Vaalco Energy (NYSE:EGY) recently announced another acquisition, which I discussed previously, with which they will use cash to buy. Management spent less than a minute on this during the conference call (and then answered a few questions). But the larger concern is that management has really only made acquisitions with an extremely fast payback. The cash flow demonstrates a very high level of profitability that offsets at least some of the risk of where they do business. As management continues to diversify in this area, the strategy used for acquisitions should ensure some very generous cash flow growth in the future.

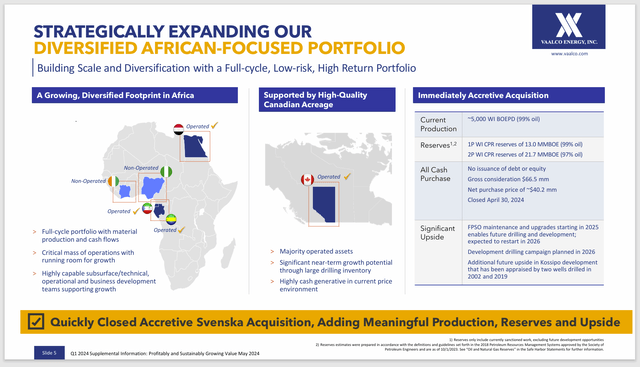

Map Of Operations

The company business in Western Africa is known for political instability. However, the offshore operations of the company have limited, if any, exposure to the onshore situation. So far, this idea is working much better than one would ordinarily think.

Vaalco Energy Map Of Operations (Vaalco Energy First Quarter 2024 Earnings Conference Call Slides)

Probably the most stable area are the operations in Alberta Canada. The supporting infrastructure and favorable government treatment of the industry in Alberta far exceed anything the company sees in Western Africa. Even the Ottawa government attitude is nothing compared to the African challenges of doing business.

The movement up the Western Coast of Africa is to a country where large companies like Murphy Oil (MUR) are active as well. This may mark a change in the company’s acquisition strategy towards more stability (and competition from larger companies).

To offset the risks and challenges of doing business in this area of Africa, management has demanded a fast payback on its money. Then, if the company needs to give up its operations, there has already been a significant return on the investment (on average) that in management’s eyes more than justifies the risk.

Egypt is an unusually stable country (in terms of the African continent) for doing business with a lot of aid from the government to oil and gas companies doing business in the country.

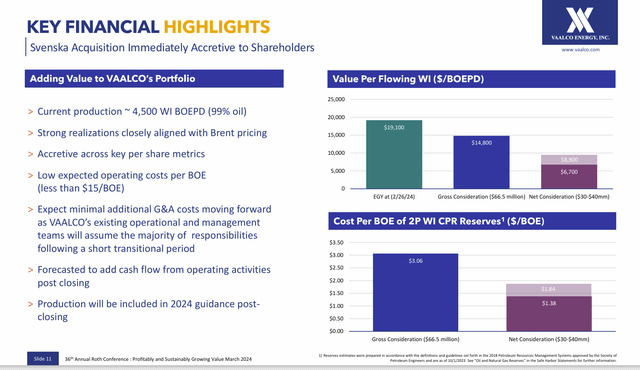

Latest Acquisition

Management is growing the company production through a combination of organic growth and acquisitions. The fast payback of these projects will enable an opportunistic acquisition every few years.

Vaalco Acquisition Benefits (Vaalco Corporate Presentation At Roth Conference March 18, 2024)

This latest acquisition (Svenska Acquisition) will be a non-operated acquisition. Therefore, a lot of fixed costs will be spread over more production to generate some cost reductions. Management specifically talks about general and administrative costs as the main beneficiary.

Canadian Natural Resources (CNQ) is the operator of this acquisition. This acquisition differs from others the company has made in that they will be repairing the ship that handles the commodity products produced in the next fiscal year.

As the company earns back the cash expended for the acquisition, that cash will likely go right back out again to handle the repairs. After that, there will likely be a drilling program, which will require still more cash. These cash requirements may affect the dividend policy and share repurchases over the next couple of years, depending upon commodity price levels.

Risk Mitigation

In all of the offshore operations, just about anything having to do with offshore is extremely expensive for a company of this size. Therefore, the company looks for established production (as in the case of the latest acquisition). Management also looks for the ability to drill development wells, which are a good deal less risky than exploration wells.

Older fields have established infrastructure, which lowers the cash outlay considerably. Having to fix older capital equipment is by and large not nearly as costly as building something new from scratch. It is also not as risky.

Management also restricts itself to largely looking at lower production levels to avoid as much competition as possible. That keeps the purchase price down.

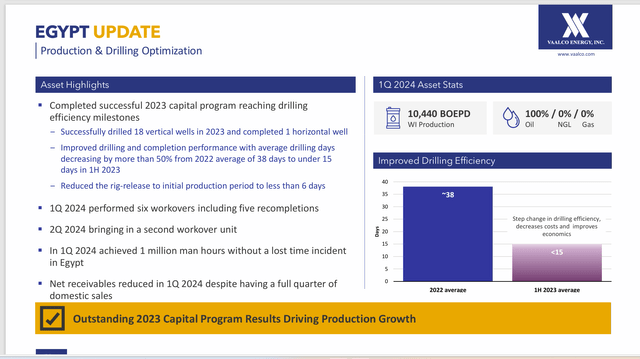

Egypt

As I noted before the acquisition of the TransGlobe business, the acquired Egyptian business has a new contract with the government that is far more favorable to the company than was the case with TransGlobe.

This new contract has enabled more activity on the Egyptian leases than I have seen in a very long time. Clearly, management is reinvigorating this business after previous management endured a long negotiating period.

Vaalco Summary Of Egyptian Operations Update (Vaalco Corporate Presentation First Quarter 2024, Earnings Conference Call Slides)

Management has tried probably the first horizontal wells in Egypt. These are largely abandoned older fields that the majors are not interested in. But a horizontal well with “modern completion techniques” could well revive some of these fields beyond market expectations.

Management has also expressed an interest in secondary recovery through water flooding. There were some large program possibilities that were not covered under the previous contract but are now allowed. Between these two new items, there could be room for considerable Egyptian production expansion for the first time in a very long time.

Continued technological advances sweeping the industry could make the situation even better in the future. Some of the progress already made is shown in the slide above. It will take some time for enough of these new wells to have an effect on reported results. But the results shown above are very promising.

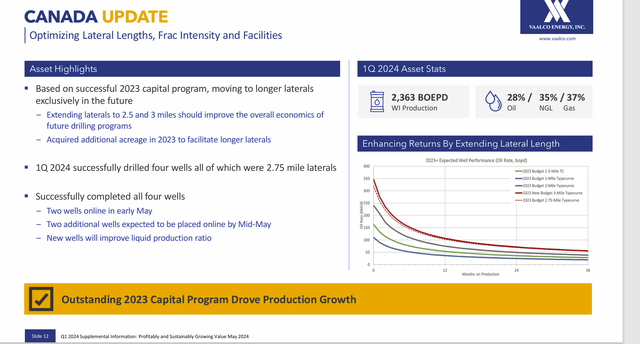

Canada

Canada is probably the most solid business and definitely a needed diversification from some of the risk taken elsewhere.

Vaalco Energy Summary Of Canadian Business (Vaalco Energy Earnings Conference Call Slides First Quarter May 2024)

Management is obviously working on getting production and costs optimized in Canada. Management had previously noted that they have roughly 50,000 acres to work with. After the first quarter, there was a press release giving a little more detail on the latest drilling campaign. For the first time in a while, management noted some acreage acquisitions.

Long time readers may remember that years ago, this purchase was made showing natural gas production. Management has made considerable progress in increasing the liquids production to make the production mix more valuable.

What needs to happen now if for management to figure out the best lowest cost option. To that extent, management is joint venturing some acreage to be able to drill longer more profitable wells. They are also likely doing acreage swaps and acquiring small acreage positions.

The result here is that they are clearly moving to a viable business model with a cash flow that results from obligations not long after the product is produced.

This varies considerably from what is happening in Africa, as management noted during the conference call. It can at times make cash planning far less challenging. That is in addition to the business attributes.

Summary

Vaalco Energy has found an operating niche in a commodity business that not many companies are particularly interested in. The latest acquisition likely moves it into an area of more competition, as shown by the presence of larger oil companies.

Financial reports will not mean much with a significant acquisition about to be completed in the near future, and it is even larger one in the previous fiscal year. However, it is important to watch that generous cash flow. That is an important safety measure until the financials become comparable again.

The other important part about the first quarter report is the large cash balance combined with no debt. Rarely do companies with no debt get into serious trouble that would involve investment principal loss in the long term. This is a very helpful characteristic, as the string of acquisitions and combinations make historical comparisons a challenge.

Still, management is making a “good living” off areas of Africa that many would not even think of trying to operate near or with those governments. Probably another big deal offsetting the risk of instability is that in many cases, management has its original money back plus profits. Therefore, any further investment is likely to be made with those profits, while the original investment money can be used for diversification.

A well-chosen basket of higher risk opportunities can itself reduce the overall business risk. Management appears to be pursuing that option.

As a result, this is a speculative strong buy opportunity where the strong balance sheet and continuing diversification program appear to be reducing the business risk of where this company does business.

Even though the risk of doing business is clearly elevated, this issue may appeal to some more conservative investors due to the strong balance sheet and conservative cash flow management.

Read the full article here