests that the pessimistic sentiment is largely unjustified. From a medium-term perspective, we believe that the overall fundamentals underlying WTI crude remain supportive of higher prices.

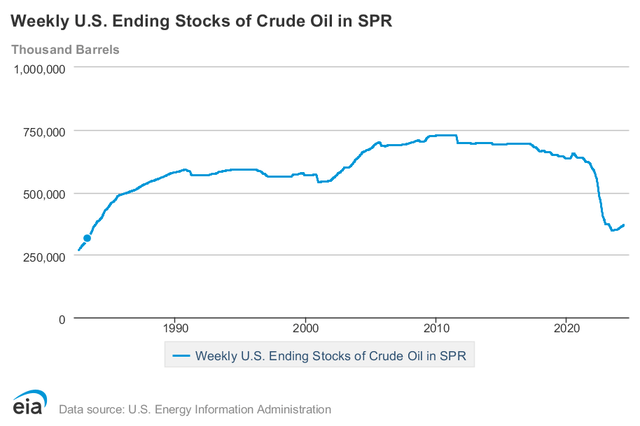

Firstly, the U.S. Strategic Petroleum Reserve’s (SPR) crude oil stockpile continues to run at historic lows, according to the latest data published by the U.S. Energy Information Administration (EIA).

U.S. Energy Information Administration

The drawdown of the SPR, due to the Biden administration’s efforts in 2022 to mitigate global supply disruptions and help lower energy costs, will have to be replenished. We expect this to continue to support WTI crude prices at around the $70 to $80 levels.

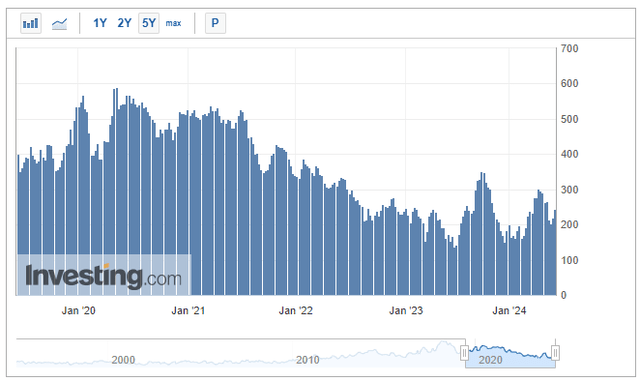

Secondly, we note that China’s demand for crude oil in 2023 has surpassed the expectations of many industry experts and economists (us included). According to data published by the EIA, China’s crude oil imports have recovered and exceeded pre-pandemic levels. This is despite evidence that China’s economy remains in a subdued and vulnerable state.

U.S. Energy Information Administration

To be clear, we continue to maintain a sceptical view of China’s macroeconomic recovery due to structural imbalances and political risk. Admittedly, we were surprised and humbled by the resilient demand for crude oil in China. Therefore, even though we continue to anticipate a sputtering economic recovery in China, we have toned down our expectations of the negative impact on crude oil demand and prices.

Finally, we see some U.S. dollar weakness ahead following the retreat in Treasury yields over the past few trading sessions. We continue to see scope for a rate cut by the Federal Reserve in September, which also adds to our thesis for moderate dollar weakness stretching into 2025. Moderate dollar weakness will be mildly positive for commodities, including crude oil, all else equal.

Sentiment Is Overwhelmingly Bearish Again

In terms of market positioning, data published by the Commodity Futures Trading Commission (CFTC) show net speculative positions on crude oil running near 5-year lows. We view this overwhelmingly bearish sentiment on crude oil as a favourable condition for our bullish contrarian view. In a good case scenario, a forceful rebound in crude oil prices may potentially trigger a rush to unwind speculative short positions, providing further fuel for the rally.

Commodity Futures Trading Commission (CFTC))

In Conclusion

We see current levels on WTI crude as a compelling opportunity to re-establish our bullish view. We expect prices to rebound forcefully over the next 1-3 months.

Accordingly, we are upgrading our rating on UCO from “Hold” to a “Strong Buy”. We see the potential for a 10%-20% rebound in crude oil prices within this time frame, and we target a 2x amplified return through a leveraged exposure using UCO.

Read the full article here