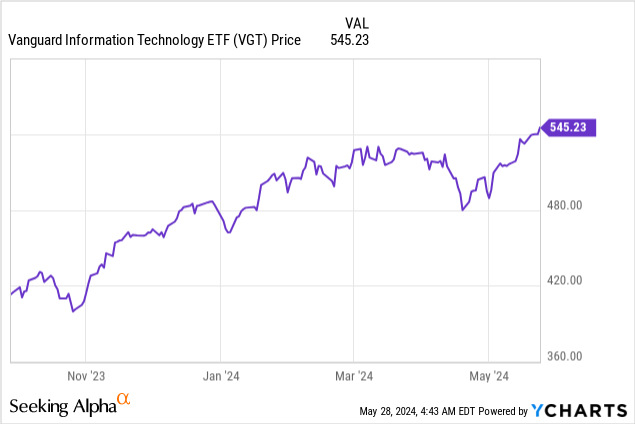

For investors who prefer to be passively invested in big tech, the Vanguard Information Technology ETF (NYSEARCA:VGT) charges fees of only 0.1% and offers a dividend yield of 0.66%. Since my last coverage in the article entitled: “VGT ETF: Buy Based On Productivity Gains And Generative AI” in September last year, it has gained more than 35% and is now trading at $545 while during this time the S&P 500 has appreciated by only 24%.

About eight months later, this publication aims to show that it is still a buy thanks to the broadening of VGT’s artificial intelligence base or more of its holdings now participating in innovation while, at the same time, there is an acceleration in the earnings growth for the IT sector. However, it is important to factor in the risks posed by high inflation and economic growth slowing further.

An Outperformance Largely Explained by the Innovation Factor

Coming back to VGT’s outperformance of the broader market, this was due to the innovation factor. In this case, holding Nvidia (NVDA) has repeatedly beaten earnings and analysts’ estimates after enjoying pent-up demand for its AI Superchips, which partly helped VGT’s upside since September. Moreover, the semiconductor giant has also been at the center of this massive investment boom, uplifting the stocks of companies that use its advanced GPU accelerator chips to offer cutting-edge applications, one of them being Microsoft (MSFT).

investor.vanguard.com

Moreover, the software giant has seen more traction for its intelligent cloud segment, a key enabler for companies to consume AI in an as-a-service mode, especially those who cannot afford to buy GPUs directly, and instead opt for monthly subscriptions. Note worthily, its strong partnership with OpenAI, where it has made a $13 billion investment, has enabled it to rapidly embed chat-based into its Office, security, and search products. In this way, it has overtaken competitor Alphabet (GOOG) which dominated the field earlier.

Even companies like Apple (AAPL) which has lagged behind Samsung (OTCPK:SSNLF) in incorporating Gen AI into its iPhone product line could make a related announcement at its annual developer conference next month, but, in the meantime, the iPhone maker has made progress in its services business enabling it to deliver both top-and bottom-line beats during its latest reported quarter.

Looking further, the ease with which Nvidia is managing to sell its GPUs shows companies do not want to be left out of the artificial intelligence race, which raises the question of AI productivity or better profitability for those who invest in the technology. Thus, based on research by McKinsey covering areas like Advanced Electronics and Semiconductors, Telecommunications, and High Tech including robotics, software development, and cloud computing, I had estimated $31.39 billion of annual productivity gains for companies operating in the IT sector from 2023 to 2040. This implies the average net income margins for VGT’s holdings could improve by 6.83%. Based on this, I had predicted a 9.6% upside, which has already been exceeded.

The reason for moderation is at that time, not all of VGT’s holdings were in the AI game, as exemplified by Oracle (ORCL) which was seeing declining sales in its cloud at that time. However, things have changed since then.

Broadening of VGT’s AI base and Acceleration in Earnings Growth

First, Oracle is now a darling of AI investors after it introduced a new database technology specifically for artificial intelligence, called Database23ai, which allows software developers to generate data-driven applications more easily. It has also massively invested in Nvidia’s GPUs to such a degree it can even lease spare capacity to xAI, Elon Musk’s company, in a potential deal valued at $10 billion.

Second, other companies have positioned themselves in the AI semiconductor space, namely Advanced Micro Devices (AMD) has emerged as a competitor to Nvidia with its MI300-series AI GPUs this year and boasted $3.5 billion worth of preorders. This is not much compared to Nvidia’s Data Center revenue of $22.6 billion obtained during its latest reported quarter, but, the fact that hyperscaler Microsoft is using its chips shows that AMD has potential in AI infrastructure.

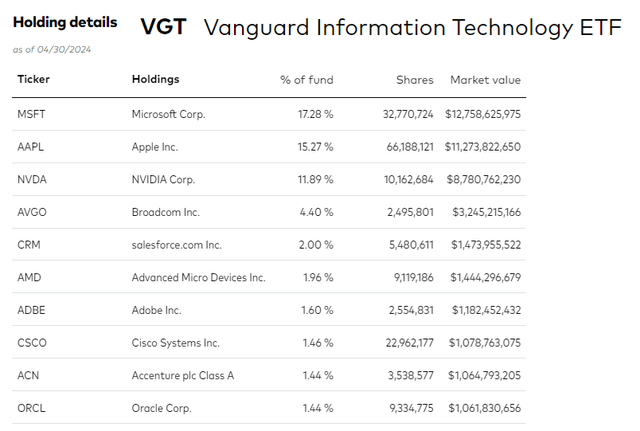

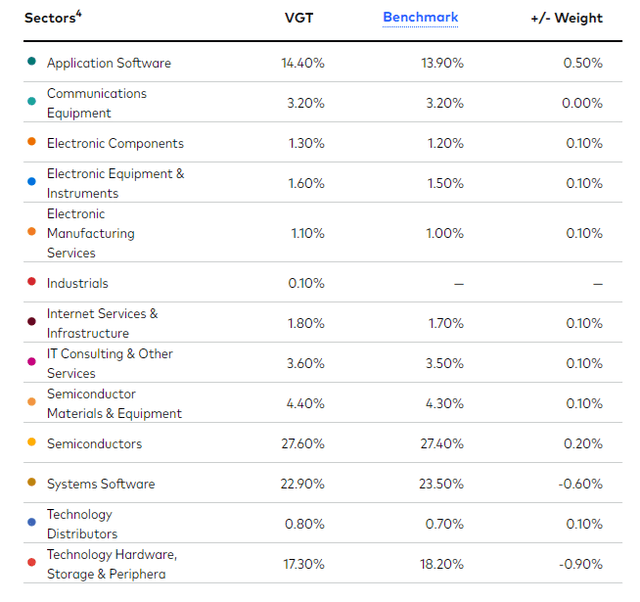

In this respect, the advantage of owning VGT’s shares is that one gets exposure to both chip stocks in a single investment, while the ETF’s sector-wise breakdown shows that its holdings are present across the whole IT ecosystem as shown below. For this purpose, it tracks the MSCI US Investable Market Information Technology 25/50 Index.

investor.vanguard.com

Looking at the Communications equipment sector, Cisco (CSCO) has inked an agreement with Nvidia to facilitate the deployment of AI infrastructures and could become a major player as enterprises try to connect massive amounts of data using open Ethernet instead of the proprietary InfiniBand technology. Talking figures, there could be around $3 billion worth of opportunities in hyperscale-over-Ethernet AI switches.

Therefore, the AI base has broadened considerably, which is confirmed by FactSet, a financial data and software company that found that artificial intelligence was the focus area of more S&P 500 companies during the Q1-2024 earning season, more than any other time over the past ten years. Thus, 199 companies cited the word “AI” and, out of these, 91% were from IT, a sector that was among the eight recording YoY revenue growth.

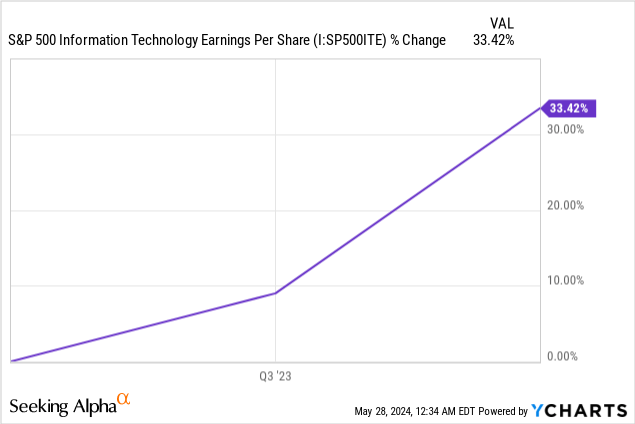

Talking profitability, the latest earnings growth for the S&P 500 Information Technology Index stands at 33% compared to about 20% YoY at the end of the third quarter of last year, or around the time of my earlier piece, signifying an acceleration of 65%.

However, this acceleration is not reflected in VGT’s valuations.

The reason is that it currently trades at a PE of 33.9x or only 2.4% above its value of 33.1x in September last year, which means that the share price does not fully reflect the 65% increase in earnings growth. Now, considering an increase of 9.6%, or the same percentage as last year, this yields a PE of 37.2x (33.9 x 1.096). This translates into a price target of $595 (543 x 1.096) based on the current share price of $543.

In this respect, given more stocks are investing in AI and talking about innovative terms like LLM (large language models), there is considerable share price appreciation potential, and the value of 37.2x may seem on the low side but, I believe it is justified because of the risks.

The Risks related to Inflation and Economic Growth

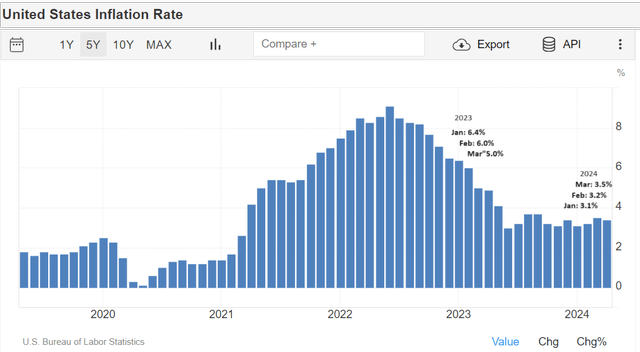

In this case, investors will note that earnings growth is inversely correlated to inflation. Hence, last year CPI was at 5% to 6% as shown in the figure below, whereas it was in the 3.1% to 3.4% range in the first quarter of this year. Digging deeper, a deceleration in the inflation rate conversely increases the disposable income available to corporations for procuring AI products and services. This has, in turn, helped VGT’s holdings to drive sales and profitability higher.

Initial chart obtained from (tradingeconomics.com)

However, persistently high CPI figures during the 2024 period as shown above show that the Federal Reserve’s battle against inflation is not yet won. Also, while most of the increase in CPI is caused by shelter and auto insurance, one should not forget innovation. As such, with so much money being poured into AI, right from GPUs, power and cooling systems in data centers, software development, and recruiting talent, it would not be surprising that the billions of dollars of tech investments end up driving CPI up unless there is an increase in labor productivity.

At the same time, the first quarter GDP growth was 1.6% on an annualized basis, a deceleration compared to the 3.4% in the previous quarter. Even then, despite the restrictive monetary policy and inflationary pressure, the fact that 78% of S&P 500 companies delivered positive EPS surprises, tends to show that the economy is showing resiliency. Contributory factors likely to be mentioned by the Bureau of Economic Analysis include the strong productivity level in addition to domestic demand, and robust labor participation.

Still, do expect volatility risks around June 11-12 during the next FOMC (Federal Open Market Committee) meeting, as the focus will likely be on inflation and how hawkish the U.S. Central Bank is prepared to be, especially in case the economic outlook deteriorates further.

VGT offers Better Risk-Return Tradeoff

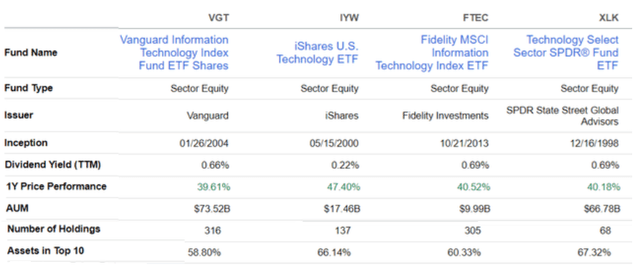

Still, investing in tech involves a higher risk-return tradeoff, but, as per the peer comparison table below, VGT does a better job at limiting concentration risks while still delivering a one-year performance of 39.6% which is less than 100 basis points below the Technology Select Sector SPDR Fund ETF (XLK), another popular passive investment. To this end, Vanguard’s strategy consists of including more stocks in its portfolio as tabled below, resulting in relatively fewer assets forming its top ten holdings or 58.8%.

Comparison with peers (seekingalpha.com)

In conclusion, an investment in the ETF continues to make sense as the upside could go further up. This is mainly based on the broadening of VGT’s AI base and an acceleration in earnings growth, which has not yet been fully priced in its share price. As for productivity, an article entitled “America’s Labor Productivity Sets it Apart”, by TD Economics, helps to put things into perspective. It states the recent acceleration in productivity which began after the pandemic and was rather cyclical in nature may last longer as the adoption of AI gains further traction and technology becomes more embedded in business processes.

In other words, a higher productivity level could offset the effects of wage increases and help in the fight against inflation, and, to this end, VGT’s holdings can deliver innovative technologies to the U.S. economy and continue to drive earnings growth. This is amid a conducive IT environment where spending should increase by 8% YoY in 2024 as, in addition to conventional expenses, companies also allocate some money for planning Gen AI projects, according to researchers at Gartner.

Read the full article here