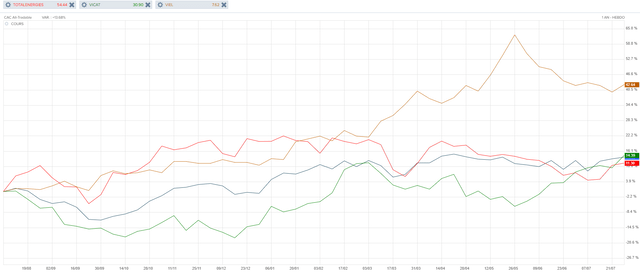

After recently reviewing the performance of three German stocks I bought in 2022, let us now take a look at a trio of French stocks which I recommended last year (see the initial article: 3 French Dividend Stocks I Am Buying: TotalEnergies, Vicat, VIEL).

This selection was based on the dividend yields offered by the three companies, and what I perceived as attractive valuations. I was not disappointed, as the stocks delivered well-covered dividends of 5% to 7%, and share price appreciation of 23% on average. In detail, the capital gains were driven by VIEL (VIL.PA), whose stock rose by 42% in a year, while TotalEnergies (TTE.PA, TTE) and Vicat (VCT.PA, OTCPK:SDCVF) posted gains of 11% and 14% respectively, in line with the broader French market.

Boursorama.com

Note: the chart above relates to the primary listing of these companies, Euronext Paris (tickers TTE.PA, VCT.PA, VIL.PA). Prices are in EUR.

Looking ahead, I remain bullish on these names, as their operational performance supports the continuation of their dividend policy, with potential for further share price appreciation as well. In fact, I have no plans to sell a single share for the foreseeable future.

TotalEnergies: Right Balance Between Dividends And Investments

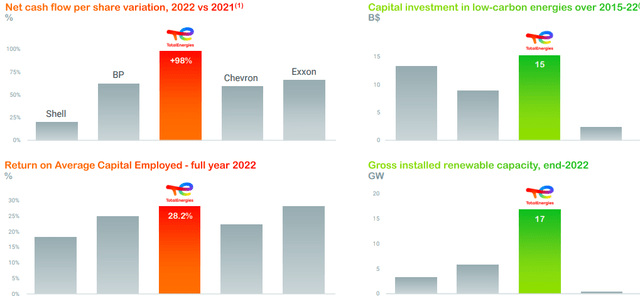

2022 was obviously a highly successful year for energy companies, and TotalEnergies was no exception. The oil major capitalized on elevated prices to reward shareholders (including a special dividend in December 2022 and buybacks) and pursue its strategy focused on long-term investments in low-carbon energies – which includes natural gas and renewables.

TotalEnergies’ Corporate Presentation

TotalEnergies keeps growing its electricity distribution segment as well, which makes me optimistic that the company will still be an energy leader in a post-oil world a few decades down the road. Meanwhile, it continues to enjoy the high returns offered by oil & gas, with H1 ’23 results remaining strong – though not as much as last year due to lower energy prices.

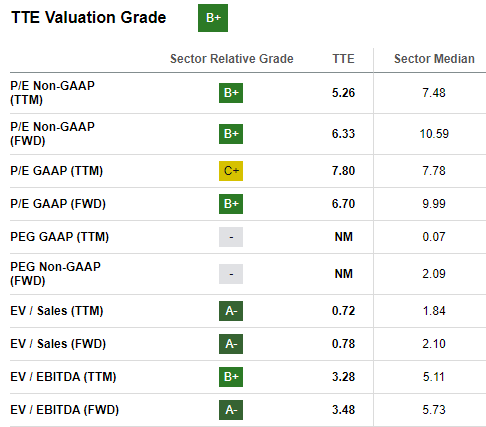

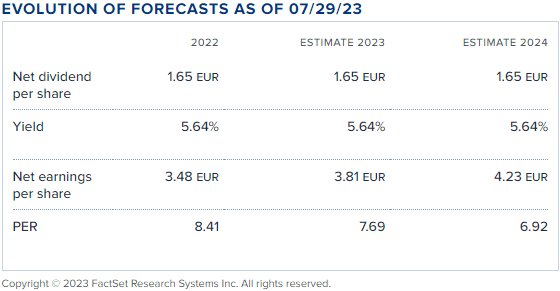

When it comes to valuation, the stock continues to look cheap as the sector remains unpopular. There is no guarantee of multiple expansion going forward, but given the underlying performance, the earnings yield and distributions are good enough to remain invested.

SeekingAlpha’s Valuation Grade and Underlying Metrics for TotalEnergies

Vicat: Still Unfashionable, But Performance Is Rock-Solid

It’s hard to find sectors that are even more frowned upon than oil & gas these days, but our second name, Vicat, might fit the bill: cement producers tend to have a high carbon footprint. They are, however, indispensable, not least in emerging markets where some of Vicat’s operations are located: India, Brazil, Egypt, Turkey, West Africa, Kazakhstan. What’s more, Vicat has done a good job developing less energy-intensive cement and concrete.

The financial results of the French company continue to be strong, on the back of successful years in 2021 and 2022. The recently-released H1 ’23 results confirmed that Vicat was able to pass on cost inflation to its customers, protecting its EBITDA level.

Vicat’s H1 ’23 results presentation

The new kiln at the Ragland, Alabama plant has also started to ramp up production, as the Americas segment (US+Brazil) catches up with the legacy markets in France, Italy and Switzerland in terms of EBITDA contribution.

In terms of valuation, Vicat remains cheap, with an estimated P/E ratio of less than 8 for 2023. Again, there’s no assurance that the stock will rerate, but investors are getting good value here, and a comfortable 5%+ dividend yield.

Boursorama.com

VIEL: Firing On All Cylinders, Still Reasonably Priced

The small cap financial stock Viel & Cie has been the standout performer among this trio. I’ve been adding to this position over the past 12 months, as I really like the diversification this company brings to the portfolio. For a more complete presentation of Viel, please see my prior articles such as this one.

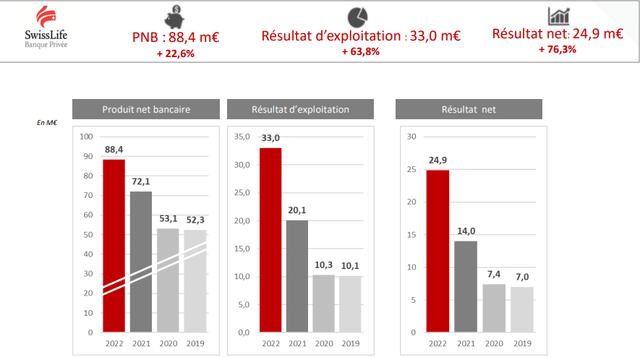

Let’s just mention here that all holdings of Viel & Cie exceeded expectations in 2022, whether it be Tradition (OTCPK:CFNCF), the Swiss interdealer broker which is Viel’s main asset, or the retail broker Bourse Direct (BSD.PA). The icing on the cake was brought by SwissLife Banque Privée (40% held by Viel) which I am highlighting here as it moved from a side business to a bona fide contributor to Viel’s results:

Viel & Cie’s Annual General Meeting presentation

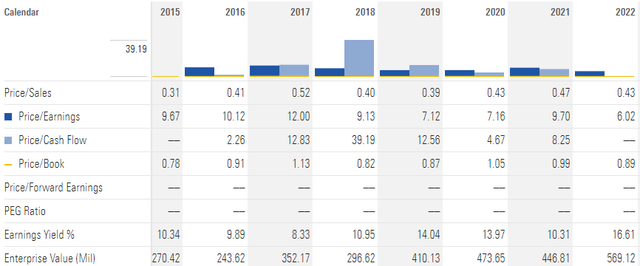

The great news is that Viel is set for even better performance in 2023. While subdued volatility could be a headwind for Tradition, this should be more than offset by the favorable impact of rising interest rates. Not only Tradition, but also Bourse Directe and possibly SwissLife Banque Privée will benefit from higher rates. With this in mind, the shares remain reasonably priced despite the 40%+ advance, with a trailing P/E ratio of 6 (and a forward P/E in the same region, in my opinion).

Morningstar.com

The dividend has been rising steadily in recent years, and I wouldn’t be surprised to see the next annual payout raised to €0.40 per share (from €0.35 in 2022), equating to a 5.3% yield at the current share price of €7.6 on the Euronext Paris exchange. Not bad for a stock that tends to provide some downside protection when markets get volatile.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here