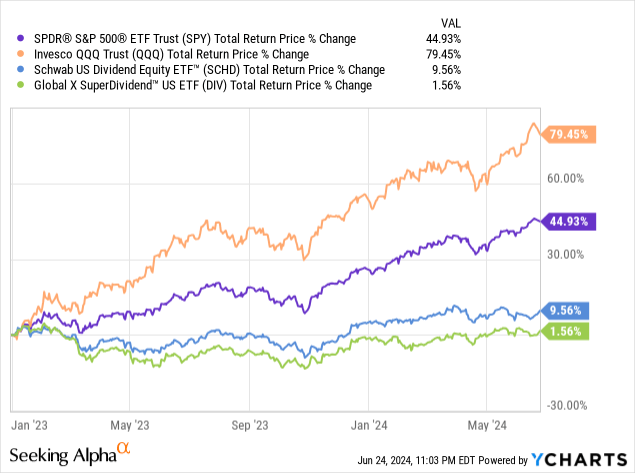

High-yield stocks (SCHD)(DIV) have significantly underperformed the broader stock market (SPY), particularly mega-cap technology stocks (QQQ) like Nvidia (NVDA) and Microsoft (MSFT), in recent years.

This underperformance is largely due to the rapid rise in interest rates since the beginning of 2022. Higher interest rates disproportionately impact high-yield stocks because they typically have more capital-intensive business models, making them more interest-rate sensitive. Additionally, high-yield stocks are often viewed as bond proxies, so higher interest rates mean that the market expects a higher dividend yield from them to compensate for the higher available returns from low-risk alternatives in the bond market.

However, recent news has been very favorable for high-yield stocks. This article will discuss this positive news and share some of the most opportunistic, risk-adjusted ways to profit from it.

Bullish Indicators For High-Yield Stocks

The most significant piece of good news is that – as my colleagues Jussi Askola and Austin Rogers recently pointed out – inflation appears to be under control and is likely to trend lower moving forward. This should pave the way for the Federal Reserve to cut interest rates in the near future. While the headline year-over-year CPI number of 3.3% in May was still above the Federal Reserve’s target of roughly 2%, a closer look at the data reveals a much more promising picture. First, CPI was flat sequentially. Additionally, if you remove shelter from the calculation, headline CPI was only 2.1% year-over-year, essentially in line with the Fed’s target. Core CPI, excluding shelter, was even more attractive at 1.9% year-over-year. This indicates that one of the main culprits keeping the headline CPI above the Fed’s target is shelter, which increased by 5.4% year-over-year. However, this is a lagging indicator, and it is highly likely that shelter inflation is much lower than the reported 5.4%. As a result, we expect the CPI numbers to trend lower in the coming months.

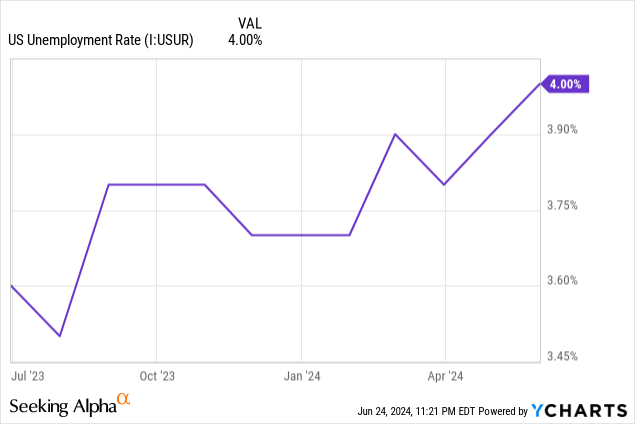

Another reason why interest rates are likely to head lower is the weakening economy. Unemployment has been rising steadily and is now around 4%.

Consumer confidence and spending are weakening, consumer and corporate debt levels are elevated, and consumer COVID-era savings have been completely depleted. Loan delinquencies are beginning to rise across the economy. Additionally, several of the U.S.’s leading trading partners, such as Japan, Great Britain, and much of Europe, are either in recession or close to it, while China is also facing substantial economic challenges.

Meanwhile, the Bank of Canada and the European Central Bank have also begun to cut rates, which puts further pressure on the United States to follow suit. Given the political pressure on the Fed to cut rates in an election year, combined with the exploding federal budget deficit due in part to elevated interest costs, we think that interest rates will likely decline in the near future, thereby providing a major tailwind for high-yield stocks.

Another reason for growing optimism about investing in the high-yield sector is the bloated valuation of the technology sector. The tech sector has become so richly valued that even industry stalwarts like Nvidia have begun to pull back sharply as their valuations appear to have gotten ahead of themselves. This trend could very possibly continue as the broader S&P 500, which is dominated by mega-cap technology stocks, is considered overvalued by several different valuation models. In contrast, the high-yield sector, especially sub-sectors like utilities (XLU) and REITs (VNQ), continues to be very attractively priced.

Additionally, many high-yield stocks, particularly those with quality balance sheets, have more defensive business models and can handle a weakening economy much better than some of the mega-cap consumer-facing companies like Apple (AAPL) and Tesla (TSLA), which rely on the sale of expensive phones and automobiles for their profitability.

Lastly, there is a significant amount of capital in private equity, particularly alternative asset managers that tend to invest in high-yield sectors like infrastructure, renewable power, midstream (AMLP), REITs, utilities, telecom, and data businesses, as well as private credit. We have already begun to see considerable consolidation in some of these sectors, with Blackstone (BX) recently going on a buying spree in the REIT sector and Brookfield (BAM)(BN) buying up several infrastructure businesses and assets. This trend is expected to continue, especially with the attractive valuations present in several high-yield sectors. This should serve as a major catalyst to drive valuations in these sectors higher.

Investor Takeaway

Given our bullishness on this sector and caution about the health of the economy, we believe that more defensive, high-quality high-yield stocks such as triple net leases (Realty Income (O) and W. P. Carey (WPC)), investment grade midstream businesses (Enterprise Products Partners (EPD) and Enbridge (ENB)), and quality infrastructure businesses (Brookfield Infrastructure Partners (BIP)(BIPC) and Brookfield Renewable Partners (BEP)(BEPC)) are among the most attractive risk-adjusted opportunities right now. Each of these trades at significant discounts to their historical average valuations and offers very attractive current yields along with solid long-term growth prospects while being backed by strong balance sheets and defensively positioned business models. Consequently, we are increasing our allocations to infrastructure, real estate, and midstream assets accordingly.

Read the full article here