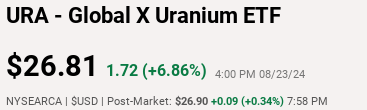

I have been a long-term bull in the uranium story, since before my retirement from active fund management in 2021. However, as a retiree with lots of hobbies and interests, I no longer have the time and patience to follow and invest in individual equities in the uranium mining space, many of which require hours of due diligence. That is why I own the Global X Uranium ETF (NYSEARCA:URA), as it provides me with diversified exposure to the uranium investment theme.

Since my last update in June 2023, a lot has happened in the uranium industry, including increasingly bullish developments on the geopolitical front as governments continue to ramp up their commitments to nuclear energy.

Spot uranium prices spiked to over $100/lb U3O8 in January on the back of negative supply news from Kazatomprom, the world’s largest uranium producer. However, in the subsequent months, we have seen a rout in uranium prices and uranium equities, as speculators took profits and Kazatomprom’s 2024 production was not as bad as feared.

However, with Kazatomprom recently announcing 2025 guidance that was materially lower than expected, I believe now is a good time to revisit the URA ETF.

Spot uranium prices normalizing to long-term contracted prices means many uranium equities are trading at fair value and the URA ETF is worth a buy for investors who are bullish on the long-term supply/demand dynamics of the uranium market.

Brief Fund Overview

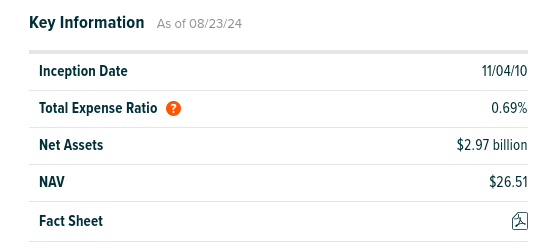

First, for new followers or those unfamiliar with the URA ETF, the Global X Uranium ETF is one of the longest-operating and largest funds focused on the uranium and nuclear industries with almost $3.0 billion in AUM. URA charges a 0.69% expense ratio (Figure 1).

Figure 1 – URA overview (globalxetfs.com)

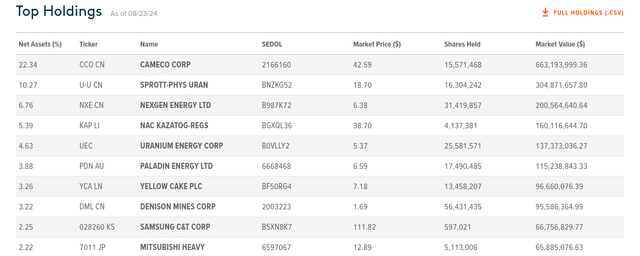

URA is fairly concentrated, with its top 10 holdings comprising 58% of the fund’s assets, and the top 3 holdings accounting for almost 40% (Figure 2).

Figure 2 – URA top 10 holdings (globalxetfs.com)

The URA ETF offers exposure to the nuclear power supply chain through uranium miners, mining explorers and developers, nuclear power component manufacturers, and physical uranium trusts.

Positive Nuclear Developments Continue

Since my last update almost a year ago, there have been a number of notable developments in the nuclear energy space.

First, at the United Nations Climate Change Conference in November (“COP28”), nuclear energy took center stage with 22 nations pledging to triple their nuclear energy capacity by 2050. Increasingly, governments are realizing that uranium is one of the greenest fuels and is critical if the world is serious about limiting carbon emissions.

Next, Kazatomprom, the world’s largest uranium miner, announced production issues on January 12. The combination of increased long-term demand and reduced short-term supply was a shot in the arm for the industry, with uranium prices spiking to over $100/lb U3O8 in January (Figure 4).

Figure 4 – Spot uranium prices (tradingeconomics.com)

$100 Psychological Level Spur Profit-Taking

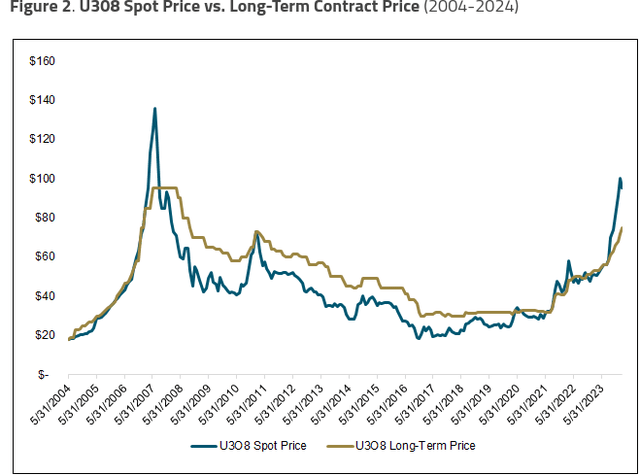

However, the spike in spot uranium prices above $100/lb U3O8 also spurred a bout of profit-taking, as many speculators have been sitting on large gains and spot price had run far ahead of uranium’s long-term contracted price (Figure 5).

Figure 5 – Spot vs. LT prices (Sprott Uranium Report)

For example, a major hedge fund in the nuclear energy space recently sold 2.7 million lbs of physical uranium to NexGen Energy (NXE) for US$250 million in convertible notes, or effectively $92.60/lb.

For those not familiar with the physical uranium market, uranium has two prices: a spot price that is commonly quoted, and a long-term price that is contracted between utilities and uranium miners. While the spot price is used by speculators and industry participants to manage their short-term inventories or speculate, most of the actual transactions in the uranium industry are conducted at the long-term price.

Selling Begets More Selling

What began as profit-taking by large speculators turned into a rout, as selling begets more selling and spot uranium prices declined by more than 25% to ~$80/lb by August. The URA ETF declined by more than 25% from its May peak, as uranium miners reacted negatively to the decline in spot uranium prices (Figure 6).

Figure 6 – URA declined by more than 25% (Seeking Alpha)

One key catalyst behind the decline was once again Kazatomprom, as the uranium miner surprisingly raised its 2024 full-year production guidance from 21-21.5k tons to 22.5-23.5k tons on August 1st (Figure 7).

Figure 7 – Kazatomprom raised guidance on August 1st (Kazatomprom August 1st operating update)

Kazatomprom Is The Wild-Card

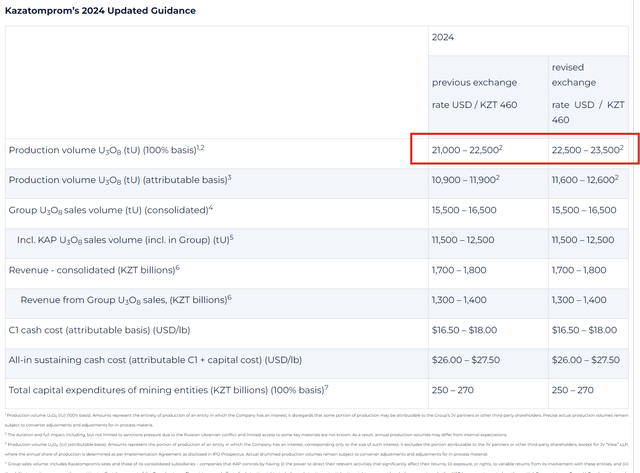

However, no sooner had Kazatomprom crushed uranium stocks with their August 1st operating update than they announced disappointing 2025 guidance that sent uranium stocks soaring on August 23rd (Figure 8).

Figure 8 – Uranium miners soared on Kazatomprom’s updated 2025 guidance (Seeking Alpha)

Instead of the 30.5-31.5k tons they had previously guided, Kazatomprom lowered 2025 production guidance to 25.0-26.5k tons of uranium. The main culprit for Kazatomprom’s reduced guidance is the uncertainty around the sulfuric acid supplies for 2025, leading to a delay in the company’s plans to expand production.

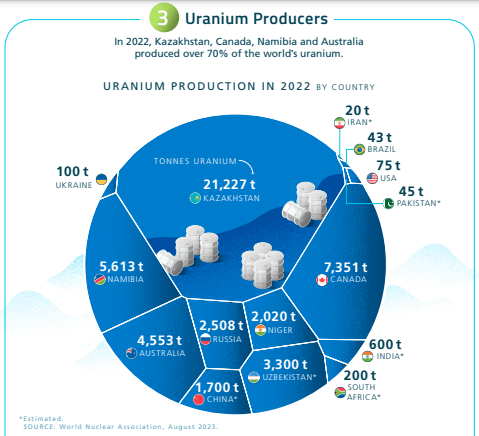

As the world’s largest uranium producer with ~25% of the world’s primary uranium production, Kazatomprom can literally move markets (Figure 9).

Figure 9 – World’s largest uranium producers (visualcapitalist)

Attractive Entry-Point For Long-Term Bulls

For long-term bulls like myself, I believe the recent market gyrations have presented an attractive entry point in uranium miners and physical trusts. With spot prices converging to the long-term price of around ~$80/lb U3O8 (Figure 10), much of the beginning-of-year speculative froth, when the uranium spot price was over $100, has been whittled away and many uranium miners’ valuations are now fairly valued.

Figure 10 – Spot uranium pricing come back to reality (Kazatomprom investor presentation)

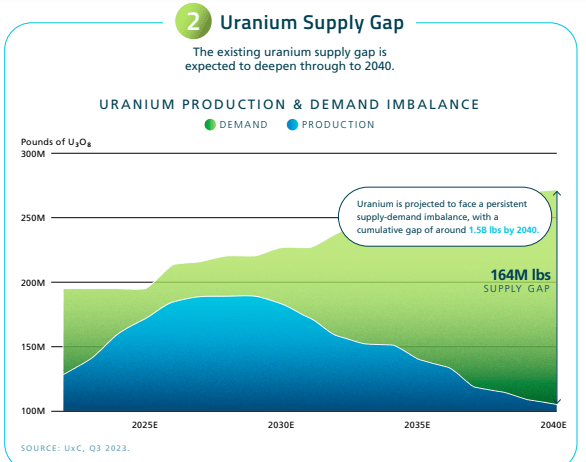

Considering the undeniable long-term supply-demand outlook, I believe now is a good entry point for those who have no exposure, or a ‘buy-the-dip’ moment for long-term bulls who took advantage of the January price spike to reduce exposure (Figure 11).

Figure 11 – Uranium in long-term supply/demand deficit (visualcapitalist)

Risks To URA

While I am bullish on the URA ETF, I need to remind fellow uranium bulls of the fact that the uranium market is very small and is prone to large gyrations based on incoming news, like what we have seen so far in August with Kazatomprom. URA investors should be mindful of market-moving catalysts like Kazatomprom’s earnings and operating updates.

Furthermore, over 20% of the ETF is invested in a single security, Cameco Corporation (CCJ). If Cameco suffers a production outage, the URA ETF could be negatively impacted.

Conclusion

The URA ETF is a convenient way for investors to participate in the uranium bull market with a portfolio of uranium producers, mine developers, physical trusts, and downstream suppliers.

With spot uranium prices recently converging with the long-term contracted price, I believe much of the speculative froth in uranium equities has been worked off and now is a good entry point for long-term investors. I reiterate my buy rating on the URA ETF.

Read the full article here