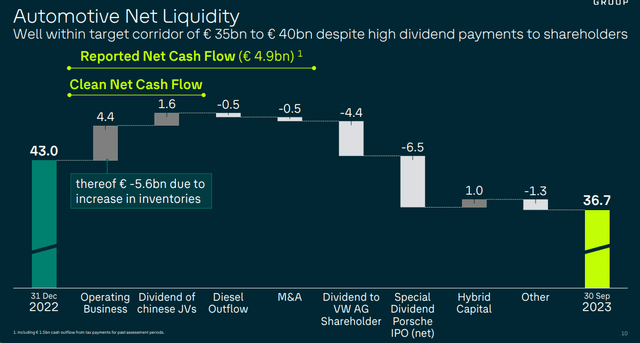

From time to time, we need to be patient and take advantage of the equity market opportunities. Last year, we reported our bullish view on Enel, while this year, our internal team believes Volkswagen (OTCPK:VWAGY, OTCPK:VLKAF, OTCPK:VWAPY) is set to outperform. This is not the first time we have covered what we see as ‘the Most Discounted Auto Stock;’ however, it is essential to recap that Volkswagen has a negative stub value. The company’s equity valuation is lower than P911 and Traton’s equity stakes (both companies are listed). This construct, coupled with a dividend yield of> 7.5%, is the clear market message. Another anomaly on the current €58 billion equity valuation is the reversal working capital requirement expected in 2024 coupled with the current automotive liquidity at €36.7 billion in Q3-end. As we can see from the Volkswagen net liquidity waterfall, the company was negatively impacted by higher inventories and by a one special dividend payment from the P911 IPO. We anticipate a positive trend at the Lab, raising our free cash flow estimates to €15 billion in 2024.

Volkswagen’s net liquidity

Source: Volkswagen Q3 results presentation

The last 1.5 years have been painful, from disappointing electric vehicle sales to losing China market leadership and no valuation upgrade from P911’s initial public offering. Looking back, we believe the Auto major has struggled to turn its size into scale and fully leverage its product portfolio. Attempts at centralizing expenses to reduce complexity have been expensive and resulted in cost duplication. Here at the Lab, we were positive on the P911 IPO; however, this has revealed the valuation drain from Volkswagen Group’s core underperformance. Therefore, even if we support a sum-of-the-part valuation, we believe additional IPOs (Lamborghini and Bentley) will unlikely create stakeholder value until the company’s core performance is fixed.

Why Volkswagen is a Top Pick?

- In November, the EU car market grew by 6.7%, marking the sixteenth consecutive month of expansion. However, after thirteen straight months of double-digit growth, this increase, according to the data communicated by ACEA, has been lower than expected with a single-digit number. Some markets have had substantial double-digit gains, including two of the largest: Italy (+16.2%) and France (+14%). In contrast, the German car market contracted, recording a decline of 5.7% compared to November 2022. EV share has remained stable at 14.2%, constantly exceeding diesel cars at 13.7%, while petrol cars maintained the leadership. In Germany, among other things, government incentives are now removed from December onwards, and sales of electric vehicles suffered a setback, with a drop of 22.5%. All major car manufacturers in the EU alone recorded a year-on-year increase except for Stellantis and Toyota. In November, compared to its home market, Volkswagen registered a positive performance of +11.4%, with deliveries at 231,743. Supported by our latest publication on VW, the US is also evaluating measures on Chinese electric car restrictions. According to the Wall Street Journal, the Biden administration is considering raising tariffs on Chinese electric cars to limit exports. The EV landscape in Europe is different than in the United States, where tariffs are already high enough to discourage competition from China, which exported nearly 48,000 EV cats to North America in October compared to more than 564,000 vehicles sent to Europe. With potential higher tariffs from China and lower incentives in the EU and the USA, traditional OEMs such as Volkswagen can sustain additional growth rates from combustible engines. Looking at the ACEA data, this cannot go unnoticed and will likely support Volkswagen in the EV transition;

- We are witnessing a management change in taking a more pragmatic approach to increase Volkswagen’s competitiveness in the upcoming years. In 2023, faced with slowing sales, Tesla sacrificed industry-leading margins and reduced the prices of its four models, with particular attention to China. Volkswagen is currently not able to compete on a gross margin level, and Thomas Schäfer, CEO of the Volkswagen Passenger Cars brand, decided to launch a business review “to start to bear fruit as early as 2024” explaining how “this is crucial if we are to withstand the increasingly tough competition in extremely challenging market conditions.” At the Lab, we believe Blume (Volkswagen CEO) has a solid track record of running P911 and will make difficult decisions, including headcount and cost reduction. The company’s competitiveness is at risk. Communication with the Workers’ Council appears open after years of tension under the Diess CEO. Governance is an additional critical risk, but there is a sense of urgency at the Group level, and the CEO is in a position of strength. We believe that low-hanging fruits can be achieved without compromise and the company recently announced a €10 billion savings program. This includes lower staff reductions with early retirement than layoffs, lower R&D expenses, and savings in SG&A costs. In addition, the CEO is raising the accountability of brands;

- This announcement, coupled with external partnership and cooperation. XPeng’s new investment was announced, and we believe that CARIAD software will likely follow with an option for a JV in the battery. This will end Volkswagen’s insularity that drove management decisions in the past two decades. In addition, the company should regain Wall Street confidence, and investor interest will require proof points. China CMD in April 2024 will likely be a positive catalyst. We maintain a soft-landing auto industry scenario as we believe a reversal trend of lower car sales should characterize 2024.

Conclusion and Valuation

Having said that, our internal team confirmed an operating profit of €24.9 billion in 2024 (from an expected €23.7 billion in 2023) and an FCF of €15 billion. With these numbers, we arrive at an earnings per share of €30. Given the workforce reduction, we believe Volkswagen won’t raise the dividend per share. Our downside protection is the company’s negative stub value with sustained free cash flow generation. We value VW with a P/E of 6.5x, confirming our buy rating target at €196 per share. Last year, we doubled the S&P 500 return with our Enel investment. This marked Mare Evidence Lab’s first article of the year, so let’s hope for the best in 2024 and thanks for your support.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here