United States Steel Corporation (NYSE:X) (USS) is finding itself in a peculiar position as the deal with Nippon Steel (OTCPK:NPSCY) is more heavily scrutinized as a national security risk. Despite these factors, the overall steel industry has fallen into a bear market, resulting in a -19% decline in net revenue and a contraction in aEBITDA margin to 10% on a year-over-year basis for Q2 ’24.

At this time, Cleveland-Cliffs is formulating a new deal to approach USS with if the deal with Nippon falls through, with an expected acquisition price somewhere in the $30s/share range. This suggests that X shares are presently fairly valued at an acquisition price. Assuming that USS will come to the table with Cleveland-Cliffs, I believe a fair price target will be $32.33/share at 7x eFY24 EV/aEBITDA, leading me to upgrade X shares to a HOLD rating.

If no deal comes to play, I believe X shares will be revalued closer to their historical trading range. If this scenario occurs, I believe my initial SELL rating for X remains appropriate for a price target of $25.92/share at 5.91x eFY24 EV/aEBITDA.

Be sure to read my initial coverage of the acquisition here:

U.S. Steel May Have To Face The Music

USS is finding itself in a more challenging position as the acquisition by Nippon becomes more heavily scrutinized by politicians on both sides of the aisle. President Biden recently announced his position in blocking the deal due to national security concerns, with VP Harris and former President Trump both stating that they would kill the deal upon being elected. Management at USS are adding some pressure to the deal, suggesting that the firm will be forced to close several steel mills due to the costs associated with refurbishing aging mills, which would result in a reduction of workforce.

Aside from political pressure as it pertains to the acquisition, the United Steelworkers Union has been adamantly against the acquisition. This suggests that an acquisition by domestic competitor Cleveland-Cliffs would be preferred, given the strong corporate/union relationship.

Up until now, Burritt has described USS as a world-class steel company, but now he is making baseless and unlawful threats, saying if the transaction with Nippon is rejected, the future of U.S. Steel as a viable steel company is at risk.

David McCall, USW President.

As part of the deal, Nippon announced a planned investment of $1.3b in USS union-represented facilities, in addition to the $1.4b committed. From the union’s perspective, the deal doesn’t make much sense given that Nippon has gone on record of honoring union contracts through September 1, 2026, a mere two years of work for the union workers. The USW made it clear early in the process of their support for an acquisition by Cleveland-Cliffs given the company’s prioritization of union labor.

On September 5, 2024, Seeking Alpha released a report citing the letter released by the Committee on Foreign Investments in the United States (“CFIUS”) stating that the organization found that the acquisition would pose as a national security threat.

The committee has identified risks to the national security of the United States arising as a result of the transaction. The consequences to national security that have been identified relate to the possible supply chain disruptions to sectors critical to national security, particularly transportation, infrastructure, construction and agriculture.

CFIUS

One of the factors often overlooked is Nippon’s historical relationship with the United States related to dumping steel on the open market. The International Trade Administration had found that Nippon had sold hot-rolled steel in the United States at prices below the normal value between October 1, 2019, through September 30, 2020, resulting in shipment restrictions placed on the steelmaker. I believe this factor is important in considering the deal, given that if Nippon were to acquire USS, Nippon could leverage the USS assets to circumvent any anticompetitive practices on the domestic front.

Despite USS turning down Cleveland-Cliffs on multiple bids, Lourenco Goncalves continues to show interest in an acquisition. Seeking Alpha reported on September 5, 2024, that Cleveland-Cliffs is actively working with various banks to raise capital to bid on the competing steel company. According to the report, the new bid would bring the offer down to the $30s/share range, significantly lower than their initial bid of $54/share in cash and equity. Despite this reduced premium, the acquisition price remains above USS’s $7b market cap before the bidding process.

Corporate Reports

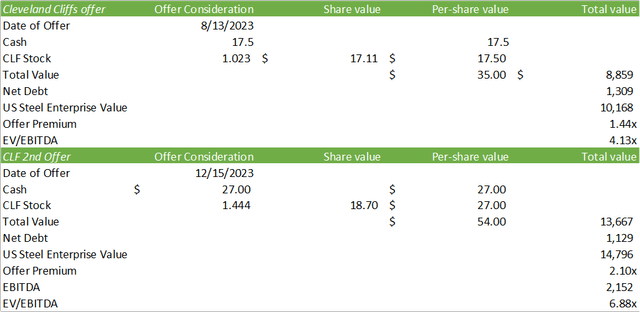

Looking through the historical bids for USS, Cleveland-Cliffs had initially offered $35/share and bumped the offer up to $54/share as more bidders entered the arena. The data below is an excerpt from my previous report on the subject.

Corporate Reports

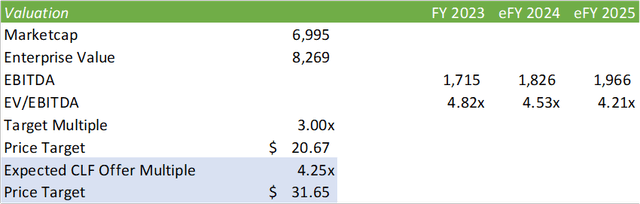

My initial valuation model for USS post-bidding war valued USS at $31.65/share. I would expect the new offer by Cleveland-Cliffs will be somewhere in the range $31.65-35/share.

Corporate Reports

USS Financials

Corporate Reports

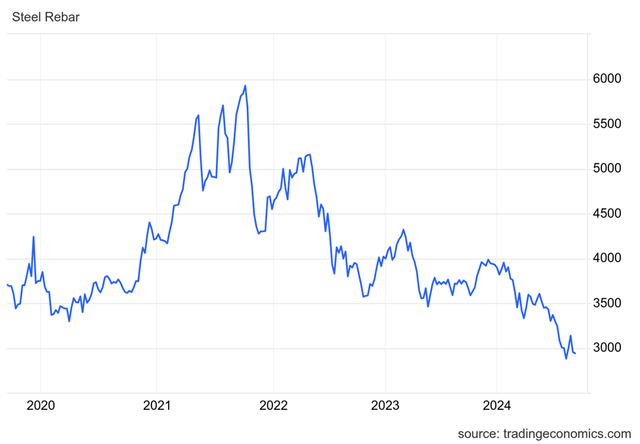

It has become clear that the steel industry has entered into a bear market, which has trickled down into USS’s operations.

TradingEconomics

For eq3’24, I’m forecasting USS to generate $3.66b in net revenue, with an adjusted EBITDA of $314mm. Looking out to eFY24, I expect revenue to come in at $15.7b with an adjusted EBITDA of $1.49b, a -16% decline in revenue when compared to FY23. Given the current state of the US and European economies, I do not believe the steel industry will emerge from this decline throughout the duration of CY24.

Risks Associated With USS

Bull Case

Despite the steel industry falling into a bear market, USS remains a prime target for an acquisition. Though I do not anticipate the USS/Nippon deal to go through, Cleveland-Cliffs remains at the table and is formulating a new deal with which to approach USS management.

Bear Case

If the USS/Nippon deal falls through and Cleveland-Cliff’s deal does not come to play, USS shares are at risk of being repriced to their historical valuation. Given the current state of the steel industry and the necessity for investment across USS’s assets, the firm may be forced to reduce their footprint, resulting in a deeper revenue and margin decline.

Valuation & Shareholder Value

Corporate Reports

USS is currently trading at a relative premium to its peers, given the M&A activity that has artificially elevated the share price. Given the price action post-acquisition announcement, I have reason to believe that the investment community does not expect the deal to go through. Considering USS’s peer valuations, X shares should be priced down to $21.68 at 6x EV/EBITDA on an unadjusted basis. This price target would assume that all deals are off the table and that USS would trade closer to its historical norms.

Seeking Alpha

Given my forecast for eFY24, I believe X shares should be priced closer to $25.92/share, also with the assumption that no deal goes through.

Corporate Reports

Given Lourenco Goncalves’ verbiage towards a new deal with USS, I would expect shares to be priced closer to 7x eFY24 EV/aEBITDA, pricing X shares at $32.33/share. This price target would put shares in the range of the current valuation of 5.76x trailing EV/aEBITDA. Given the narrow price dispersion and the likelihood of Cleveland-Cliffs coming back to the table with an offer within this expected range, I will rerate United States Steel Corporation shares with a HOLD rating with a price target of $32.33/share.

If no deal occurs, I believe X shares will fall back to a more normalized valuation of 5.91x EV/aEBITDA, pricing shares at $25.92/share based on my aEBITDA forecast for eFY24.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here