UGI: Investment Thesis

There are a number of factors I believe are likely to cause an improvement in UGI Corporation (NYSE:UGI) share price in the period ahead. These include –

- a likely SA Quant rating change from Hold to Buy

- improved profitability due to positive management actions

- a strengthening in the balance sheet, including improvement in the debt ratio

Fundamentals are important, but market sentiment has a significant impact on a stock’s share price performance. UGI has historically enjoyed P/E multiples in the double digits until relatively recently. UGI has a dividend yield over 6%. The dividend is well covered by earnings. It has been paid continuously for the last 140 years, with a commitment to continue paying. The company has failed to meet optimistic EPS projections made by management in 2021. I believe this is a major factor contributing to the current depressed share price. The present multiple is 7.36, based on non-GAAP EPS TTM at March 31, 2024. I believe the market has overshot to the downside with UGI stock price, and I rate the shares a Buy. Additional detail for the various factors discussed above appear below.

UGI: Market sentiment

We can analyse the fundamentals, but share price of a stock is also heavily influenced by market sentiment toward that stock. In my February 1, 2024 article, “UGI Corporation: Dashed Expectations Create Buy Opportunity”, I came to the conclusion the depressed share price was due to EPS growth not matching expectations created by management back in 2021. Since then, market sentiment towards the stock has been in decline. The effect of this on UGI’s stock price has been severe. Between 2021 and 2024, the P/E ratio for UGI has averaged around 11.5, with the median around 12.0. That is a far cry from earlier years when the stock regularly traded at P/E ratios over 20.0. But 11.5 is the average multiple for the period 2021 to 2024, and the trend has been downward throughout this period. UGI’s forward P/E ratio is currently 7.99, and it has been lower than that.

UGI: Assessing the direction of market sentiment –

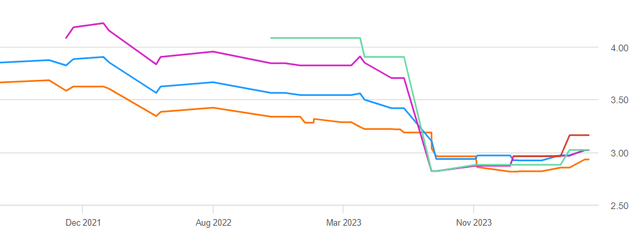

I like to look at SA Quant ratings for fundamental quantitative analysis combined with an assessment of elements of that analysis ascertained as potential influences on market sentiment. Figure 1 below shows SA Quant assessment of market sentiment at Feb. 1, 2024, the date of my previous analysis, compared with the current SA Quant assessment at Jul. 12, 2024.

Figure 1

SA Premium

As can be seen, “Revisions” are one of five Factor Grades considered influential on investor sentiment, and thus share price. Back in June 2021, UGI management provided some bullish guidance for 2021 and 2022, which caused SA and other analysts to significantly lift forward EPS estimates for the next few years. That guidance has not been met. This has resulted in subsequent downward revisions by analysts, as shown in Figure 2 below.

Figure 2

SA Premium |

|

Source: Seeking Alpha Premium Quant Earnings Revisions – UGI Corporation |

By October 2023, hopes for the high EPS growth rates expected back in mid-2021 had been completely dashed. In addition, interest rate increases had impacted the share prices of utility stocks across the board.

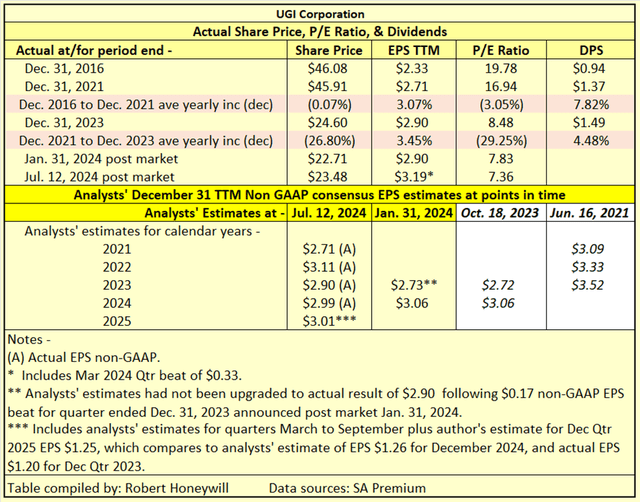

The impact on share price is shown in Table 1 below.

Table 1

SA Premium

Table 1 shows UGI grew non-GAAP EPS by an average 3.07% per year between 2016 and 2021, while share price remained virtually unchanged over this period. Between end of 2021 and end of 2023, despite non-GAAP EPS increasing by 3.45%, share price fell by 26.80%, from $45.91 to $24.60.

Looking back to Figure 2, we can see a start of some upward revisions to analysts’ EPS estimates. This has already had an impact on SA Quant ratings with “Revisions” upgraded from a “D” at Feb. 1, 2024, to an “A+” at Jul. 12, 2024. Improved profit due to strong EPS beats against estimates for both December 2023 and March 2024 quarters has seen SA Quant “Profitability” rating increase from a “C-” at Feb. 2024 to the current “B” rating. Figure 2 shows the overall SA Quant rating has improved from 2.68 at Feb. 1 to the current 3.32. This is not far below a 3.50 rating, which would see Quant rating flip from the present “Hold” to “Buy”. One drag on the Quant rating has been “Momentum” which has gone from a “C-” at Feb. to the current “D-” as the share price of $22.71 at Feb. 1 continued to fluctuate and reached a low of $22.01 on July 9. The share price has ticked upward since then, and we could be reaching a tipping point where we see some sustained upward momentum in the share price.

UGI: Profit Performance FY2016 to FY2023

UGI is a utility with both regulated and unregulated operations. Average yearly EPS growth over the last 7 years has been modest, in the low single digits, but nevertheless positive. The regulated operations have shown steady earnings growth, averaging 9.5% per year over the last 7 years. Excerpted from the Company’s March Quarter earnings call,

…we are targeting a 4% to 6% EPS growth rate… Fiscal 2025 and 2026 will be rebuilding years …anticipate investing capital of approximately $3.9 billion across UGI during that period. A primary driver of the targeted EPS growth is our planned investment of approximately $2.6 billion at the regulated utilities, which will facilitate 9%-plus rate base growth…

The prospect of 9%+ returns has to be tempered with the fact regulated operations contribute only around one-third of earnings, hence the lower overall targeted growth rate.

Of the non-regulated operations, Midstream & Marketing has performed well, but the nature of the business leads to considerable volatility in year-to-year earnings. AmeriGas Propane and UGI International showed good earnings growth through FY 2021, but have struggled since, with significant earnings decline for AmeriGas Propane in particular. A plan is in place to stabilize and optimize AmeriGas Propane operations.

UGI: Dividend considerations

The current quarterly dividend of $0.375 per quarter ($1.50 per year) provides a healthy dividend yield of 6.40% per year at current $23.42 share price. Per Table 1 above, dividend growth has exceeded share price growth by a wide margin over the last 7 years. Excerpted from the company’s March quarter earnings call transcript in relation to earnings and dividends,

With a robust performance in the first half of the fiscal year, we are on track to deliver within our fiscal 2024 adjusted EPS guidance range of $2.70 to $3. We are also pleased to mark the 140th year of consecutively paying dividends, demonstrating our commitment to returning value to shareholders…. Between fiscal 2024 and 2026 as we focus on strengthening the balance sheet and stabilizing AmeriGas, we expect that dividends will stay flat, while still achieving a payout ratio close to 50%. Now as we move to fiscal 2027, we anticipate returning to our targeted 4% dividend growth rate over the long term.

Despite the proposed suspension of dividend growth over the next three years, the dividend yield is likely to remain very attractive, and the dividend payment appears very safe.

UGI: Balance Sheet

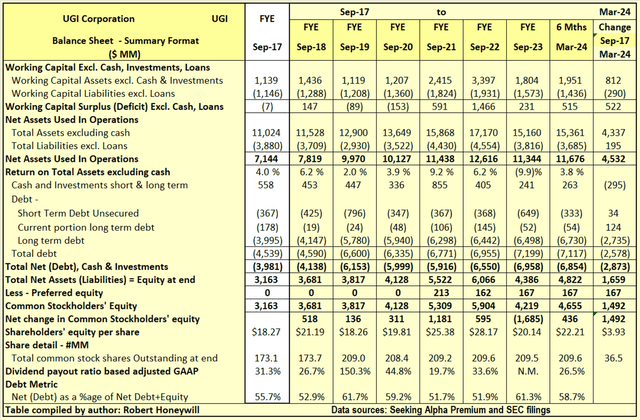

Table 2.1 UGI Balance Sheet – Summary Format

SA Premium & SEC filings

Over the 6.5 years end of September 2017 to the end of Mar. quarter 2024, UGI’s shareholders’ equity increased by $1,659 million. This $1,659 million increase, plus an increase of $2,873 million in debt net of cash was used to fund an increase of $4,532 million in Net Assets Used In Operations. Net debt as a percentage of net debt plus equity increased from 55.7% at the end of September 2017 to 58.7% at the end of Mar. quarter 2024. Outstanding shares increased by 36.5 million from 173.1 million to 209.6 million, over the period. Shares issued for employee compensation exceeded share repurchases. However, the great majority of the increase in shares came from share issues for the CMG acquisition in 2019 (see p. F-28 of FY-2019 10-K for details of acquisition). The $1,659 million increase in shareholders’ equity was comprised of $167 million from a preferred share issue and an increase of $1,492 million increase in common stock shareholders’ equity. The $1,492 million increase in common stock shareholders’ equity over the last 6.5 years is analyzed in Table 2.2 below.

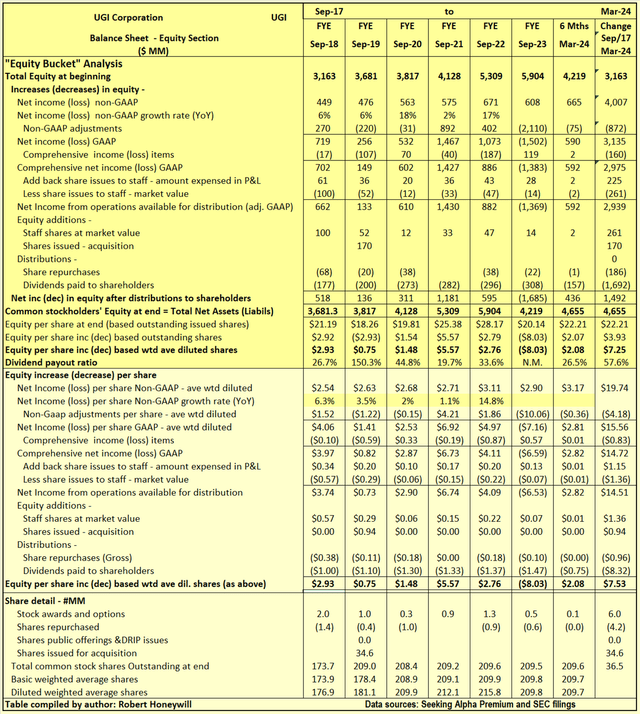

Table 2.2 UGI Balance Sheet – Equity Section

SA Premium & SEC filings

I often find companies report earnings that should flow into and increase shareholders’ equity. But often the increase in shareholders’ equity does not materialize. Also, there can be distributions out of equity that do not benefit shareholders. Hence, the term “leaky equity bucket.” I look for evidence of this in my analysis of changes in shareholders’ equity.

Explanatory comments on Table 2.2 for the period end FY-2017 to end Mar-2024.

- Reported net income (non-GAAP) over the 6.5-year period totals $4,007 million, equivalent to diluted net income per share of $19.74.

- Over the 6.5-year period, the non-GAAP net income excludes $872 million ($4.18 EPS effect) of items regarded as unusual or of a non-recurring nature in order to better show the underlying profitability of UGI. These items are primarily impairment charges for goodwill, amortization of intangibles, and restructuring charges.

- Other comprehensive income includes such things as foreign exchange translation adjustments with respect to buildings, plant, and other facilities located overseas and changes in the valuation of assets in the pension fund – these are not passed through net income as they fluctuate without affecting operations and can easily reverse in a following period. Nevertheless, they do impact the value of shareholders’ equity at any point in time. For UGI, these items were negative, decreasing equity by $160 million over the 6.5-year period.

- There were share issues to employees, and these were a significant expense item. The amounts recorded in the income statement and in shareholders’ equity, for equity awards to staff totaled $225 million ($1.15 EPS effect) over the 6.5-year period. However, the market value of these shares is estimated to be $261 million ($1.36 EPS effect). The understatement of expense by $36 million is not material in the context of non-GAAP earnings total of $4,007 million over the 6.5-year period, and not overly concerning from a “leaky equity bucket” aspect.

- By the time we take the above-mentioned items into account, we find, over the 6.5-year period, the reported non-GAAP EPS of $19.74 ($4,007 million) has decreased to $14.51 ($2,939 million), added to funds from operations available for distribution to shareholders.

- Dividends of $1,692 million and share repurchases of $186 million were adequately covered by the $2,939 million generated from operations, leaving a $1,061 million increase in equity. This $1,061 million from operations, together with the $261 million capital raised through share issues to staff, and the $170 million related to shares for the CMG acquisition, resulted in the $1,492 million net increase in shareholders’ funds per Table 2.1 above.

Summary and conclusion

Sentiment toward this stock is likely colored by failure of management to meet the high expectations set for EPS growth in mid-2021. Judging the company’s performance against its longer term historical performance, it’s believed the stock is significantly undervalued by the market. The possibility of interest rate cuts in 2024 would be a further positive. It also would not take much for SA Quant ratings to flip to the positive and to a Buy recommendation. At a P/E ratio of 12.0 the share price would increase from its present $23.42 to ~$35.00. A P/E ratio of 12.0 is below UGI sector median of 16.61 and also below UGI’s longer-term average multiple. I rate the stock a Buy.

Read the full article here