Viking Holdings Ltd (NYSE:VIK) is a cruise and passenger shipping company that had a recent IPO. The company operates in two segments called River and Oceans, operating a total of 92 ships, of which 81 were river vessels and 9 were ocean vessels. It operates in the US, Europe, and international markets.

One thing that sets this company apart from other cruise companies is that it operates smaller ships and its cruises tend to be more of a cultural and learning experience for a different group of people who are looking for a calmer cruise experience. Typically, larger cruise companies like Carnival (CCL), Royal Caribbean Cruises (RCL), and Disney (DIS) are known to have these cruises that are very much like having a constant party and exposure to constant stimulation like loud music, light shows, colors blasting and while some people like that kind of entertainment, others prefer something calmer and more quiet, so Viking offers an alternative for these types of people who would rather have a relaxing experience than partying experience. The company’s cruises also offer a lot of educational experiences, cultural learnings, and seminars offered by experts in different fields where people can gain exposure to their favorite topics of curiosity.

River Cruise Ships (Viking Holdings)

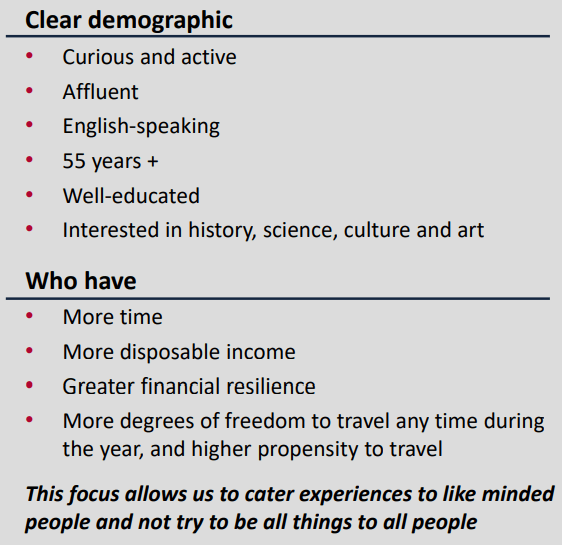

Because it offers a different type of experience that includes a more relaxed environment, the company’s target audience also shares a more or less common demographic. These people tend to be 55 years or older, more affluent than average, well-educated with a strong interest in history, science, culture, and art, and more likely to be retired so they have more time and more disposable income. Many of the customers of the company are repeat customers who do their cruises year after year.

Target Demographics (Viking Holdings)

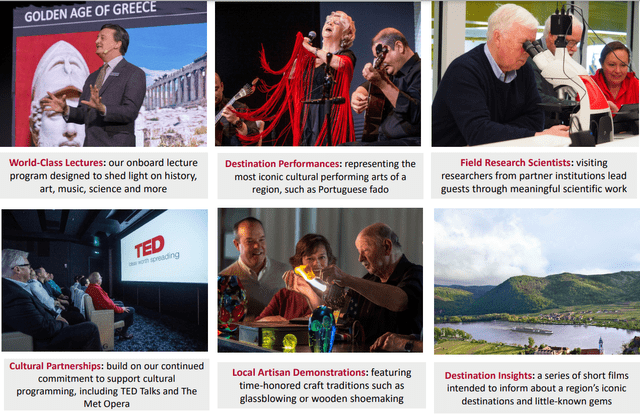

Some of the unique experiences offered by this company to its customers include lectures focusing on art, science or history, artistic performances, applied research demonstrations, live TED speeches, artisan demonstrations, and destination explorations. Many of the destinations covered by these cruises tend to be places of high cultural importance as well as beautiful scenery where people can explore those areas.

Variety of Experiences Offered (Viking Holdings)

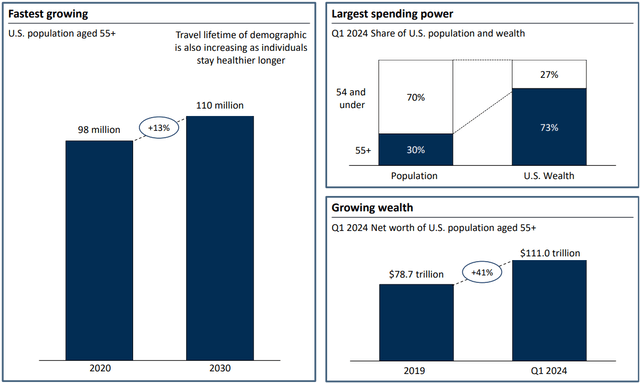

The company’s target audience of people aged 55+ also happens to be the fastest-growing population segment in the US, and they tend to have the highest spending power and more wealth than any other age group. This is likely because they have been around for longer and had more experience and opportunities to amass wealth over the years. Think of it like this, if you started investing into your 401k when you were in your 20s or early 30s, by the time you are 55 years or older, you will have had a significant amount of growth in your portfolio due to 20-30 years of compounding which will allow you to have a more comfortable life. Currently, 55+ year old demographic makes up only 30% of the US population, but they hold 73% of all wealth and their net worth collectively rose from $79 trillion to $111 trillion in the last 5 years. Of course, part of this was because the average 55+ year-old got wealthier, but that’s not the only reason. Another reason is that more people entered into this demographic group in the last 5 years, which means the collective wealth of this group rose by having more people in it. In the next 5-10 years, we can expect these numbers to grow even further as more people enter in this age group and older people are expected to live longer due to advances in medicine.

Financials of 55+ Demographics (Viking Holdings)

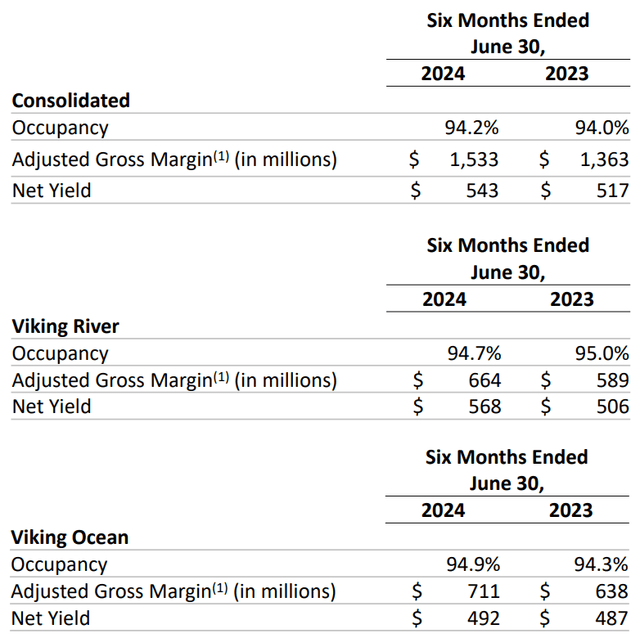

In the first 6 months of 2024, the company’s cruises had an occupancy rate of 94.2% up from 94.0% from the previous year. River cruises actually saw occupancy drop a bit from 95.0% to 94.7% but ocean cruises made up for it. Even though occupancy rates rose only slightly, gross margins and net yield (profits) were up significantly, indicating that the company was able to charge its customers higher prices and people were fine with it. Total adjusted gross profits rose from $1.36 billion to $1.53 billion, an increase of 12%, and operating profit (net yield) was up from $517 million to $543 million, which is an increase of 5%. Operating income in the river cruises segment rose by more than 10% (up from $506 million to $568 million) but the same metric was flattish for the ocean segment (up slightly from $487 million to $492 million) indicating that there might be more pricing power in river segment than the ocean segment. Notice that occupancy in the river segment dropped slightly but resulted in bigger profits, while occupancy in the ocean segment rose slightly but resulted in flattish profits.

Financials by Segment (Viking Holdings)

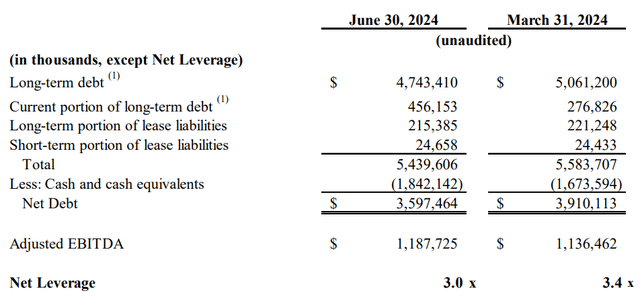

As with most cruise companies, this company has a lot of debt. After all, it costs a lot of money to build big cruise ships, and it can take many years for a newly built ship to recuperate all its costs. Since the company had a recent IPO it has a cash position of $1.84 billion, but its debt position is about $5.44 billion, which gives it a net debt position of $3.60 billion. Considering that the company has an adjusted annual EBITDA of $1.19 billion, it would take the company 3 years to pay off this debt, thus giving it a net leverage ratio of 3.0x. This is somewhat down from last quarter’s leverage ratio of 3.4x. While this doesn’t look too bad, keep in mind that the company has spent $460 million in the last 12 months on debt servicing (interest payments alone), which means its debt servicing can eat into a big chunk of its profits. Then again, this is very common in the cruise industry, which is known to be very capital intensive both in terms of building new ships as well as running ships on a day-to-day basis from an operations perspective. This aspect of the business is unlikely to ever go away anytime soon, if ever.

Debt Situation (Viking Holdings)

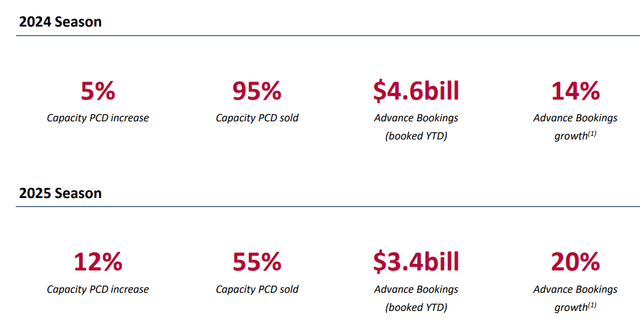

The company’s forward guidance calls for a lot of growth in the next year or so. For the year 2024, it already sold 95% of all capacity as well as selling 55% of capacity for the 2025 season. By the end of this year, the company expects to have 14% growth in advance bookings, followed by another 20% growth in 2025. Keep in mind that the company expects a capacity growth of 12% for 2025 as new ships will be delivered, and it will have more cruises to sell, but even with this, the company expects to fill this capacity almost entirely by next year.

Forward Guidance (Viking Holdings)

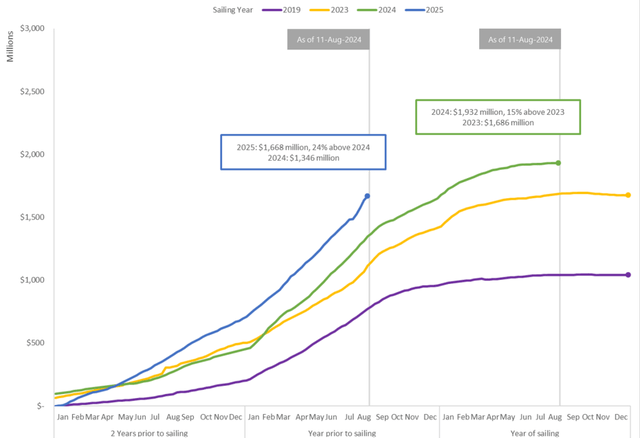

As a matter of fact, current trends of advanced bookings are already well ahead of any year since 2019. If this trend continues, 2025 will be the highest year ever in the history of the company both in terms of capacity offered, capacity sold, and total revenues. Since the company is increasing its capacity by 12% and expecting a 20% growth in total bookings, we can surmise that it is in the process of raising prices by about 8% between now and next year, but this doesn’t seem to be slowing people down from booking cruises from this company.

Forward Booking Progress (Viking Holdings)

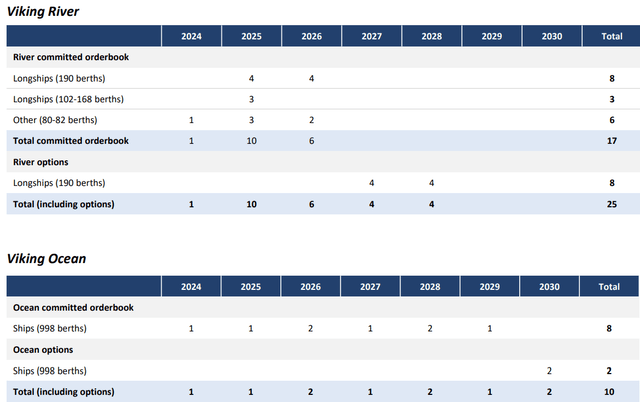

In the long term, the company will be ordering more ships as it sees more opportunities for growth. Between now and 2030, the company expects to add 25 river cruise ships and 10 ocean cruise ships for a total of 35 new ships. The company already ordered and is on track to receive 10 new river ships next year, which is where that 12% capacity growth I mentioned above will come from. It is also on track to add 1-2 new ocean ships every year to its fleet between now and 2030. On one side, this must be positive since the company is expecting to see a lot of growth in the future and making these investments but on the other hand, this will likely to increase the company’s debt level and leverage ratio significantly in the coming years unless these ships can quickly turn profits. The company is basically betting that the trends it’s been seeing in the last few years will continue for the next 10 years, but it’s difficult to tell whether the exceptional economic growth we’ve seen in recent years can continue on like that without any speed bumps.

New Ship Orders (Viking Holdings)

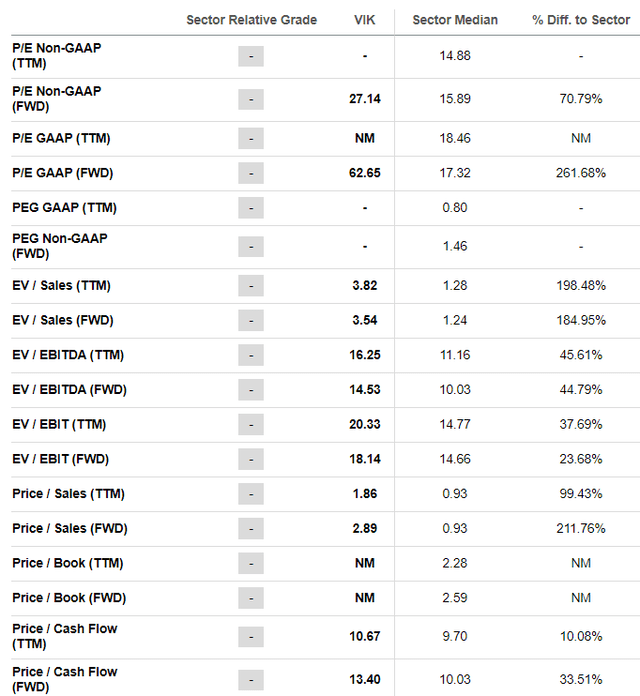

We are looking at an interesting company that’s been seeing a lot of growth recently, but its valuation is definitely not cheap. The company has a non-GAAP trailing P/E of 27 and a forward P/E of 63, but this is mostly due to how it books its profits. For example, last year the company reported a big loss because of a $2.4 billion charge on “Private Placement Derivative Loss” which is not part of the company’s operations and was a strategic loss-taking for tax purposes. When we look at the company’s EV/EBITDA, we are seeing a more reasonable value of 16 for trailing and 14 for forward metric, but even this is significantly above the sector median of 11 and 10, respectively, for trailing and forward metrics. Another relevant metric for the company is price to cash flow, which is 13 (forward basis) and while it’s not too bad for a company growing in double digits, it’s still above the sector median of 10.

Valuation (Seeking Alpha)

Moving forward, the company seems to expect a lot of growth, and it’s ordering a large number of ships to be delivered in the next 5-6 years but at the end of the day, this company operates in a highly cyclical industry, and considered discretionary spending the global economy is already showing signs of slowing down in the next year or two. If we were to see a global recession, the company might see a lot of cancellations, and its operations might suffer significantly, especially considering its heavy debt load. If the company’s valuation was a bit cheaper it could offer a larger margin of safety for investors, but its current margin of safety is probably limited as it trades at a premium against its peers even though it trades at a cheap valuation compared to the overall market (considering S&P 500 currently trades at a P/E of 28).

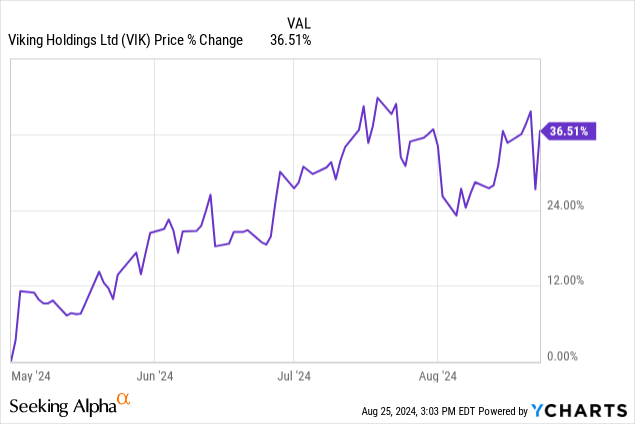

This is an interesting company which I will be watching closely. The stock is already up 36% since its recent IPO, which shows that investors are highly optimistic about it and there is a lot of hope built into its current price. The company has a unique premise and interesting approach to the cruising business, and it serves a niche market of people who seem to have a lot of money and free time but don’t want the “noisy” cruise experience offered by other companies. I might consider buying some shares if there is a pullback or shares get cheaper, but at the current valuation, I am just going to keep it on my watchlist and see where it goes.

Read the full article here