Investment Thesis

I wanted to take a look at UniFirst (NYSE:UNF) which is not very well known/covered widely in the investment world to see if the company, which sounds like a boring company would be a hidden gem in the investment world and may be a good long-term investment. Upon further review of the company, I can see that its margins have deteriorated slightly due to the negative inflationary period which affected costs and due to the company’s key initiatives. Therefore, I assign a hold rating as I do not see margins improving for a little while longer until the initiatives are fully implemented and price stability resumes.

Briefly on the Company

UniFirst is the largest provider of uniforms in many different workplaces around the US. The company designs, manufactures, personalizes, and rents many uniforms ranging from shirts, pants, coveralls, lab coats, and even protective gear like flame-resistant and highly reflective visibility garments.

The company will also regularly pick up their product for weekly cleaning, and then deliver back on time all cleaned and processed. The company derived almost 90% from the US and Canadian Rental and Cleaning operations, which make up the Core Laundry Operations segment.

The company’s business model is quite straightforward and that is one of the reasons I wanted to cover it, to see if there is something there from simplicity.

Outlook

Given the macroeconomic outlook that we have been experiencing recently resurged, the inflation is stickier than once believed earlier and the FED may raise interest rates further and keep them higher for longer. All because the economy is still doing exceptionally well, and that is not what Mr. Powell wants. The unemployment rate has not ticked up significantly since the interest rates skyrocketed, which is a good thing for a company like UNF, because most of their revenue depends on how many people are employed in the serving industries, of which there are many around the US and Canada.

So, how likely are we going to see a recession soon? Back in July, economists predicted that we would see a recession by July of ’24 and put the chance at around 59%. Fast forward a few months, that risk dropped to 49% and we will see a recession by September of ’24. It looks like we are further and further away from a recession, which could bring down unemployment rates significantly, therefore affecting companies like UNF dramatically. Or will it?

Looking at the past revenue performance of the company, especially during the pandemic times, I did not see a massive drop in revenues at all, which may indicate that the company seems to be quite well equipped for these sorts of headwinds. However, the COVID pandemic was just a temporary setback and many businesses resumed their operations, which meant that they required UNF’s services soon after.

If we see a proper recession where the unemployment rate climbs higher but stays at that level for longer, I could see the company’s revenues get hit, however, it seems like the coin is weighted on no recession for at least the foreseeable year or two, which should bode well for UNF.

Margins Suffering – Short-term Headwind

During Q4 ’21, the management announced that the company is going to embark on a multi-year project that will transform the company’s ERP systems “with a strong focus on supply chain and procurement automation in technology.” Besides this initiative, the company started investing heavily in the UniFirst brand which primarily was a big cost in FY22. These initiatives weighed massively on the company’s profitability as margins were squeezed considerably as you will see in the financial section later. On top of these initiatives, the company felt pressure from the inflation rising considerably in FY22, which increased product and labor costs dramatically (also covered in the financials section).

I believe that these are all short-term headwinds and after the initiatives are fully incorporated and the inflation comes down and stabilizes, I can see the company’s margins improve once again.

Financials

As of Q3 ’23, the company had around $69m in cash and short-term investments against zero debt. This is always a great position to be in, as it allows for flexibility in how the management wants to utilize the company’s cashflows and not to worry about annual interest expenses on debt that lowers the company’s available capital. The company can focus on retaining its profitability, rewarding its shareholders via dividends, share buybacks (if shares are cheap enough), or use it for some growth initiatives, although, it is hard to see how a company that’s been around for almost a century will come up with some growth strategies.

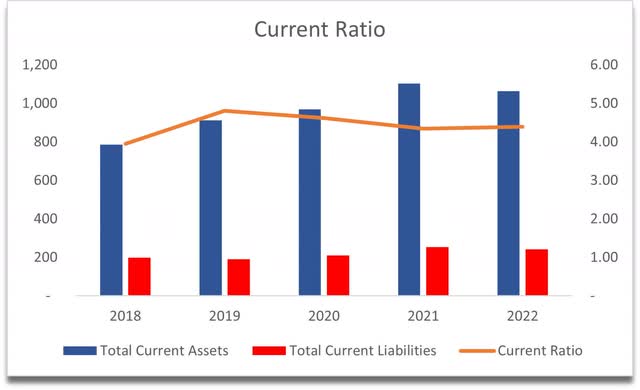

The company’s current ratio has been very strong over the years, and as I suspected a bit too strong, which goes back to my other point of how the company could come up with growth strategies, it seems like it can’t and is hoarding cash, which could be used more efficiently in rewarding its shareholders in some ways rather than holding on to the cash pile, which serves no purpose but to have the ability to pay off short-term obligations. The company’s current ratio is very strong but inefficient in my opinion because of the mentioned reason, and I would consider an efficient ratio to be in the range of 1.5-2.0. As of Q3 ’23, the ratio has come down to around 3, but it is still a little too high. It is, however, better to have a high ratio than under 1.

Current Ratio (Author)

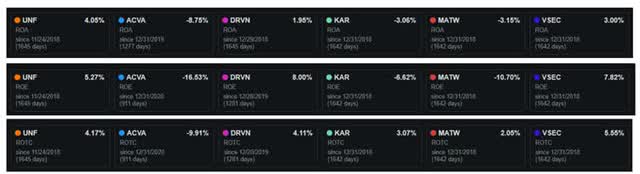

Speaking of efficiency and profitability, the company’s ROA and ROE trended down in the last few years which is a little concerning, however, this coincides with the management not utilizing the company’s assets very efficiently. How do these stack up against the competition? It seems that UNF is at the top of the range of the competition that Seeking Alpha suggests, which puts ROA and ROE into a different perspective. Low ROA and ROE are expected in this industry, so I am not too worried about how UNF is faring here.

The company’s return on invested capital is not very high and has been exhibiting a downtrend over the last while, which suggests that the management isn’t able to invest in projects that would offer a high return any longer and that the company may be losing its competitive edge and moat in recent years but if we also look at the competition, it seems that UNF is performing much better than most of the competitors.

Efficiency and Profitability vs Competition (Seeking Alpha)

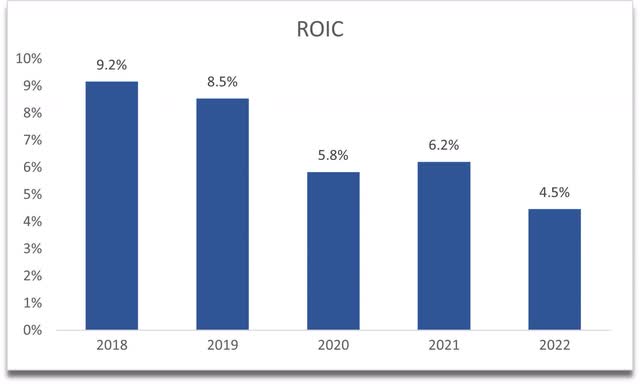

However, if we compare the company’s recent ROIC figures to its weighted average cost of capital or the WACC, we can see that the company is not creating value for investors since the WACC is about double the ROIC and that is not a good sign. I have calculated the WACC to be 8.2%, and since the company has no debt, UNF’s WACC is its cost of equity, which I found by using the CAPM.

Looking through in more depth, I can see that net operating profit after tax, or NOPAT saw a decent decline in FY20, which was the pandemic year. This drove down the company’s margins because the revenue was flat for that year while expenses continued to increase. Fast forward to FY22 and we can see that expenses went up more than the company received in revenue, which drove down ROIC even further after a slight uptick in FY21. 2022 was the year when inflation peaked at almost 10% in the US, and over 10% in the EU, which weighed heavily on production and labor costs for many companies, including UNF as the CFO said in an FY22 conference call:

Our operating results were also impacted by higher energy costs as a percentage of revenues as well as increased input and labor costs due to the current inflationary environment.” The company also mentioned that the margin contractions were attributed to extra costs of their three key initiatives:

Our financial results in the third quarters of fiscal 2023 and 2022 included approximately $8.4 million and $11.4 million, respectively, of costs directly attributable to our three key initiatives the CRM, ERP, and branding initiatives.”

Since we are moving away from such an inflationary period, I will look to see how the company’s ROIC developed when it announces its full-year FY23 results later this month.

ROIC (Author)

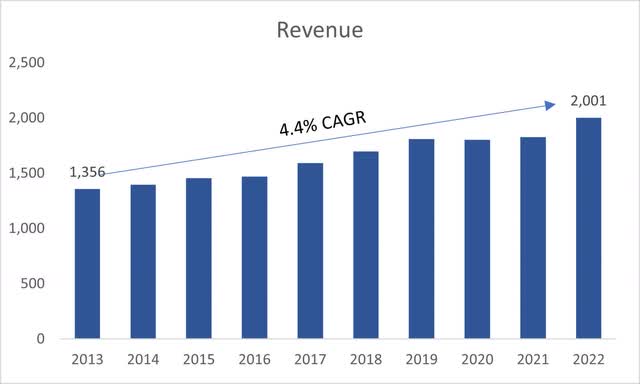

In terms of revenues, the company’s been growing quite slowly but with a clear uptrend. It is not the quickest growth I’ve seen, but given the company is relatively old, it’s decent enough I would say. Analysts see revenue growth for FY23 to be 11.4%, 7% for FY24, and 4.8% for FY25. Based on how well the first 3 quarters of the year went (all figures recorded low-teens revenue growth y/y), I will assign 11% for FY23 also.

Revenue growth (Author)

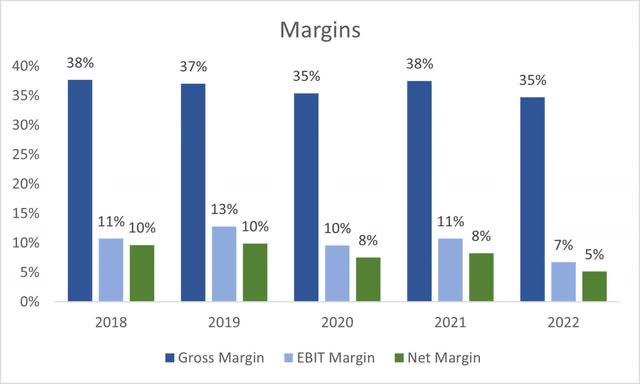

In terms of margins, these have also suffered at the end of FY22, which is not a good sign. Unfortunately, as of 39 weeks ended May ’23, the margins have only gotten worse for the company. Gross margins went down to around 33% and operating margins are down to around 6%, while net margins are at around 4.5%. I would like to see these stabilize and improve over the next couple of quarters, but looking into it further, we can see that the management is still spending quite a bit of money on three large initiatives (mentioned above), which are weighing on their margins significantly.

Margins (Author)

Overall, it looks like the company is going down the wrong path recently which is understandable given the macroeconomic environment we were/are in. However, because of these downtrends, I will have to assign a larger margin of safety to take on the risks of the company. The management is seeing further pressures on margins due to higher costs for the mentioned key initiatives and the inflationary environment, which I think shouldn’t be as impactful as it was earlier.

Valuation

As I mentioned earlier, I will anchor my assumptions for FY23 to the analysts’ assumptions of 11% for FY23, however, in the whole analysis valuation, the CAGR will be around 4.2% for the base case scenario because the management did not provide any inclination that the products will do much better going forward, especially with the type of macroeconomic environment we’re in where the inflation is still sticky and interest rates are set to stay higher for longer. I would also like to be more conservative when it comes to revenue growth for that extra margin of safety.

For the optimistic case, I went with a 6.2% CAGR, while for the conservative case, I went with a 2.25% CAGR for the next decade. These estimates seem to be reasonable to me and all are possible for the company.

Revenue Assumptions (Author)

In terms of EPS, the analysts see around $6.9 for FY23, $7.5 for FY24, and around $8.4 for FY25. I went with $6.80, $7.5, and $8.5, respectively. So, for my base case EPS growth I went with around 10% CAGR, for the optimistic case, I went with around 13% CAGR, while for the conservative case, I went with a 9% CAGR. These EPS figures were derived from assumptions on gross and operating margins. The management doesn’t see cost pressures subside for the year, so I went ahead and assumed the same because of this inflationary environment. For the future, I assumed that the cooling inflation will bring down costs over time, and the company will regain its profitability, just as the management also mentioned in Q3 ’23.

So certain supply chain, freight cost, overseas freight, raw material costs, we’re starting to see come down.”

Margin Assumptions (Author)

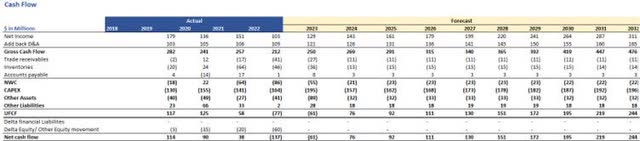

On top of these estimates, I went with a decent amount of margin of safety due to how profitability and efficiency deteriorated over the years and because the latest results are not showing any signs of improvement. I went with a 30% margin of safety. For the DCF valuation, I went with the unlevered free cash flow or UFCF assumptions that I derived from forecasting all the balance sheet items 10 years into the future.

Cash flow statement forecast (Author)

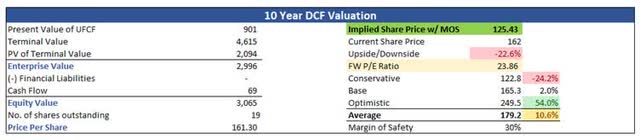

For the calculations, I used the WACC of 8.2% as mentioned earlier and I assumed the terminal growth rate to be 2.5% because that is the long-term inflation goal, and I would like a company to at least be able to keep up with it.

With that said, UNF’s intrinsic value and what I would be willing to pay to take on the risks of the company is around $125 a share, which means the company is trading at a premium to its fair value.

Intrinsic Value (Author)

Closing Comments

It seems like the company is too expensive for me right now if I were to take on the risks. A 22% pullback is also possible given the macroeconomic situation and the sector’s outlook. I’ve set a price alert around my PT, and I will probably forget about the company for the time being. I’ll check in on the following earnings reports to see how the margins have developed since the last report and reassess if necessary.

For the time being, I would like to see the financials of the company improve, not just the margins but the competitive advantage, and the efficiency and profitability metrics too. The biggest threat to the company’s revenues, the recession, seems to be subsiding and it looks like we are not going to see one coming for at least another year or so, however, that doesn’t mean it won’t change once we see more economic data coming out in the remainder of the year and the months following, as these predictions tend to change quite rapidly depending on how the economy is performing.

Read the full article here