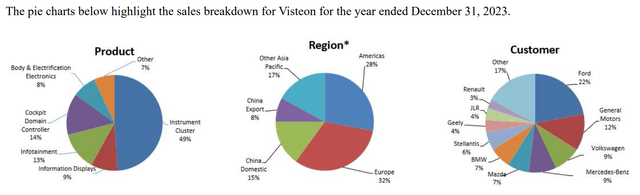

Visteon Corporation (NASDAQ:VC) is a June 2000 spin-off from Ford (F). This U.S. automaker remains its largest customer, accounting for 22% of 2023 sales. However, the company now serves the whole auto/truck industry, mostly manufacturing the display video/panels on your dashboard and various instruments/devices/inventions for measuring and controlling onboard electronics. It is now becoming an important supplier of displays and electronics for accelerating growth at a host of electric vehicle OEMs, with new wins and business coming in this area of the market over the next several years.

Visteon, 2023 10-K Filing

The good news for investors is the valuation is low, growth expectations are ratcheting higher, and the balance sheet is clean/conservative. For a bonus, the push for autonomous driving capabilities and AI connectivity in cars could prove the catalysts for oversized share performance by owners of the business.

Let’s go through the bullish setup, potentially supporting a powerful rebound in the stock price into 2025-26.

Visteon Homepage – July 15th, 2024 Visteon – Q1 2024 Earnings Presentation Visteon – Q1 2024 Earnings Presentation Visteon – Q1 2024 Earnings Presentation

Undervaluation Argument

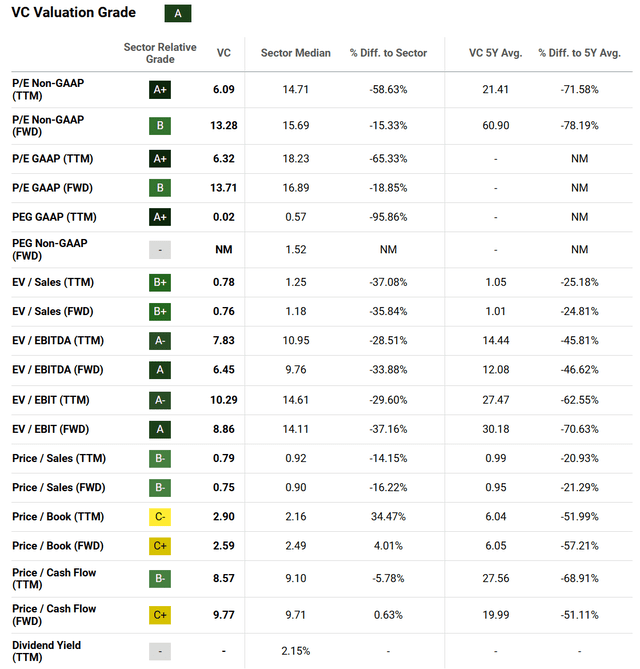

Including the one-time tax gain reported in late 2023, Seeking Alpha’s computer ranking system puts a Quant Valuation Grade of “A” on Visteon shares today. This comparison tool reviews each company’s worth vs. a 5-year history window, plus current fundamental analysis ratios vs. prevailing numbers in industry peers/competitors.

Excluding Visteon’s accounting change, I am estimating the valuation score would still be in the high “B” range compared to the auto parts supply industry, or leading electronics/computer manufacturing names.

Seeking Alpha Table – Visteon, Quant Valuation Grade, July 15th, 2024

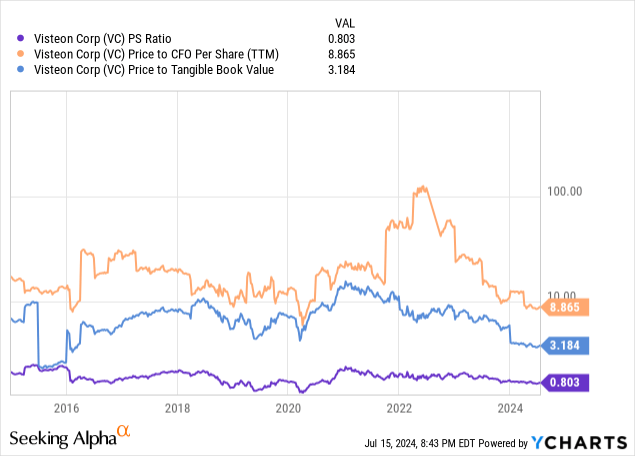

Operating valuation statistics have drifted to the lower end of VC’s 10-year trading history. Below you can review how price to trailing sales (0.8x), cash flow (8.9x), and tangible book value (3.2x) compare to recent trends. I figure shares are trading at a rough 30% discount to long-term averages, using the three data points.

YCharts – Visteon, Basic Fundamental Ratio Valuations, 10 Years

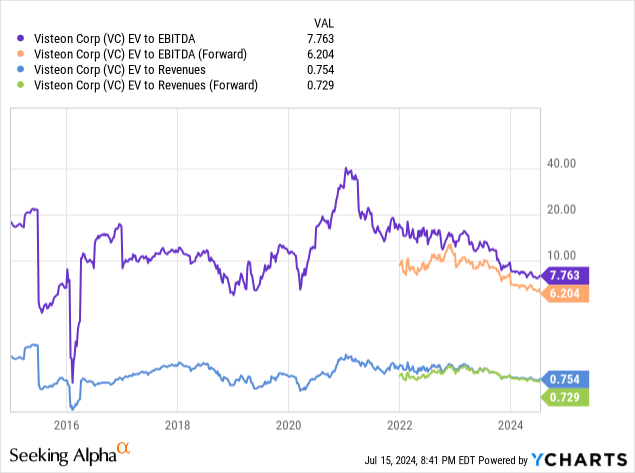

When we include $504 million in cash vs. $332 in total financial debt, the net enterprise valuation is equally compelling as a value play. EV to forward estimated EBITDA (6.2x) is approaching its lowest level since 2016, and stands at a good 50% discount to its 10-year average. EV to sales of 0.75x is trading at a 30% discount to decade-typical numbers.

YCharts – Visteon, Basic Enterprise Valuations, 10 Years

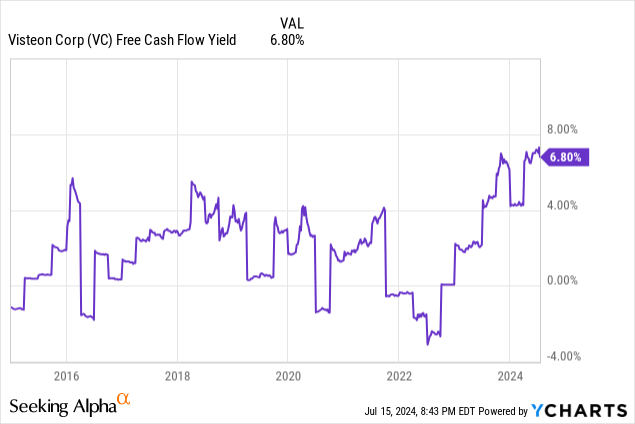

Perhaps the most bullish valuation idea is free cash flow generation has been superb over the last year (excluding the one-time accounting gain). With a sliding share price helping out, the trailing free cash flow yield of 6.8% is essentially a 10-year-high. And, free cash flow yield could actually improve dramatically in the years ahead, if analyst estimates for earnings growth are hit and CAPEX dollars are held in check by management. In other words, management could have the flexibility to increase its share buyback and/or start a cash dividend, without slowing its growth path.

YCharts – Visteon, Free Cash Flow Yield, 10 Years

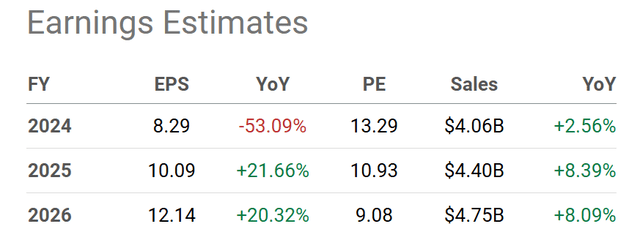

Below is the present Wall Street analyst forecast for cash EPS and sales growth at Visteon between 2024-26. The forward income estimates are quite exceptional vs. anemic growth in the past at VC. For valuation purposes, a P/E below 10x operating results would be the lowest since 2019, just before the share price bottomed at $44 per share.

Seeking Alpha Table – Visteon, Analyst Estimates for 2024-26, Made July 14th, 2024

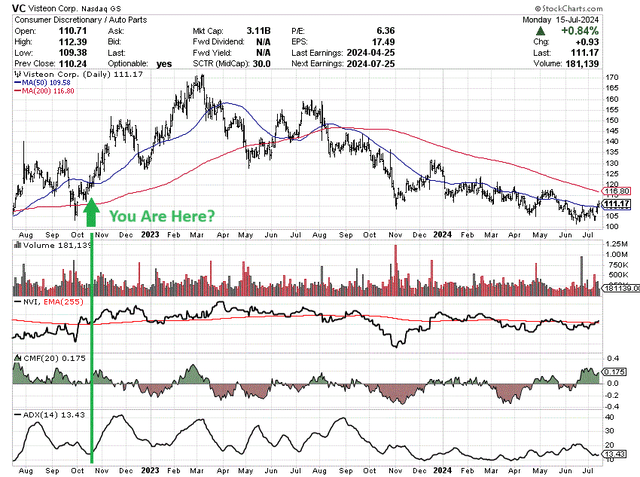

Technical Chart Improving

Supporting a turnaround in the stock, and my outlook for a nice rebound in price, technical trading clues are pointing to better days ahead. In particular, we appear to be in a positive trading setup similar to October 2022. Below I am highlighting the convergence of four indicators, which hasn’t happened in 20 months.

Namely, a stock quote crossing above the 50-day moving average, alongside an improvement in the Negative Volume Index, a very positive 20-day Chaikin Money Flow reading, and a low-volatility 14-day Average Directional Index score, together suggest a period of price advance could be approaching.

My view is today’s trading backdrop could be the healthiest in quite some time, with some sort of bullish up-move now well overdue (following roughly a year of steady decline).

StockCharts.com – Visteon, 24 Months of Daily Price & Volume Changes, Author Reference Point

Final Thoughts

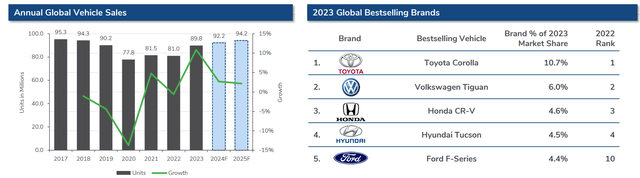

Overall, Visteon should be one of the main beneficiaries of the trend toward turning car/truck cabins into traveling computer centers. And, with total car sales on the planet trending upward again from the 2020 pandemic bottom, I believe VC shares are worthy of serious consideration in portfolio construction.

Kroll.com – Auto Market Research, Spring 2024 Update

Of course, the biggest investment risk owning Visteon would come with a deep economic recession. However, the sliding stock price from $172 in March 2023 seems to have already discounted a soft landing to mild/temporary economic slowdown. If we can avoid a severe contraction in GDP output and auto demand later this year and 2025, I am confident VC will trend much higher in price on improving sales, income, cash flow results.

For price targets, I am modeling worst-case risk estimates down to $75, given a company-wide sales decline of 5% to 10%. Such would mark the largest sales drop (asset adjusted) since 2012. $75 for price would equal an investment loss of -35%, while putting price to depressed sales and book value closer to 10-year lows.

On the potential reward side of the equation, 16x cash income and a normalized 1.1x sales would bring a share price of $175, using analyst estimates, by the end of 2025 or early 2026 (18 months out). Yet, if aggressive share buybacks reduce outstanding shares by 10%, AND business results beat current estimates, a premium valuation could support prices materially above $200. So, I am estimating a potential upside of +55% to +70% for bullish targets.

While the upside is not spectacular, those searching for steady +15% to +20% annualized returns over the next few years (during an overvalued Wall Street market situation), might want to weigh the pros and cons of Visteon. I rate shares a Buy under $115, and own a small position.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Read the full article here