Let me start here by saying that I am a bagholder.

I have been wrong on Medical Properties Trust (NYSE:MPW). I have lost money on it. And I wish that I had taken the short sellers more seriously on this one. In hindsight, they were 100% correct, and they deserve credit for their successful call.

So keep that in mind as you read through this article. I have been wrong before and could be wrong again.

Even then, I still hold a small position as part of my portfolio. I never sold it because I have thought that its risk-to-reward remained attractive for more aggressive investors, especially following the crash in its share price.

However, I have stopped buying more of it as a result of my eroding conviction in the company, and the last quarter results didn’t help.

The market initially reacted positively to the results, but I was troubled by two things:

1) MPW Will Lose Ownership In Its Steward Hospitals in Massachusetts

About two years ago, MPW sold a 50% JV ownership in a portfolio of Steward hospitals to an institutional investor called Macquarie.

Steward

Boston Globe

This deal was then repeatedly used as an example to demonstrate that even sophisticated investors see value in MPW’s Steward hospitals.

Moreover, the deal was then also used as a case study to close more similar deals with other institutional investors to raise capital and pay off debt.

Well… MPW just announced that these Massachusetts hospitals will be returned to the lenders, marking a total loss for both: MPW and its JV partner, Macquarie.

Here’s what MPW said about this:

Due to unanticipated restrictions imposed by regulators that impacted the process of transitioning ownership of eight hospitals operated by Steward in Massachusetts, MPW – which owns a 50% interest in these properties through a partnership that has a separate master lease agreement with Steward – expects to relinquish its ownership of those properties to the non-recourse secured lender. As a result, MPW has fully impaired its equity investment in the partnership. The NFFO contribution of the joint venture in the second quarter was approximately $7 million, or $0.01 per diluted share.”

The immediate financial impact is not that significant to MPW because it had previously sold the 50% JV stake at a high value and also added a lot of debt on these properties.

But I fear that this massive failure will hurt MPW over the long run because it may discourage other potential JV partners from working with MPW.

Macquarie invested a lot of money into this, and they lost it all.

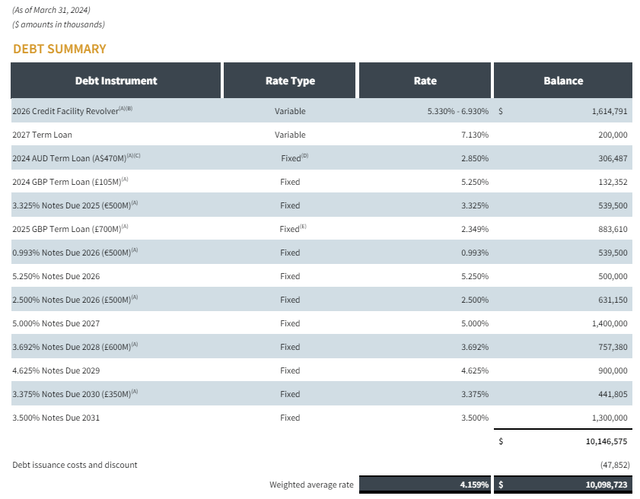

That’s a very bad look for MPW right as it is seeking additional JV partners to raise more cash and pay off the significant debt maturities that are coming its way:

Medical Properties Trust

MPW tried to explain on their conference call that this should be a one-off case and blamed the regulator for the loss, but I have learned to be skeptical of anything coming from MPW’s management, and this adds further doubt to their ability to release and sell the Steward properties.

2) Another Dividend Cut… Coupled Potential Share Issuances

MPW entered a deal with its lenders to ease some of its covenants and in exchange, it will pay a lower dividend to retain more cash until the Steward mess has been resolved.

The fact that they even need to do this is very concerning, and it is a strong reminder that MPW could well be a 0. It is heavily leveraged, has significant debt maturities coming its way, and interest rates are today a lot higher, even as its biggest tenant is still in bankruptcy.

With that said, cutting the dividend is actually good news to me. I have been calling for MPW to fully suspend its dividend for a while now. They should put everything they can towards deleveraging the company to assure its survival, rather than risking the long-term solvency of the company.

But the bad news here is that fully suspending the dividend does not seem possible according to them due to REIT regulations, even despite all their recent write-offs. On the contrary, they may need to issue a dividend in stock if their taxable income requires a payout in excess of $0.08 per quarter.

This would be highly dilutive to shareholders.

The Bright Side

On the bright side, they have surprised all of us by how many assets they have managed to sell this year. Here is what they said on their conference call: [emphasis added]

“On our last quarterly update call, we expressed our belief that we would exceed our $2 billion full year monetization target. And as Ed just pointed out, we have now executed more than $2.5 billion in year-to-date transactions.

Very importantly, virtually all of these, a total of roughly 50 hospital facilities in five major transactions have been executed at very attractive valuations, whether that’s based on capitalization rate, IRRs to us, real estate replacement cost, our initial investment and almost any other valuation metric, particularly in light of the diminished values that other real estate categories have suffered during the same period.”

That’s good news.

They have now raised over $2.5 billion, which has allowed them to pay off all debt maturities of this year and most of next year.

The big question now is whether they will manage to keep raising similar amounts of cash in the coming quarters, or will they hit a wall?

Most likely, they sold their best assets first since those would be the easiest to monetize, especially in today’s tough market.

This means that they now have fewer high-quality assets to sell and on top of that, potential buyers will look at the recent failure in Massachusetts and think twice before buying anything from MPW or entering a JV deal with them.

The issue is that they have another ~$3 billion of debt maturities coming their way in 2026 and 2027 and a lot of this debt was taken when interest rates were a lot lower.

If they face more similar setbacks as in Massachusetts, struggle to sell assets, and interest rates don’t come down enough, MPW could still be a 0.

On the flip side, if Massachusetts was truly a one-off, they keep making strong progress in selling assets, and interest rates come down materially by 2026, as is expected, MPW could strongly recover and double or triple in the coming years.

I continue to think that the risk-to-reward remains compelling, and I am happy to hold a small position as part of a well-diversified portfolio, but again, remember that I have been wrong so far and there is a clear speculative element to this thesis.

Read the full article here