With the Q1 earnings season out of the way for the Gold Miners Index (GDX) where we saw an average realized gold price of $2,070/oz, all eyes are now on the upcoming Q2 results. Given that the average realized gold price is sitting above $2,300/oz quarter-to-date, Q2 will bring with it much stronger financial results on balance, and one producer set to benefit is Victoria Gold (OTCPK:VITFF). This is because the company had a weaker than planned Q1 operationally, but should see increased production at higher margins as the year progresses. In this update, we’ll dig into the Q1 results, the Q2 margin outlook, and whether the stock is worthy of a spot in one’s portfolio.

Eagle Mine Gold Pour – Company Website

All figures are in United States Dollars unless otherwise stated with a C$ in front of the dollar figure. G/T refers to grams per tonne of gold. AISC refers to all-in sustaining costs.

Victoria Gold Q1 Production & Sales

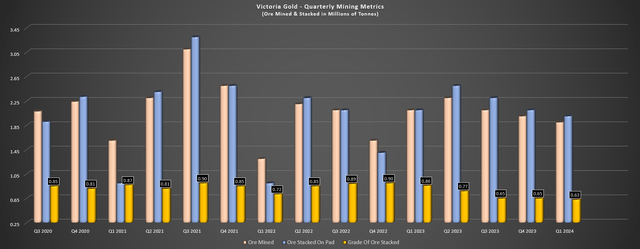

Victoria Gold (“Victoria”) released its Q1 results last month, reporting quarterly production of ~29,600 ounces of gold, a 21% decline from the year-ago period. The lower production was related to lower grades and lower than planned stacking rates, with ~2.0 million tonnes stacked at 0.63 G/T of gold (Q1 2023: ~2.1 million tonnes at 0.86 G/T of gold). Victoria noted that fewer tonnes resulted from reduced mobile equipment availability related to “slower than expected delivery of OEM parts to maintain drill rigs.” The fewer tonnes mined and stacked weren’t helped by mining headed into lower grade zones related to the mining sequence, with the double impact of lower throughput and sharply lower grades. On a positive note, the company has confirmed that the issue has since resolved and “mining tonnes have increased significantly.”

Victoria Gold Quarterly Mining Metrics – Company Filings, Author’s Chart

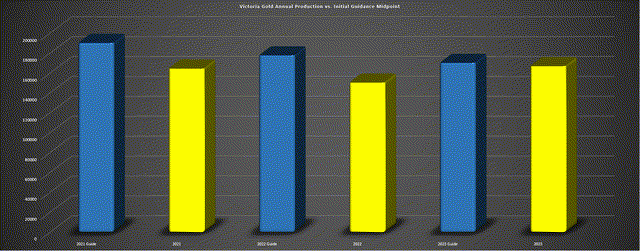

Victoria Gold Actual Annual Production (Yellow) vs. Guidance Midpoint (Blue) – Company Filings, Author’s Chart

The lower production year-over-year and tough start to 2024 has understandably discouraged some investors, with production tracking at just ~16.9% of annual guidance, requiring significant catch-up to deliver into guidance. Anxiety related to the ability to deliver at/above its guidance midpoint isn’t misplaced, with Victoria missing its guidance midpoint for three consecutive even if last year’s miss was largely related to wildfire impacts. And while I’m less confident in its ability to hit the 175,000-ounce mark (guidance midpoint) this year after the underwhelming Q1 performance, it’s important to note that the results aren’t that out of line with past Q1 results.

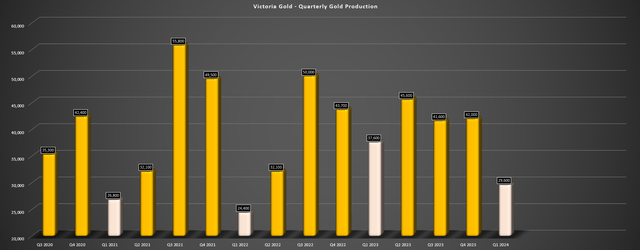

Victoria Gold Quarterly Gold Production – Company Filings, Author’s Chart

As shown in the chart above (beige bars represent Q1 vs. gold bars for all other quarters), production is always weakest in Q1, with Q2/Q3 being significant catch-up quarters, as Victoria’s management detailed below. So, although I’m less optimistic about Victoria producing 175,000 ounces, I am quite confident in the ability to deliver into the low end of its 165,000 to 185,000 ounce guidance this year. Given the higher realized gold price and despite what will likely be higher all-in sustaining costs year-over-year ($1,580/oz plus vs. $1,488/oz in 2023), Victoria should still be able to generate over $35 million in free cash flow this year using conservative gold price assumptions.

In summary, I don’t see any reason to panic about the weak Q1 results, but the company certainly has its work cut out for it to deliver a beat on its guidance midpoint, and I was hoping this might finally be the year to help restore some confidence in management’s operational execution.

“From a production standpoint, it’s fair to say that Q1 and Q4 are a bit tougher challenges for production. You get colder temperatures, you get snow. Q2 and Q3 are certainly the quarters where we can maximize area under leach, take opportunities, side slope leaching, and do a few other things that allow us to get a lot more tonnes to the pad, typically, and bring ounces forward.”

– Victoria Gold, Q4 2023 Conference Call

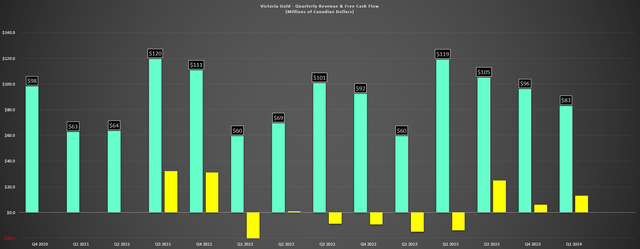

As for Victoria’s financial results, revenue sunk to C$83 million in Q1 2024, down from C$97 million in the year-ago period. This was related to fewer ounces of gold sold (~30,500 ounces vs. ~38,200 ounces), offset by a higher average gold price of $2,019/oz. And while the dip in revenue was disappointing and revenue will be impacted by hedges this year (~30,000 gold forward contracts at $2,116/oz), cash flow came in at a respectable C$30.0 million, while free cash flow came in at C$13.4 million, with Victoria paying down $8.3 million in debt and ending the quarter with just shy of C$29 million in cash and cash equivalents. As of the end of Q1 2024, net debt stood at ~$150 million, and its share count was slightly higher year-over-year with ~1.1 million shares sold at ~US$6.30 in a flow-through financing.

Victoria Gold Quarterly Revenue & Free Cash Flow – Company Filings, Author’s Chart

Costs & Margins

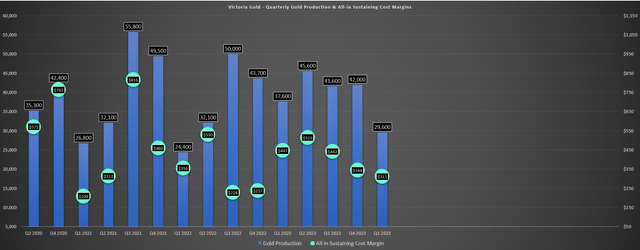

Moving over to costs and margins, Victoria reported all-in sustaining costs of US$1,708/oz in Q1, a significant step-up from $1,420/oz in the year-ago period. The higher costs were despite lower sustaining capital and affected by fewer ounces sold and continued inflationary pressures. This shouldn’t be surprising given that Victoria shared in its Q4 2023 results that while costs appeared to be leveling off for the group, it was still struggling with inflation, with this primarily related to labor costs, offsetting any benefit from lower fuel prices. The good news is that since Q1 we’ve seen a weaker Canadian Dollar and lower oil prices, as well as higher gold prices. So, while AISC margins dipped to $311/oz (Q1 2023: $447/oz) in Q1, we should see a material improvement sequentially with the benefit of:

1. higher gold prices, averaging over $2,300/oz quarter-to-date

2. a weaker Canadian Dollar

3. slightly lower fuel prices

Victoria Gold Quarterly Production & AISC Margins – Company Filings, Author’s Chart Gold/Oil Ratio – StockCharts.com

“As with many other operators, despite inflation having peaked, we continue to see cost inflation at Eagle. I would say the stickiest costs are, you could guess, it is labor. Labor is our largest cost, and it’s very sticky. And when inflation went up, labor needed to go up with it. Unfortunately, when inflation falls, labor does not fall back down.“

– Victoria Gold, Q4 2023 Conference Call

“The decrease in cost of goods sold is attributed to lower gold oz sold, partially offset by higher costs due to inflation.“

– Victoria Gold, Q1 2024 Results

So, what’s in store for Q2 2024?

Even if we assume an average realized price of just $2,270/oz and improved AISC of $1,610/oz, Victoria’s AISC margins would improve from $311/oz in Q1 2023 to $660/oz in Q2 2024. On a year-over-year basis, this would translate to a ~29% improvement vs. $515/oz AISC margins in Q2 2023. Hence, Victoria will have a much better quarter of free cash flow generation on deck, with it noting that the #1 priority for excess free cash flow is tackling its debt on its revolving credit facility, after the full repayment of its term loan in the next two quarters.

Valuation

Based on ~69 million fully diluted shares and a share price of US$5.65, Victoria trades at a market cap of ~$390 million and enterprise value of ~$540 million. This leaves the company trading at ~0.50x P/NAV vs. an estimated net asset value of ~$780 million, a very reasonable multiple even for a higher-cost single-asset producer that’s struggled to deliver on its production targets the past three years. However, it’s important to note that while 2024 is an average year for the Eagle Mine in the Yukon, 2025 is expected to be a phenomenal year. In addition, while AISC are likely to come in above $1,550/oz this year and over 10% above the industry average, life-of-mine AISC are expected to come in below $1,400/oz even adjusting for inflationary pressures and below $1,200/oz next year. Hence, although Victoria is undoubtedly penalized as a high-cost single-asset producer today, we should see a much better year ahead in 2025.

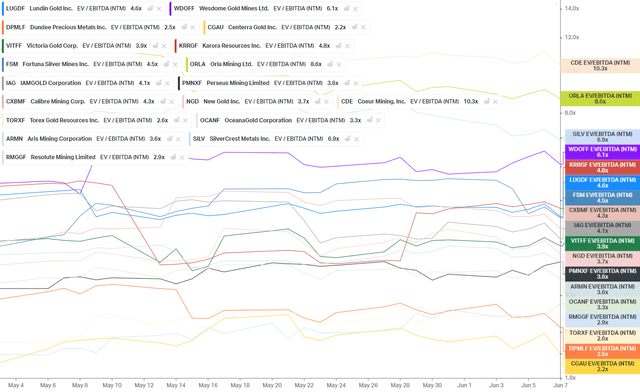

Forward EV/EBITDA Multiples – Junior & Mid-Tier Gold Producers – Company Filings, Author’s Chart

So, what’s a fair value for the stock?

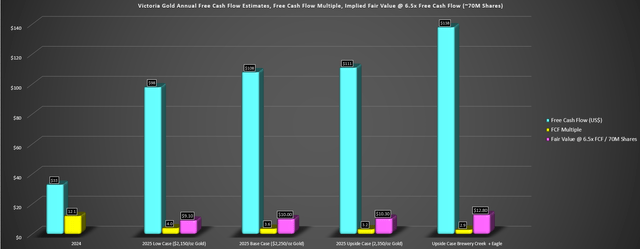

Using what I believe to be conservative multiples of 0.90x P/NAV and 5.0x P/CF (2024/2025 average estimates) and a 65/35 weighting to P/NAV vs. 2024/2025 average P/CF, I see a fair value for the stock of US$9.50. This points to a 68% upside to fair value, making Victoria significantly undervalued at current levels. Looking at gold price sensitivity charts below with free cash flow estimates for FY2025, this fair value estimate implies that the stock only trades at ~6x free cash flow in FY2025 which I would argue is a very conservative multiple for a Tier-1 jurisdiction producer. And if Victoria were to trade on purely a free cash flow standpoint, its fair value would increase to US$10.00 to its 18-month target price, pointing to nearly 90% upside from current levels ($2,250/oz gold price assumption).

Victoria Gold Annual Free Cash Flow Estimates, Free Cash Flow Multiple, Implied Fair Value @ 6.5x FCF Estimates – Company Filings, Author’s Chart & Estimates

Looking out longer term, Victoria has an additional upside to its current production profile if it brings either Raven or Brewery Creek online, and I have assumed that Brewery Creek comes online first as this requires significantly less capex. Using these assumptions and the same $2,250/oz gold price assumption (~240,000 ounces per annum from Eagle + Brewery Creek), Victoria’s fair value would increase to US$12.80 with the company capable of generating closer to $140 million in free cash flow per annum.

Hence, whether one looks at solely the 2025 numbers using relatively conservative gold price assumptions ($2,250/oz) or longer-term potential with a second online and the benefit of a slightly higher multiple (two mines vs. one), Victoria makes for a very interesting buy-the-dip candidate with a very reasonable valuation, especially if it can start delivering on guidance and see an uplift in sentiment which would contribute to a more favorable trading multiple. For now, Victoria remains above its ideal buy zone, but I would expect any sharp pullbacks from here to present a buying opportunity.

Summary

Victoria Gold had a tough Q1 with production coming in below planned levels, made worse by the fact that this is already the seasonally weakest part of the year. However, I remain confident that Victoria can deliver into its guidance of 165,000 to 185,000 ounces (albeit the midpoint could be tough to hit), and while the stock isn’t cheap on 2024 numbers, its free cash flow multiple drops from ~12 to ~4 with a much stronger year on deck in 2025. So, for investors looking to bet on a Tier-1 jurisdiction turnaround story with a very reasonable valuation, suggesting any sharp pullbacks from here should present a buying opportunity.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here