VICI Properties (NYSE:VICI) is the 11th largest REIT by market cap, with a large presence in the entertainment industry, such as gaming, hospitality, and others. I started analyzing this REIT after its shares showed mediocre performance in recent periods, which caused the multiples and dividend yield (currently close to 6%) to fall to an attractive level.

In addition, I was surprised as I realized that VICI properties have more moats than I thought in the pre-analysis, with a very resilient business model and interesting growth possibilities. Despite this, there is a certain complexity to the analysis, with a high cost for portfolio expansion and returns that still have a level of uncertainty in the long run.

VICI Have More Moats Than I Thought

VICI is a relatively recent IPO, made at the end of 2017. Since then, there has been excellent shareholder value generation, with an adjusted EBITDA growth of 330%, which has allowed for enormous diversification and less dependence on players like Caesars (CZR). The amount of this investment was $37Bn, making the REIT the largest owner of Hotel Room Real Estate in America, with more than 60,000 hotel rooms, more than 4.2MM square feet of gaming space, as well as a number of other complementary things, such as outlets, meeting spaces, golf courses, and entertainment venues.

The first factor that draws attention to VICI is that its portfolio is 100% triple net leases, mitigating the complexity of the operation and the need for capital, but there are many other factors that highlight its resilience. Its clients are generally very large and also recognized for their location, which means that the average rent per asset is multimillion, more specifically, $32.85 million and this with an average lease term of 42 years, the overwhelming majority being long-term CPI protected.

As mentioned in the first section, there is a high cost for asset development, especially in premium locations such as Las Vegas. This is a strong barrier to entry, especially considering that prime real estate on LV’s main streets is already taken.

In my opinion, the most counterintuitive thing was the stability of rent collection in this sector. Because it is focused on experiential, gaming, and the like, my first impression was that because it is something superfluous, in delicate economic times, such as the COVID-19 pandemic, or scenarios of high inflation, interest rates, and higher levels of unemployment, this sector would tend to suffer first. But in fact, what was observed was different: in 2020, VICI achieved 100% Rent Collection, while other triple net lease REITs achieved between 70% and 99%. This was made possible by several factors, but especially by the solidity of their clients and the quality of their properties, since they wouldn’t want to risk losing access to the location due to rent arrears.

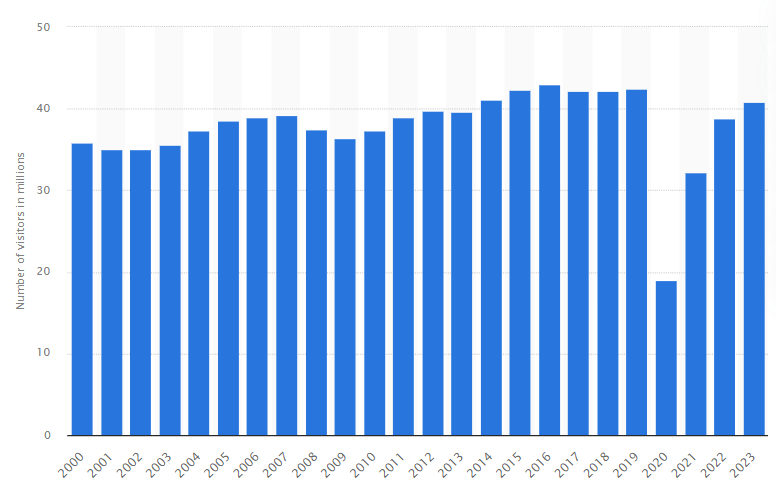

When we look at the evolution of tourists to Las Vegas from 2000 to 2023 on Statista, this number showed an upward trend and a rapid recovery in the post-COVID-19 period. Although the number decreased last year compared to 2019, the upward trend seems to be continuing, with industry experts saying that Las Vegas has eliminated seasonality and seems busy all year round.

Number of visitors to Las Vegas in the United States from 2000 to 2023 (In Millions) (Statista)

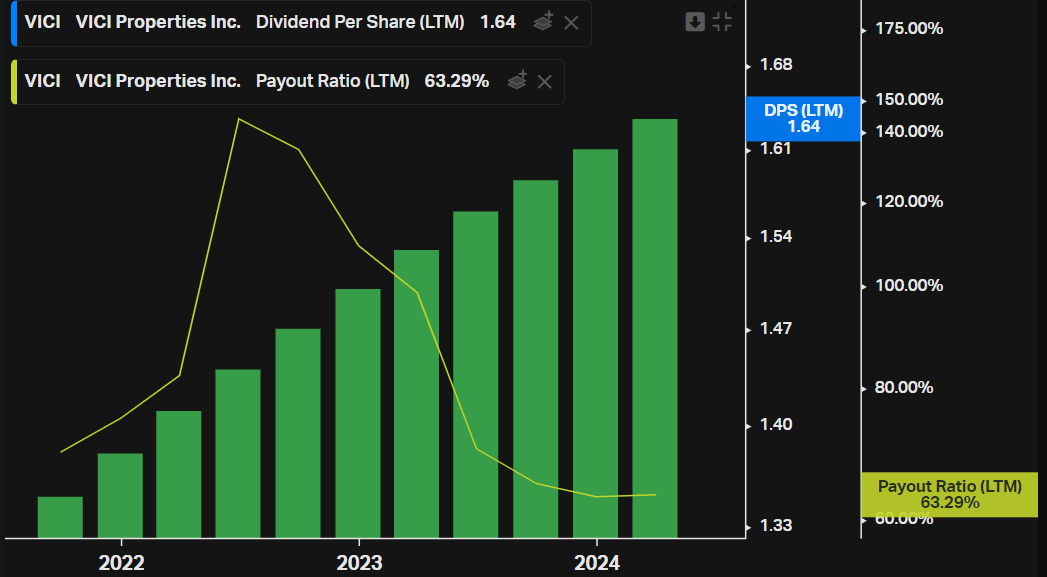

These characteristics of pricing power, dominance in premium locations, and a very high barrier to entry (through high costs and high regulation) translate into large moats for VICI, which end up being reflected in its financials, such as high margins (92.5% EBIT Margin) and great growth. To illustrate, below is a graph that every REIT investor likes to see, a Dividend Per Share advancing consistently in recent years, while the payout remains at very controlled levels (~63%). In the last 3 years, the CAGR of this DPS has been 8.3%.

Koyfin

Could VICI Sustain This Growth?

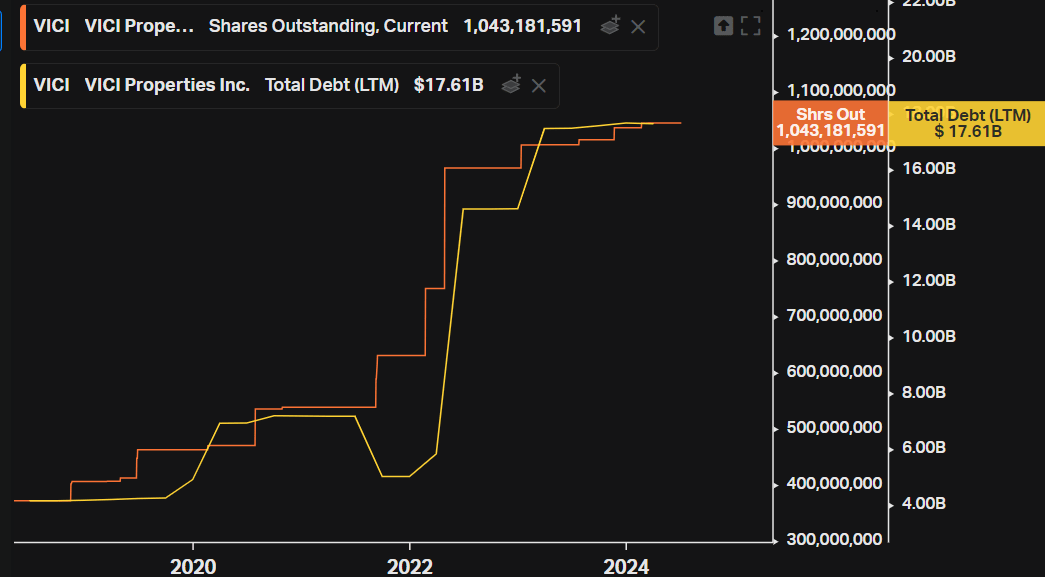

The main question mark of the thesis is whether VICI will be able to maintain this growth in a sustainable way. The tricky part of the thesis is that in order to achieve this track record of strong growth, a lot of capital was needed, which is very common for REITs, and even more common considering the segment and the ambitious projects that VICI has undertaken. Note that the number of outstanding shares has more than doubled since 2018, along with its total debt, which already stands at $17.6 bn. So it’s a bit difficult to perpetuate all this growth ad infinitum.

Koyfin

It’s worth mentioning that its net leverage ratio is 5.4x, a very comfortable capital structure for such a solid and predictable REIT. So I don’t think the complex part lies in the capital structure, but rather in future growth. It’s not very obvious how profitable expansion can be, will all this stock and debt issuance find projects with a cap rate as good as the most recent history, i.e. yields above 7%?

For the short term, it seems so. The cap rate spread of the new investment in the Venetian is quite attractive, higher than that seen in other markets. According to the words of VICI’s CEO “[…] there’s just nowhere else in today’s triple net lease market where you can put that amount of money, $700 million up to, to work into that kind of irreplaceable real estate at a 7.25% cap rate[…]”

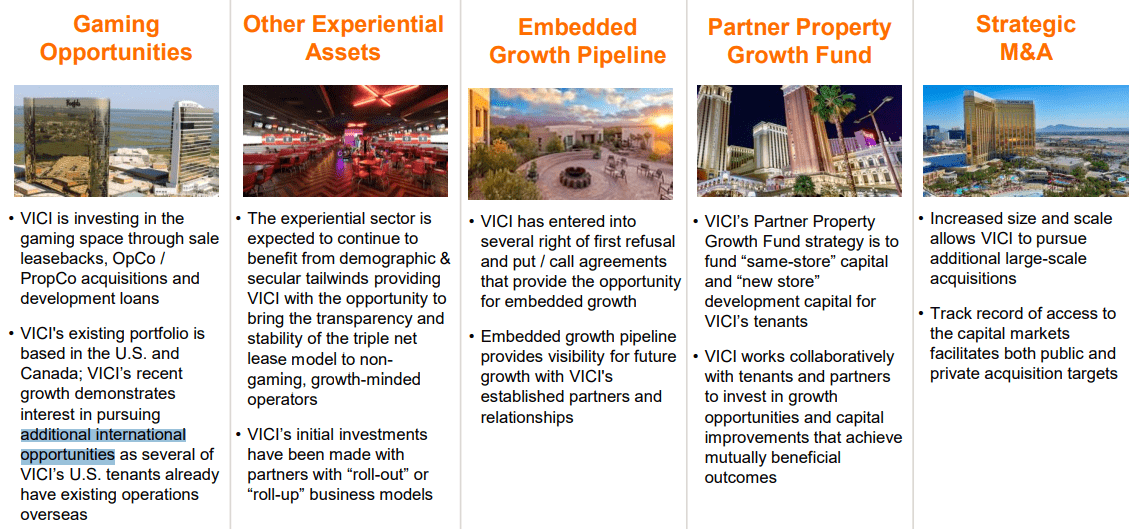

In the medium term, there also seem to be opportunities just as interesting, with a list of put/call and ROFR agreements for the possible acquisition of interesting properties, including some with a cap rate close to 8%. Other than that, VICI already owns about 26 acres of undeveloped land adjacent to the LINQ in Las Vegas, which should unlock value in the medium term in the future and expand its portfolio, my guess would be by something close to 5% counting the other 7 acres of Strip frontage property at Caesars Palace. Along with expansion through partners and their already developed properties, there are other things that VICI can explore to maintain interesting growth, such as new avenues of growth in alternative assets (Wellness, Youth Sports, Family Entertainment Centers, and others), and also expansion into new geographies.

VICI Properties

Although I mentioned that it is not plausible to project aggressive growth ad infinitum, I believe it is reasonable to believe in the company’s management. There is a range of interesting opportunities, which together with the large moats and different dynamics of this market (such as low cyclicality, and high entry barrier because of costs and regulation) should mean that the REIT will maintain an interesting and sustainable CAGR over time, something around 4% and 5%. What corroborates this figure is a study by Mordor Intelligence, which shows that the Casino Gambling Market is expected to deliver a CAGR of 4.95% between 2024 and 2029, reaching a level of $191.4 bn, growth driven by a number of factors, such as the popularization of online casinos attracting new audiences and interest in this type of tourism. It’s worth mentioning that VICI isn’t just about gambling, so it also benefits from other types of leisure tourism, such as concerts and the like.

In short, I give the benefit of the doubt that the medium- and long-term execution will remain solid, with an allocation of capital that will prioritize the shareholder through attractive and sustainable investments. Even so, it is necessary to continue monitoring the investments that the company has been making, together with raising capital through the issue of shares and debt.

The Current Valuation Presents an Attractive Opportunity

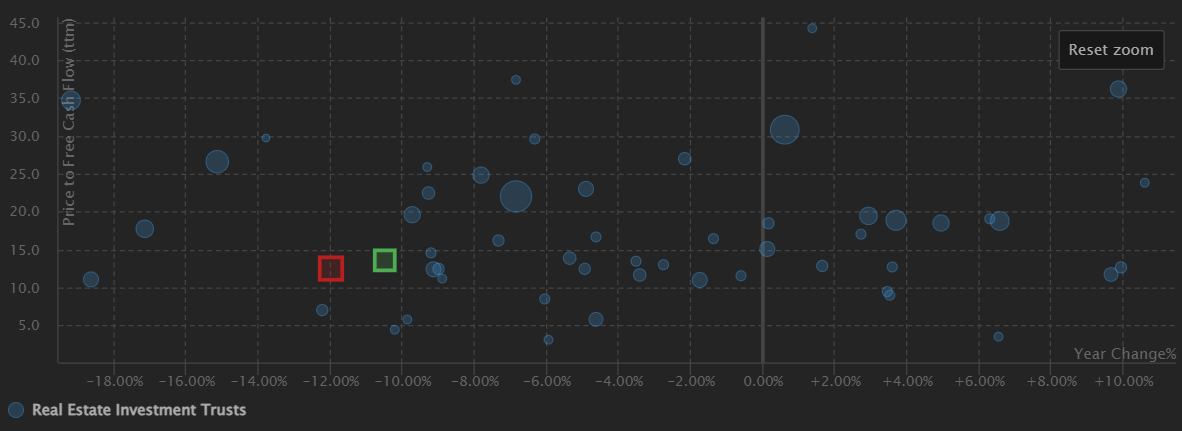

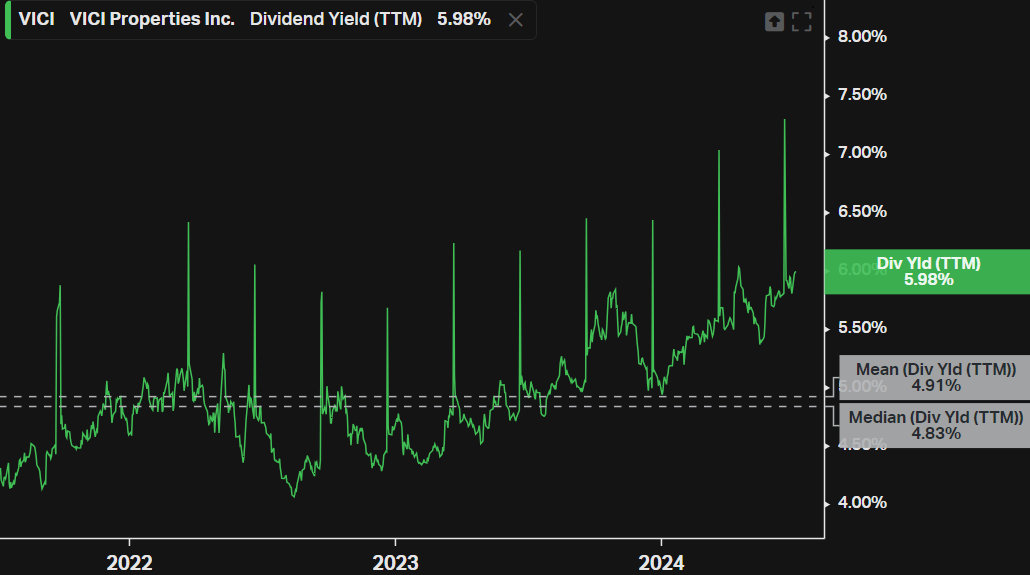

VICI stocks are close to the 52-week range low, trading at a forward P/FFO of 10.98x and a dividend yield of 5.98%. In the chart below, I’ve highlighted two REITs, VICI in green and Realty Income (O) in red. Both caught my eye because they performed poorly year to date and are trading at less than 15x their Free Cash Flow, despite being among the largest REITs by market cap (indicated by the size of the bubble) and also being resilient.

TrendSpider

This drop in the Year to Date has made the valuation of VICI very attractive, with the stock trading at a dividend yield substantially higher than its history. Over the last 3 years, the mean yield has been 4.9%, while the median has been 4.8%, so I see the current yield of almost 6% as an attractive level to be exposed to.

Koyfin

I only consider this level attractive because it seems plausible to me that VICI will maintain interesting growth over the next few years, causing the yield on cost to advance steadily and gradually. By applying a Gordon model with the following assumptions, it is also possible to find a fair value of $27.67 per share.

-

Next Year’s Dividend: $1.66

-

Discount Rate: 10%

-

Annual Dividend Growth Rate: 4%

Note that these assumptions are conservative, with a discount rate that guarantees an interesting annual return and a growth rate of 4%, which is entirely possible given market trends and possible investments, meaning that positive surprises could be seen along the way, with the VICI unlocking more value or the market changing its perception.

Despite this, I wouldn’t count so much on multiple expansions. Although 11x FFO sounds attractive and with a slight room for expansion (if we think that the right thing would be to trade at 12.5x, the upside would be ~13%), it seems to me that there is little relevance for this to weigh on the investment decision, the most coherent being to buy for the high FFO yield and hold the stock, benefiting from future growth and reaping the rewards through distributed dividends.

Reinforcing the Risks and Challenges

As stated before, the characteristics of VICI’s operations mean that expansion requires a high level of capital for development, which together with strong regulation in the gaming industry and consolidation in areas such as Las Vegas (although there is still room for construction and innovation, through verticalization and the like) makes growth in this sector less than trivial. If we think of a scenario where there is a decline in this market and few attractive options, if VICI continues to issue shares and/or raise debt to invest in properties that will bring lower returns, this could destroy shareholder value. I don’t think this is the base scenario, but it is something that should be monitored.

Also, although the capital structure is healthy, the shorter maturing debts (with some obligations as early as 2025 in the amount of $2 bn), could put pressure on cash momentarily and reduce the ability to grow dividends or make them resort to issuing more shares, diluting the shareholder.

Apart from other macroeconomic risks, the current dependence on the casino market (and even on some specific players such as Caesars) and the like is also something that should be monitored, even with other properties, if there are any very negative surprises in this sector – such as regulatory shifts, changes in consumer preferences, competition in other geographies and similars – this directly affects VICI, unlike other REITs in more “traditional” markets, better diversified and with more secular trends.

Final Thoughts

Based on the information above, VICI seems to be a solid option for those who want exposure to the REIT market through a differentiated but reliable player with growth prospects. Once again, I’d like to point out that although its investments are looking good in the short term, it is necessary to monitor the issuance of capital in relation to the investments made, checking that yields remain at attractive levels, since this segment is less obvious, with strong regulation, making it a barrier to entry, but also adding a degree of complexity to expansion and projections.

Read the full article here