Following up on my original article on Unilever (NYSE:UL) “New CEO Making Changes” from December, we can assess what the new CEO has done since then. On the whole, we see that he has already made a positive impact on the company. The company seems to be on the path of a successful turnaround, and Unilever has performed well over the past year; generating over 20% gains.

“We are focused on driving high-quality sales growth and gross margin expansion, led by our Power Brands. Over the first half, we made progress on those ambitions.

Underlying sales grew 4.1%, driven by a third consecutive quarter of positive, improving volume growth, while pricing continued to moderate in line with our expectations. Strong gross margin progression fuelled increased investment behind our innovations, and resulted in a step-up of our profitability.” (CEO Hein Schumacher, HY2024).

As noted by the CEO Hein Schumacher during the HY2024 results presentation, Unilever has stepped up its performance in both growth and profitability, which are key metrics for investors. As a result of these fundamental improvements, Unilever’s shares have increased in value.

We see further upside for Unilever shares next year, as the company keeps delivering on volume growth and will close a $20B deal for its ice cream division. Unilever is focused on generating shareholder returns, as it remains undervalued versus its competitors. We therefore rate Unilever as a “buy“.

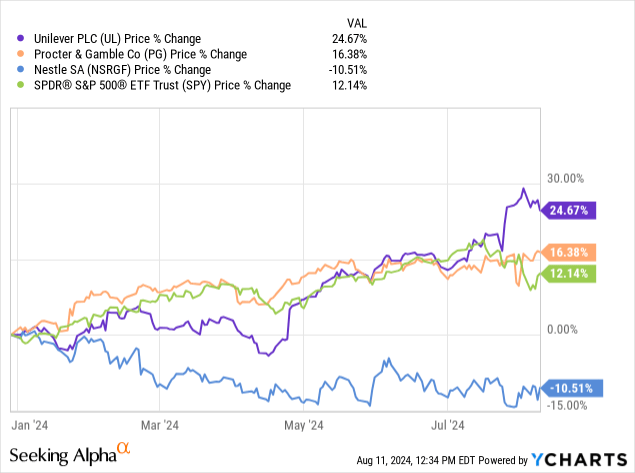

Recent Performance

In terms of shareholder returns, Unilever has delivered over 20% share price appreciation year to date, outperforming competitors like P&G and Nestlé by a wide margin. Unilever has also outperformed the SP500 over this period.

Significant Operational Improvements

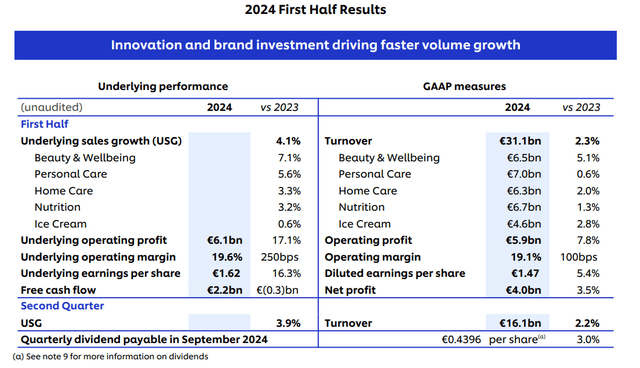

This share price appreciation is explained by improvements in underlying performance. Most notably, a return to positive volume growth and a margin expansion has improved key growth and profitability metrics, as shown below.

Financial Results (Unilever, HY2024)

This is a very impressive performance, growing earnings per share by 5.4%. This organic EPS growth is supported by a share buyback program of €1,5b and a progressive dividend policy, growing at 3%. Taken together, Unilever is delivering significant value for its shareholders.

Future Outlook and Catalysts

There is still more to come from Unilever. The company is focusing its efforts by investing more in its “power brands”, and its emerging markets exposure supports long-term growth. This strategy has paid off this year and I expect these trends to continue. Unilever remains well positioned and its beauty & wellbeing and personal care divisions are showing great results. The power brands in the beauty & wellbeing division are growing at double-digit rates.

Unilever has announced that it is separating its ice cream division valued at €17B, which is over 10% of Unilever’s total market cap. This division makes up around 15% of total revenues, but it has lower growth and has relatively more exposure in developed markets. Unilever is focused on creating shareholder value with it, possibly through a special dividend or a spinoff. The full separation of the ice cream division is expected to be completed end of 2025.

The separation of Ice Cream will create a world-leading business, operating in a highly attractive category, with brands that together delivered a turnover of €7.9 billion in 2023. The business has five of the top 10 selling global ice cream brands including Wall’s, Magnum and Ben & Jerry’s, with exposure in both the in-home and out-of-home segments across a global footprint. (Unilever, 2024)

Next to that, Unilever announced that it will be cutting about 1/3rd of office workers in the EU, thereby further lowering overhead costs and improving margins. While firing people is always difficult, Unilever has a substantially higher headcount than its competitors, and this decision seems fair from that standpoint.

Still Undervalued on a Relative Basis

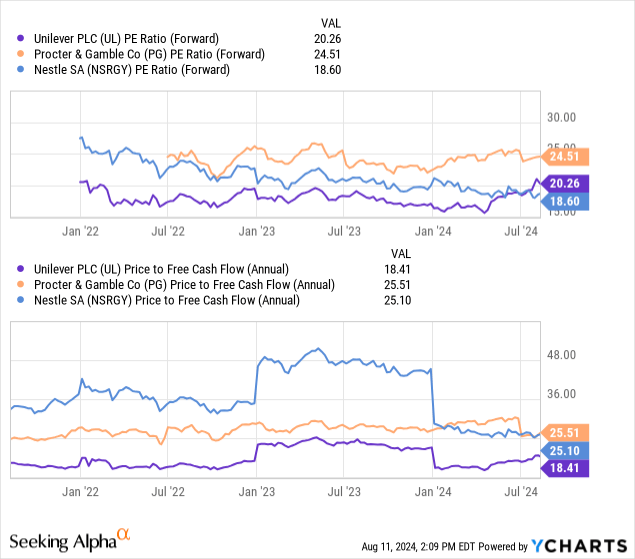

Unilever shares have been re-rated by the market, with a multiple expansion to 20 times forward earnings, which, we think, is a fair multiple for this business. This higher multiple is justified because growth expectations have improved for Unilever. The guidance for FY2024 underlying sales growth (“USG”) is between the range of 3% to 5%, with the majority of the growth being driven by volume that is higher quality growth than pricing. Moreover, Unilever expects underlying operating margin to be at least 18%, promising a year-over-year margin improvement that directly contributes to the bottom line.

Meanwhile, Unilever’s competitors such as Nestlé have reported declining revenues. While the gap in valuation has decreased between Unilever and its competitors, it still remains undervalued compared to Procter & Gamble (PG). Unilever’s sales growth guidance is the highest out of these three companies.

Risks

The margin of safety for Unilever has decreased after a 20% increase in share price this year, and investors have high expectations going forward for Unilever. Unilever needs to keep up its good performance to justify a higher valuation. Given the remaining initiatives by the new CEO, we believe that there is more to come in terms of operational improvements from Unilever.

Moreover, stretched consumer budgets have increased competition from private label (store brand) products. That being said, most consumers still prefer name brands, but Unilever should not let the price difference become too large. At the moment, private label takes up around 25% market share in the CPG category in the US. Private label competition is not new, and follows a cyclical pattern. Private label gained market share after a period of high inflation, but inflation is now normalizing again, which could allow consumers to return to their preferred name brands. Moreover, the private label issue seems to be a mainly European phenomenon with less penetration in the US and emerging markets. That being said, private label is a relevant risk for Unilever, who has significant European exposure.

Conclusions

We conclude that the company has made a number of significant operational improvements over the past year, as shown by both volume growth and improving margins. While the past year has already shown a lot of upsides, we believe that Unilever still has more potential for next year. We expect that the company will keep improving its growth and margins under the new CEO’s leadership. Most importantly, the Ice Cream separation is expected to unlock significant value for shareholders next year. Unilever is pulling off a successful turnaround and shows determination to maximize shareholder value.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here