It’s been a tough past month for the Gold Juniors Index (GDXJ) with the index suffering a near 15% correction. However, one name, Vox Royalty Corp. (NASDAQ:VOXR), has bucked this trend thus far and has added to its gains in June, likely stemming from its improving investment thesis and significant undervaluation vs. peers. In this update, we’ll dig into what makes the stock unique, why the company has a very bright future and a closer look at its undervaluation vs. peers and its royalty portfolio.

All figures are in United States Dollars unless otherwise noted with an A$ for Australian Dollars and based on a constant 0.65/1.00 AUD/USD exchange rate.

The Current Environment

We’ve seen a significant increase in entrants in the royalty/streaming space over the past five years, which made the space more competitive with more companies fighting for deals and ultimately driving returns on these deals lower. Fortunately, this hasn’t affected the big-3 royalty/streaming companies too much, as they are in a league of their own in terms of deal size. In addition, mid-tiers and the big-three obviously benefit from a lower cost of capital than their junior royalty peers, making it extremely hard for the junior royalty names to grow and often leading to the junior royalty companies stooping to lower IRR deals simply to achieve growth for growth’s sake.

Unfortunately, this means that while some of the junior royalty companies have decent growth and have built a path to the 20,000 gold-equivalent ounce [GEO] level longer-term as new assets come online, they’ve paid the price for these deals on a per-share basis. In addition, there’s no clear path to growing from 10,000 to 40,000-50,000 GEOs because they’re now competing with the majors that are bidding on smaller royalty assets as things get more competitive for bigger assets and the juniors can’t win bids unless they overpay because they lack:

- The brand name and “seal of approval” on their asset for the seller who comes from selling a royalty with the top-5 companies

- A much lower cost of capital

- The liquidity to make a run at $20+ million deals, which often means transacting on lower-quality assets with weaker operators and/or mostly development assets and getting the proverbial leftovers that the majors didn’t want

This makes for a bleak investment thesis for investing in most junior royalty companies if they are forced to grow through relatively low IRR and or lower-quality deals. However, Vox Royalty has separated itself from the pack and now owns the second-largest portfolio hard rock royalties in Australia. Before we get into what makes Vox Royalty unique, let’s address an important point on why royalty/streaming companies are a staple for an investor looking for precious metals exposure and tackle a misconception about their return potential.

Why Own Royalty Companies?

Some investors might be less enthused about owning a royalty company in what looks to be a new bull market for gold/silver, given that these companies offer much less torque or perceived torque relative to their producer and developer peers and are thought to be lower beta and safer “blue-chips” that will significantly lag in a bull market. However, there’s an important distinction worth making.

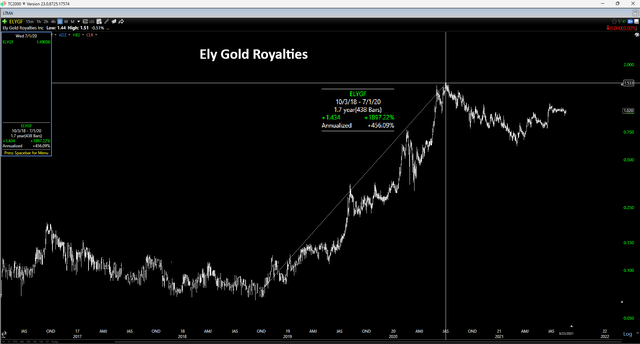

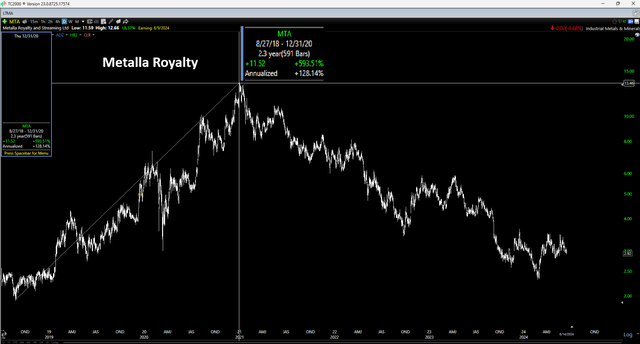

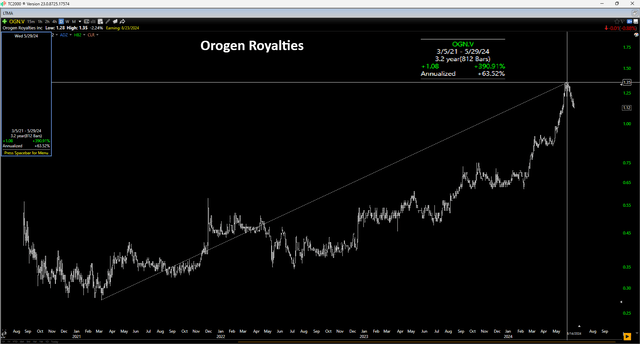

This is that while mid to large-scale royalty companies provide the least torque and don’t provide the same upside leverage from a share price performance standpoint as producers/developers, the junior royalty companies offer massive torque and have regularly enjoyed 200% – 600% moves off their lows and 50%+ annualized returns. Some examples are shown below, with Ely Gold Royalties returning over 1000% in less than five years and being one of the largest winners sector-wide in the past decade.

Ely Gold Royalties – TC2000.com Metalla Royalty & Streaming Chart – TC2000.com Orogen Royalties Chart – TC2000.com

However, unlike their producer/developer peers, these companies provide this leverage without the usual risks and negatives that include:

- exposure to inflation on operating costs/capital costs

- lack of diversification that magnifies any issues at an individual mine/project

- requirement to fund drilling, sustaining capital/growth capital and technical studies at mines/projects

- difficulty diversifying above 10 assets successfully, given that this can result in a lack of focus

- severe margin compression during cyclical downturns

And as for their superior attributes, there are several notable benefits to this model, including:

- the ability to scale materially without added technical risk or significant growth in G&A

- the ability to diversify by jurisdiction and by asset at multiples of the scale of even the largest producers

- upside to plant expansions and mine life extensions at none of the cost

- greater chances at benefiting from new discoveries with dozens of developers/operators drillings dozens of properties vs. a focus on 1–2 properties for juniors and 10–15 properties for majors

On the last point (#4), and given how rare major discoveries have become, I would much rather position myself with a shotgun approach (royalty model) vs. the sniper approach (developer/explorer model), especially given that royalty companies don’t spend a cent for this exploration yet have dozens more “at-bats.” These exponentially higher at-bats and chances for a home run come from the fact that a junior wakes up, turns on its rig[s] and drills its one or two highest priority prospects. A royalty company wakes up, focuses on business development uncovering deals that will fuel its next leg of growth, while simultaneously across the world, dozens of operators, developers and explorers turn on their drill rigs and drill out their deposits at zero cost to the royalty company on its royalty ground.

GFI Daily Chart – TC2000.com

Finally, and not discussed nearly enough is the fact that the share price movements in royalty companies are typically cleaner and one is less likely to get bucked off the trend without the major risks of capex blowouts, major resource model changes, permitting hiccups and the several other setbacks that come with owning a relatively concentrated developer/producer. This is critical because there’s nothing more frustrating than being right on a fundamental thesis but not making money because of being shaken out, and the average investor has a better chance at stomaching shallower corrections vs. major gap downs and up to 50% declines that are the norm with producers/developers even in bull markets.

The Business Model & Why Vox Royalty?

The name we’ll discuss today has a competitive advantage in the global royalty space, and this company is Vox Royalty. As one of the newer entrants to the space, Vox Royalty (“Vox”) has an interesting business model given that it got its start in 2019 through the acquisition of Mineral Royalties Online [MRO], a proprietary database of over 8,000 royalties. Importantly, this acquisition gives the company access to legacy royalties that have already been created, are flying under the radar, and ultimately allows it to avoid the competitive auction process of bidding on royalties/streams in an arena where the smaller company simply can’t compete, and they’re often only winning because the larger companies are walking away as there’s no value left at the going bid. Vox’s Chairman and CEO Kyle Floyd expands on this deal below:

“What differentiates us vs. every other royalty company in the world is that in 2019 we bought a database of mining royalties. So there was a company called Mineral Royalties Online and we were in the process of building our own database to understand where royalties were and who owned them to give us a leg up on the competition. MRO was a little further ahead than us, we ultimately bought this business in 2019 for $2.1 million, which at the time felt like the most expensive acquisition we’d ever done because we weren’t actually buying royalties, we were just buying the ability to find better value.

And since that point, the combination of that database and also the synergies of bringing like like-minded people that had the right skill sets, we’ve led the world in terms of third-party royalty acquisitions. And what matters most over that time period, we’ve created the most value per share”.

– Recent Presentation, Planet MicroCap.

Vox’s Competitive Advantage – Company Presentation

To summarize, Vox is not out there creating royalties on existing assets or bidding on royalties that most companies in the sector are already aware of, but often bidding for royalties from individuals or companies that may want to monetize these royalties or from companies in unrelated industries that may simply want to divest of royalties that are peripheral to their core business.

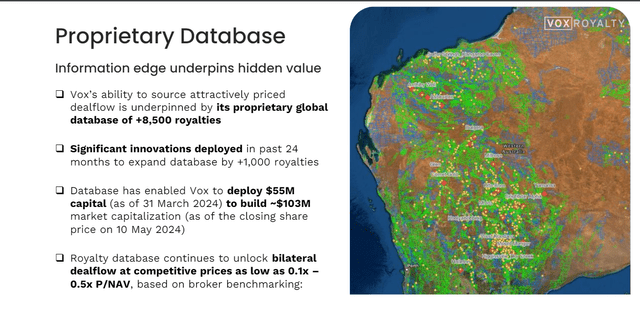

Proprietary Royalty Database

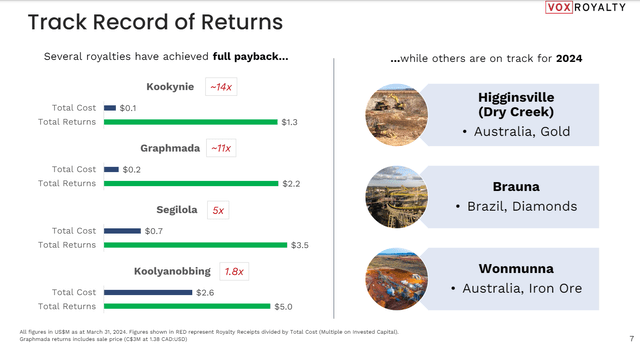

An example of one of their earlier deals highlights this opportunity, with Vox paying ~$2.6 million in 2020 to acquire an uncapped 2.0% FOB [free on board] royalty covering a portion of the Deception Pit at the Kooylanobbing Iron Ore Mine in Western Australia that is operated by MinRes [MIN.ASX], an ~$11 billion market cap company trading on the Australian Stock Exchange [ASX].

The royalty was acquired from Vonex Limited, which was a micro-cap telecommunications/Internet service provider. This deal has already paid out US$5.0+ million in revenue less than four years later with the mine still in production, an incredible payback for a producing asset. To put this in comparison for those investors less familiar with the Australian Market, this would be like transacting on a mine owned by Kinross Gold Corporation (KGC) with a near ~$10 billion market cap that’s already in production and still nailing down a sub 5-year payback which is unheard of for near production of producing assets held by majors.

Another example of an impressive deal was its acquisition of the Segilola royalty on Thor’s new gold mine in Nigeria, where it paid just ~$700,000 for a 1.5% NSR (capped at $3.5 million) on an asset in construction. And while buying capped royalties is not the most attractive move as it effectively caps any discovery upside, throughput expansions or mine life extensions, this royalty paid back in less than three years as well at 5x its purchase price. Hence, while I prefer not to see deals with caps or major step-downs, this is an investment that any royalty company would take any day of the week.

Finally, Vox completed a deal on Kookynie in 2020 (including the Puzzle Group deposits) which it paid ~$100,000 for, with this being one royalty in a larger royalty package, effectively making the price of this royalty even lower. This royalty included an A$1/tonne royalty for each ore reserve over a 100,000 tonne minimum hurdle, besides a per tonne royalty on tonnes mined once the asset is in production. And with the declaration of reserves of ~2.7 million tonnes at 1.30 grams per tonne of gold (~110,000 ounces), Vox was paid US$1.3 million or over 15x its royalty purchase price just over two years later.

Vox Royalty Track Record of Returns – Company Website

One of the massive benefits of this model is that Vox doesn’t get caught up in a battle of ever-increasing bids to scoop up these royalties because it’s often the only company aware of them, and these royalties often have motivated sellers, like Vonex was with Kooylanobbing because they were just happy to offload an ancillary asset and improve their balance sheet. Instead, Vox can make what it believes to be a reasonable offer and otherwise walk away, especially when it has nearly 9,000 royalties in its database across several commodities that it can extend offers on. And as the company highlights in its most recent Investor Letter and disclosure, it’s often evaluating over $500 million of potential royalty deals and can sit back and wait for the fat pitches as highlighted by Vox’s Founder, CEO & Chairman, Kyle Floyd, below:

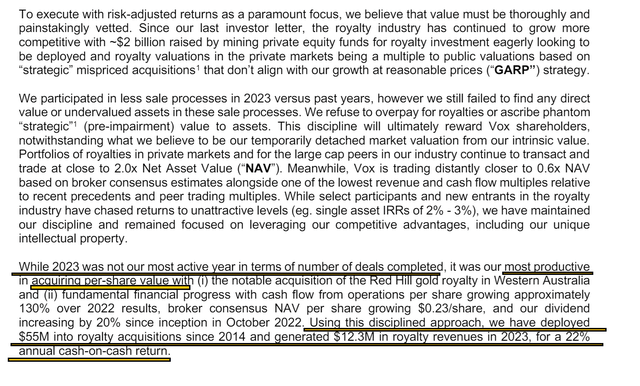

“Given we are focused on per-share returns versus speculative “strategic” value, our number of deals completed annually will vary year over year. We are never in a rush to deploy capital, and with the benefit of a strong balance sheet and growing free cash flow, we have the ability to be patient and only transact when value is compelling.”

“Our primary royalty acquisition focus remains pre-production royalties that range from six months to three years from first production, where we are able to diligence and price deals most consistently in line with historical Vox returns.”

– Vox 2024 Shareholder Letter.

Vox 2024 Shareholder Letter – Company Website

Talk is cheap, and the above points (“we refuse to overpay for royalties”) could be made by any royalty company. However, with the industry-leading IRRs enjoyed by Vox, it’s clear that they are delivering on their promises and staying true to their disciplined approach, which has ultimately helped to drive the impressive returns on deals completed to date. In fact, as Kyle Floyd recently outlined:

“To put this in context, of the nine assets that entered production – by the mid-point of 2025 we expect to be paid back on all nine of those assets with an average payback ratio of about 2.6 years. The industry equates to typically between 10 and 15 years for pay back on a mining royalty. So, it puts things in context our ability to source these assets at very dislocated values and do that systematically and repeatedly”.

– Vox Royalty, Planet MicroCap Presentation (emphasis added).

Critics of Vox’s early deals and massive paybacks could argue that while the returns are exceptional, most of the majors won’t roll out of bed in the morning for high IRR deals that might net $2.0 million in excess returns if they pay off. Other critics might note that Vox was lucky and jumped on assets in 2020/2021 when we were still seeing quite a few high IRR deals completed in the space as things were volatile because of the global pandemic. Finally, those interested in precious metals royalty might have passed on Vox given that it has generated the bulk of its revenue from iron ore royalties (Koolyanobbing/Wonmunna), and less revenue from gold (Janet Ivy) now that its Segilola royalty has hit its cap.

So, what has changed today?

Before digging into the portfolio and the game-changing acquisition announced in Q3 2023, it’s worth noting two things. The first is that the bulk of Vox’s development assets are on precious metals royalties so as this portfolio matures which is occurring as we speak with multiple new gold assets set to contribute over the next two years (Otto Bore, Bulong, Mt. Ida, Red Hill, Castle Hill, Plutonic East), gold will become the dominant revenue source for the company.

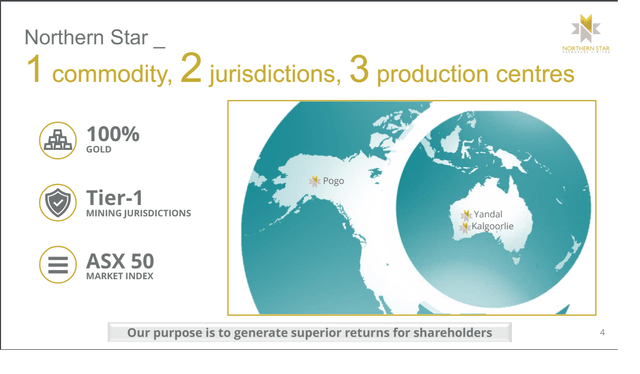

The second point worth noting is that growth is not years away like some royalty companies that are waiting for major assets to come online, and its producing royalty assets are mostly owned by massive and experienced operators, which is a rarity in the junior space. In fact, Vox’s Janet Ivy royalty (producing gold asset) is operated by Norton Goldfields (subsidiary of mega-gold company Zijin Mining), its iron assets are operated by an ~$11 billion market cap company (MinRes), its Otto Bore gold producing asset is operated by Northern Star (NST.ASX) which is Australis’s largest gold producer and a top-10 producer globally, and its soon-to-be producing Castle Hill royalty is owned by Evolution Mining (OTCPK:CAHPF), Australia’s 2nd largest gold producer.

Northern Star Resources – Company Website

For those unfamiliar with ASX-listed companies, Northern Star can be thought of the Australian Market’s Agnico Eagle Mines equivalent with large mines (KCGM, Jundee, Pogo), solely Tier-1 ranked jurisdictions, and Northern Star owns what will be a top-10 gold mine with it working to expand its Super Pit (KCGM) shown above to 27 million tonnes per annum or ~900,000 ounces per year later this decade. Currently, it is producing over 500,000 ounces of gold per annum from KCGM, but is growing into a 2.0 million ounce per annum gold producer across its portfolio as KCGM scales to nearly 1 million ounces per annum.

Hence, Vox has built a producing royalty portfolio operated by some of the best companies, and it’s done so while paying a fraction of the price it might have if it didn’t have its superior business model where it bids on hidden royalties, where it’s clearly seen immense success.

The result? Significant per share growth, and a relatively tight share structure compared to peers, with just 50 million common shares outstanding.

Fortunately, Vox has ample liquidity to keep up this growth with a ~$15 million RCF announced earlier this year ($10 million top-up option) and ~$10 million in net cash. And with the combination of consistent cash flow, a strong balance sheet and ample credit available at a much lower cost of capital, this could be Vox’s busiest year yet with the potential for significant growth in NAV/share.

Last, it’s important to point out that the company has seen an improved return profile while scaling up, with its deal size up ~8x from 2020 to 2024 (~$500k to ~$4.0 million) with higher returns. And as stated in the company’s shareholder letter, it expects 2024 to be a more active year with a focus on its sweet spot, which is 15 to 30-year-old legacy secondary royalties in Australia with production six months to three years away. Hence, with improved liquidity and the ability to take down larger deals, it’s possible that Vox could end the year with its estimated net asset value closer to US$4.00/share.

The Portfolio

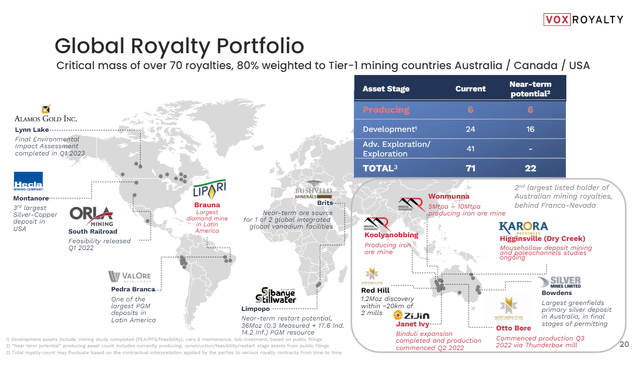

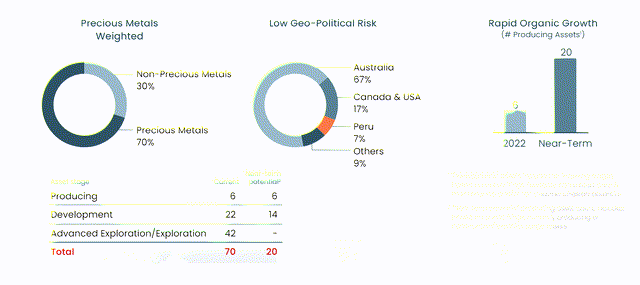

Looking at Vox’s portfolio, the company has over 70 royalty assets currently, which might seem low relative to peers with 100+ royalty assets. However, like Nomad Royalty which was acquired, Vox is focused on quality over quantity, with over 10% of this portfolio being producing assets by 2025, and over 20% being development assets. In fact, Vox’s producing assets could grow to closer to 20 assets in the next six years, tripling its current amount of producing assets. And as we’ll detail in the next section, one of these is a monster asset for a company of Vox’s size.

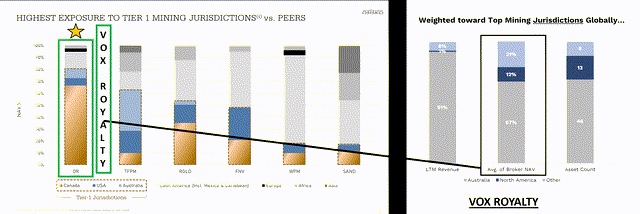

Vox Royalty Jurisdictional Profile – Company Presentation, Canaccord, Osisko Gold Royalties, Author’s Notes Vox Royalty Portfolio – Company Website

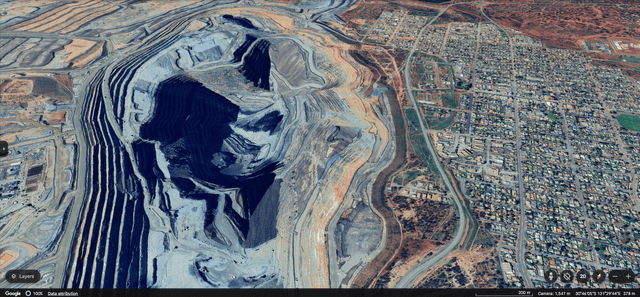

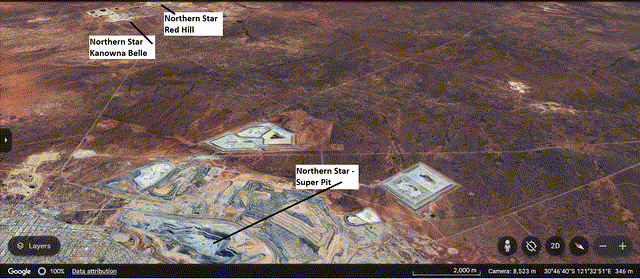

As for the jurisdictional weighting, Vox has ~80% of NAV tied to North America and Australia which should give it a premium multiple vs. most peers with less than 50% of NAV from Tier-1 ranked jurisdictions, with it ranking #2 among royalty companies in the above chart for its percentage of NAV tied to Tier-1 ranked jurisdictions. Meanwhile, nearly 70% of NAV is in Western Australia, which may rank #2 behind Nevada (according to Fraser Institute Annual Survey of Mining Companies) and close to Ontario/Quebec, but Western Australia is arguably more attractive given that permitting timelines are quicker while it remains a top jurisdiction in terms of mineral endowment. In fact, its flagship Red Hill royalty is expected to be processed at Australia’s largest gold mine, KCGM, otherwise known as the Golden Mile or Super Pit, which has produced over 60 million ounces of gold since the 1893 gold rush, with there being 49 operating mines, 100 headframes and over 3,000 kilometers of underground development in 1903 shortly after the gold rush began.

In fact, as detailed by historical accounts, prospectors uncovered rocks with such abundant levels of visible gold it was assumed to be pyrite (fool’s gold) and these rocks were discarded as waste and used for construction in Kalgoorlie. To the horror of those that didn’t ferret away this ore for themselves, it was discovered in 1896 that the rocks were tellurides – a compound of gold and tellurium that constitutes a smaller portion of the mineralization at Fimiston (KCGM Super Pit) today. Hence, for a brief period, the streets of Kalgoorlie were paved with gold. The sheer scale of this operation is shown below, adjacent to Kalgoorlie-Boulder.

Kalgoorlie Operations – Northern Star Website KCGM Super Pit – Google Earth

As for Vox’s commodity weighting, ~70% of its weight is in gold and silver, with a smaller weighting to iron ore, diamonds, copper, platinum group metals and some smaller royalty assets concerning vanadium, nickel, titanium, graphite, and even uranium.

Vox Commodity Weighting, Organic Growth Profile & Geopolitical Risk –

Looking at producing assets and its main development asset, there are several development assets highlighted on the above map that some might be familiar with, including a royalty on Orla’s (ORLA) South Railroad Project in Nevada, Alamos’ (AGI) Lynn Lake Project (albeit only a portion of the Maclellan Pit and with a capex recovery threshold), royalties on two massive PGM deposits (Limpopo and Pedra Branca), and optionality with Hecla’s (HL) Montanore deposit if it’s ever developed in Montana (3rd largest silver-copper deposit). However, one asset steals the show for Vox and this was added in a 2023 acquisition that entirely changed my view on the company from interested to excited and with continued resource growth at this asset over the past year, I think the market is sleeping on what this has done to separate Vox from its smaller peers with it now having its cornerstone asset.

This asset is Red Hill.

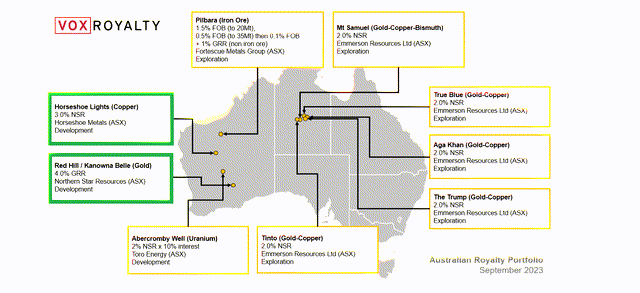

A Game-Changing Acquisition

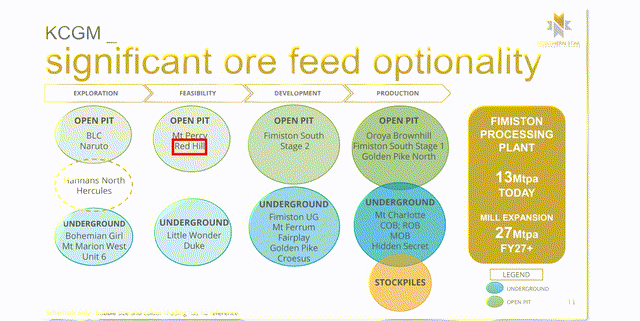

Vox Royalty announced an acquisition last fall for nine royalties at a cost of $4.5 million, including smaller exploration assets like Aga Khan (2% NSR), Tinto (2% NSR), True Blue (2% NSR), Mt Samuel (2% NSR), and a 3% NSR on a high-grade past producing copper asset, Horseshoe Lights. However, the best asset in the portfolio was Red Hill (shown below), an asset that Northern Star Resources has been talking a lot more about over the past two years that made it into a presentation last year as a future feed source for its KCGM Mill Expansion. For those unfamiliar with the asset, the expansion is currently underway and will add 14 million tonnes to KCGM’s processing capacity, effectively making it as big as Agnico Eagle’s Detour Lake, which processes ~28 million tonnes per annum.

Australia Royalty Portfolio Acquired by Vox, September 2023 – Company Website Red Hill Proposed Future Feed Source (Fimiston Plant) – Northern Star Presentation

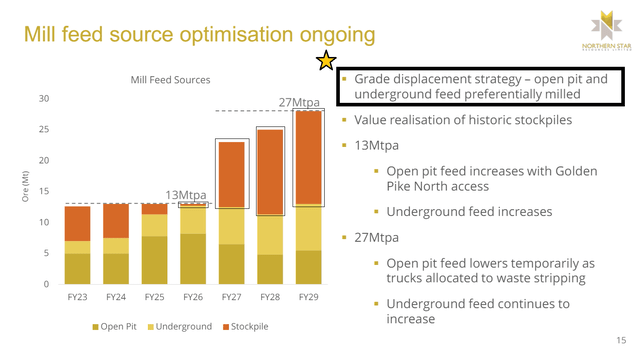

Red Hill was a past producing mine under Barrick Gold (GOLD) before its sale and in its last year it produced ~1.44 million tonnes at 1.86 grams per tonne of gold or ~81,000 ounces, and it previously generated over $5 million in royalty revenue at depressed gold prices earlier in the 21st century (2003-2008). This asset strategically lies just 3 kilometers from Northern Star’s Kanowna Belle operations and 20 kilometers north of Northern Star’s massive Super Pit, making it a very attractive ore source for displacing lower-grade feed and low-grade stockpiles at KCGM given the significant boost to capacity expected by FY2027 (calendar year H2-2026), which Northern Star has discussed in recent presentations (shown below).

As of the most recent update, Northern Star declared reserves at this asset in its annual reserve update (May 2024) following PFS level work, with plans to truck ore south to its Fimiston Mill.

Mill Feed Source Optimization (KCGM) – Northern Star Presentation

Besides the fact that Vox has picked up a 4.0% gross revenue royalty (up to 85% royalty coverage or effective ~3.6% royalty) on an asset that is sitting just over 20 kilometers from one the world’s largest future processing facilities (~27 MTPa), the price paid for this portfolio made it one of the best acquisitions I’ve seen in years. This is because the resource at the time of the acquisition was already ~1.2 million ounces at 1.1 grams per tonne of gold, giving Vox attributable production of ~18,000 ounces even at a 3.0% assumed effective royalty rate on future reserves (4% GRR x 70% – 75% coverage) and an assumed 50% resource to reserve conversion rate.

This translates to ~$36 million in future contribution at a $2,000/oz gold price or over 8x the acquisition price of US$4.3 million with eight other royalties all thrown in within the royalty package that was purchased.

Red Hill, Kanowna Belle Operations & KCGM Super Pit – Google Earth, Author’s Notes

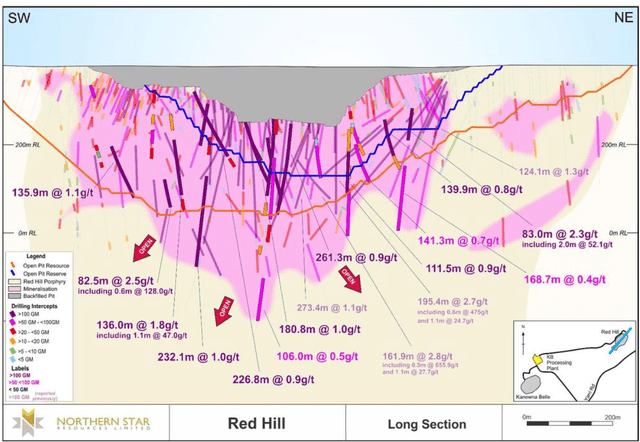

Fortunately, Vox not only paid this attractive price, but had the foresight to see that this asset was likely to grow. And as of Northern Star’s most recent update, Red Hill has grown its resource to ~1.9 million inferred ounces at 1.2 grams per tonne of gold, a ~60% increase in ounces with a 10% lift in grade. Meanwhile, Northern Star is clearly serious about this asset because it has declared a maiden reserve (PFS level work completed) of ~600,000 ounces (15.9 million tonnes at 1.1 grams per tonne of gold), and as shared in Northern Star’s additional disclosure, mineral resources are not reported because of a lack of data below 150 meters relative level, but it’s apparent that Red Hill remains open for future expansion – suggesting further growth in resources and reserves. It’s also worth noting that this reserve is based on a very conservative A$2,000/oz or ~US$1,300/oz gold price.

Red Hill Resource & Reserve Pit – Northern Star

Apart from the benefit of sharing some infrastructure with its Kanowna Belle operations next door, this is a low-strip future open-pit operation with the ability to strip the historical tailings and get right into ore before trucking it south to an existing plant – making it a low-capex and rapid payback opportunity. In addition, Northern Star stated it would do additional drilling this year, with drilling to increase geological confidence and test the current resource for “bulk potential below the Red Hill Pit.”

Other than Southern Cross [SXL.ASX] which has drilled some monster holes at the Sunday Creek Project in Victoria (Australia), the intercepts out of Red Hill are extremely impressive from a grade/thickness standpoint, with highlights that include 82.5 meters at 2.5 grams per tonne of gold, 232.1 meters at 1.0 gram per tonne of gold, 161.9 meters at 2.8 grams per tonne of gold (including 0.5 meters at 656 grams per tonne of gold), 83.0 meters at 2.3 grams per tonne of gold, 180.8 meters at 1.0 gram per tonne of gold, 261.3 meters at 0.90 grams per tonne of gold, and 135.9 meters at 1.1 grams per tonne of gold.

It’s important to note that several of these intercepts are mostly located outside of reserves, suggesting upside to deepening this pit and capturing more of this ~1.0 gram per tonne material.

Why is this important for Vox?

At a share price of US$2.40, Vox trades at an enterprise value of ~$110 million and generated just over $12 million in revenue last year. However, Red Hill alone has an estimated NAV of ~$50 million or US$1.00 per share at a long-term $2,100/oz gold price and covers roughly half of the company’s enterprise value today from this single asset. As for a production timeline, Red Hill could start contributing over $10 million in annual revenue by late 2026. If achieved, this would nearly double Vox’s annual revenue, pay back in less than six months on what appears to be a decade long mine life, and it looks like the deposit still has room to grow.

So, just like Orogen Royalties (OTCQX:OGNRF) saw rapid resource growth and future project economics on its cornerstone royalty asset in Nevada that allowed it to outperform its junior peer group, Red Hill has now given Vox a cornerstone gold royalty asset in the top mining jurisdiction from a geological attractiveness and permitting standpoint that should lead to a significant re-rating in the stock.

(*) Red Hill may not be a Silicon in scale with what’s likely to grow into a 2.5+ million ounce resource vs. 10+ million ounces at the Expanded Silicon Project, but the royalty coverage rate on Red Hill is more than three times as high, and it’s enough to seriously move the needle for Vox. (*)

Importantly, this was not a Hail Mary type transaction where Vox simply got lucky several years after acquiring this royalty. Instead, Red Hill was a low-risk shovel pass given that it was buying a massive royalty on a million-ounce gold project owned by the largest gold company in Australia next to the largest gold mine in Australia, with the processing capacity at that asset under expansion to double annual throughput. Despite the attractiveness of Red Hill, Vox didn’t buy this royalty and sit on it for years but stayed true to their transaction “sweet spot” of six months to three years to ensure superior returns on capital employed even with this being a phenomenal royalty asset with the potential to generate ~$10 million in annual contribution over what’s likely to end up being a 10+ year mine life.

In my view, this deal has confirmed that Vox’s success has not been taking value where others couldn’t be bothered (because of smaller-sized deals) in its early years, but that it clearly has a competitive advantage and can consistently find hidden value with its proprietary database. The evidence is in the price paid with a purchase price of less than 0.2x NAV on Red Hill (never mind the eight other assets) for a million-ounce resource near a hungry mill owned by a top-10 gold producer.

My assumptions around Red Hill assume a 1.1 million ounce reserve base (just 58% conversion to reserves), a conservative ~2.9% effective GRR (based on an estimated 73% royalty coverage). This equals to ~32,000 ounces of gold or $72 million in future contribution from this asset at $2,250/oz gold. However, production from Red Hill on a 100% basis could be higher in early years with higher grades and closer to 164,000 ounces, with the potential for closer to 5,000 ounces of attributable production in Year 1 and 2 assuming a processing rate of ~4.0 million tonnes per annum, grades of 1.45 grams per tonne of gold and an 88% recovery rate. This would mean ~$11 million in annual revenue in peak years ($2,250/oz gold price) from this single asset to Vox.

Other Royalty Assets

Aside from Vox’s producing royalties (which should generate upwards of $12 million in revenue this year) and the company’s cornerstone gold royalty asset, Red Hill, Vox has a solid portfolio of development assets in Tier-1 ranked jurisdictions. Some of these include:

1. Bullabuling – Norton Goldfields [Zijin Mining]

Vox has partial royalty coverage over a past-producing mine 70 kilometers southwest of Kalgoorlie and just west of Coolgardie that produced just shy of ~400,000 ounces. The project has a resource of ~3.21 million ounces at 1.05 G/T of gold and is expected to be a simple open-pit CIL project with a relatively short construction period, a strong operator in Norton Goldfields, and it boasts a 10+ year mine life producing upwards of 180,000 ounces per annum on average (~215,000 ounces in first three years). Vox receives a ~$7/oz payment for each ounce produced with partial coverage on the asset linked to the Bonecrusher and Dickson deposits (~775,000 ounces of resources), with upside at the Phoenix, Hobbit and Titan deposits.

Bullabuling Production Profile (2013 PFS), Vox Royalty Ground & Bullabuling Project – Vox Royalty, Bullabuling Gold

As for the strength of the operator, Zijin Mining’s market cap is larger than that of Agnico Eagle (AEM) and Barrick Gold combined, with Norton Goldfields (a subsidiary of Zijin) consolidating several gold projects in Australia starting in 2005, including Bullabuling.

This gold asset looks like it has a good shot at going into production later this decade and could contribute upwards of $0.3 million per annum to Vox Royalty over a 10+ year period, with upside from any extensions to mineralization and other deposits not currently in resources.

Vox’s royalty ground is highlighted in white and shown above, with the previously projected production profile on the left side of the image.

2. Bowdens Silver Project [Silver Mines Limited]

Another project where Vox has a royalty is Bowdens, a development stage open-pit silver, lead, and zinc project east of Mudgee in NSW, Australia. Notably, Bowdens is the largest known undeveloped silver project in Australia, with the project being home to ~400 million silver-equivalent ounces or ~190 million ounces of contained silver, and with it having received NSW mine development approvals (Q2 2023). A Feasibility Study completed in 2018 envisioned a 2.0 million tonne per annum and low strip (~1.6 to 1.0) open-pit mine, producing ~53 million ounces of silver, ~108,000 tonnes of zinc and ~79,000 tonnes of lead over a 16-year mine life, with ~5.4 million ounces of silver, ~5,200 tonnes of lead and ~6,000 tonnes of zinc in the first three years. Importantly, capex was estimated to be a very reasonable ~$160 million and ~$220 million, even assuming upwards of 35% inflation.

At prices of $28.00/oz silver, $2,500/tonne zinc and $2,100/tonne lead, this translates to ~$410 million in annual revenue or upwards of $3.0 million in revenue per annum to Vox in peak years based on a 0.85% gross royalty rate (resources). However, it’s important to note that while there’s an attractive open-pit project here at moderate grades, the underground resource is higher grade at ~200 G/T silver-equivalent and these higher grades are immediately beneath the current ore reserve base (open-pit ounces). And as Silver Mines has stated:

“the potential for a contiguous underground operation, in addition to the planned open pit operation, has firmed significantly as we further prove this large mineral system.”

(*) Vox has additional upside at this project long-term, with 1.00% royalty coverage on regional tenements. (*)

Open-Pit & Below Pit-Drilling + Bowdens Mineralization – Silver Mines Limited Website

Although early days, there appears to be the possibility for this higher-grade underground resource base to supplement the open pit starting after Year 3 of the mine life. Hence, while Vox will enjoy higher production in the first few years if Bowdens is brought online (Final Investment Decision targeted by year-end), it looks like the contribution to Vox could get even better post Year-3 under an optimized mine plan with higher-grade underground feed able to lift overall feed grades. And to put this asset in perspective, this one asset alone with significant leverage to silver prices would translate to nearly 30% growth for Vox relative to its guided FY2024 revenue midpoint of $12.0 million.

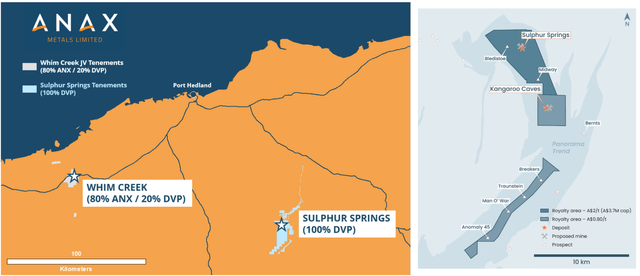

3. Sulphur Springs Project [Develop Global]

While one of the smaller assets in the portfolio, Sulphur Springs is another asset that could head into production this decade, with this VMS deposit home to ~24.4 million tonnes at 1.2% copper, 3.5% zinc and ~19 grams per tonne of silver or a reserve base of ~8.8 million tonnes at 1.1% copper and 5.4% zinc. Vox Royalty holds a ~$1.30/tonne royalty on Sulphur Springs up to a $2.4 million cap, but also an uncapped ~$0.52/tonne royalty on Kangaroo Caves, a nearby deposit with a resource of ~3.6 million tonnes at ~6.0% zinc and ~0.80% copper.

Vox Royalty Coverage & Proposed Synergies (Whim Creek / Sulphur Springs Leaching) – Develop Global, Vox Royalty

According to Develop Global, which has strong leadership in Bill Beament (built Northern Star into a multi-billion-dollar company from a shell company), recent work has yielded promising results. According to Develop and Anax Metals, there appears to be the potential to pull forward some production from this asset (which would benefit Vox) with recent metallurgical work on select oxide and transitional ore outside of reserves having the potential to be heap leached at Anax’s Whim Creek operation, with Whim Creek bacteria used to improve the leaching process.

Work is ongoing, and the real production would come down the road with plans to process ore at a ~1.3 million tonne per annum concentrator, but it sounds like this could bring forward some revenue to Vox near-term and give it another producing asset ahead of full production later this decade at Sulphur Springs (currently planned for 2028).

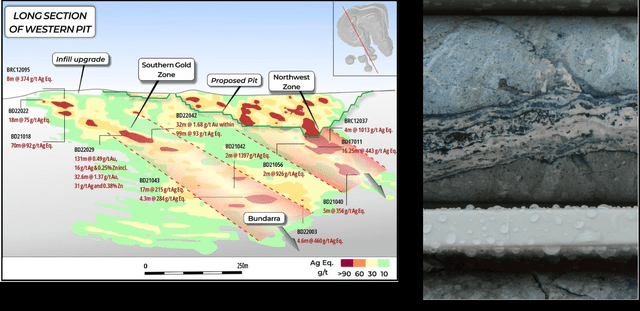

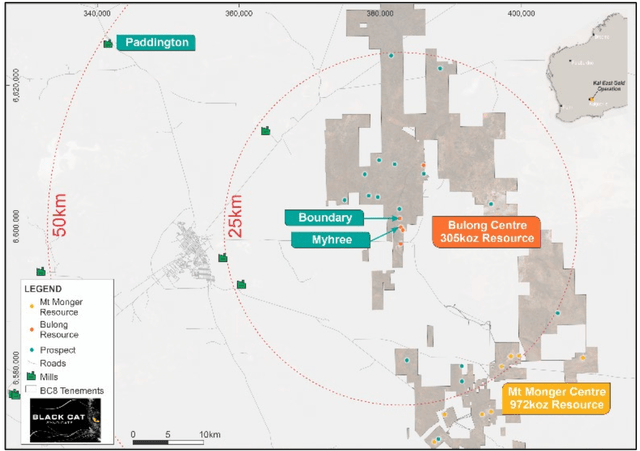

4. Bulong [Black Cat Syndicated Limited]

As for the Bulong Project east of Kalgoorlie where Vox has an uncapped 1.0% NSR covering multiple deposits (strategically located within 50 kilometers of five mills), Black Cat received some positive news recently. This news announced in late of May was that Black Cat has come to an agreement with Paddington Gold Pty Ltd (Norton Goldfields – Zijin Mining) and Mineral Mining Services to mine, haul and process high-grade open pit ore from its Myhree and Boundary pits at the Paddington Mill. The current agreement with Paddington provides for the allocation of 850,000 tonnes of open-pit ore delivered in stockpiles of ~135,000 tonnes per quarter starting in Q3 of this year.

Before this deal, I was assigning minimal value to Vox’s royalty assets owned by Black Cat [BC8.ASX] given that this was a relatively small junior with a decent portfolio of assets, but no clear path to developing them. However, this toll-milling deal to exploit Bulong Project ore requires no upfront funding from Black Cat and will generate cash flow to help fund its Paulsens Gold restart, when combined with other financing deals completed recently by Black Cat. As for Vox, this deal looks like it will bring in cumulative revenue of ~$1.3 million between Q3 2024 to Q4 2025, boosting revenue this year and next.

Paddington Mill & Boundary/Myhree Deposits – Black Cat Syndicate Limited

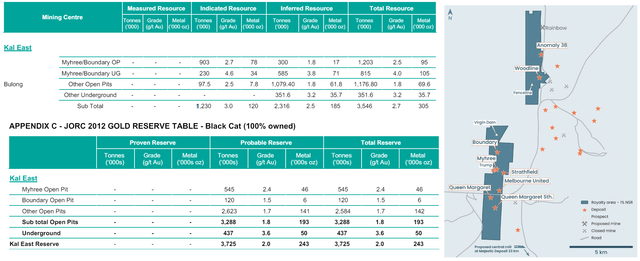

And while the current processing agreement focuses on just the Myhree and Boundary pits (~52,000 ounces in reserves at 2.24 grams per tonne of gold), and ~200,000 ounces in resources), we could see mining head underground if the deal is extended, providing additional contribution to Vox with grades being over 2x as high underground (~105,000 ounces at 4.0 grams per tonne of gold). Hence, this could be a solid ~$0.6+ million/year contributor for Vox on an asset I was previously modeling at zero this decade.

Vox Royalty Coverage (Right) and Resource/Reserves at Bulong – Black Cat Website, Vox Presentation

While this is positive news from a near-term revenue standpoint for Vox from an asset I wasn’t expecting to contribute soon because of conservatism given Black Cat’s previous financial position, there are two other positive takeaways here from this news.

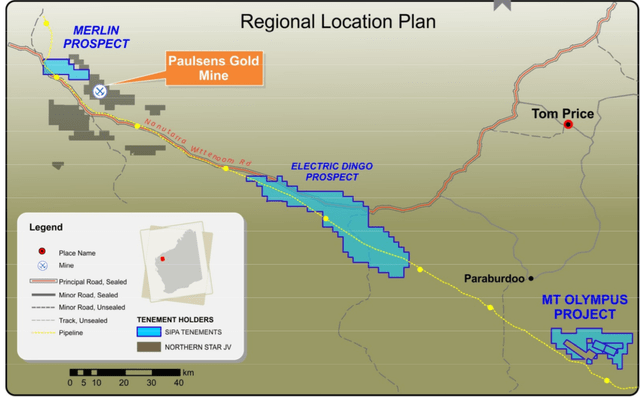

The first is that if Paddington is interested in nearby ore sources for its mill, Vox has significant royalty coverage at Bulong on other deposits covered by Vox with above-average open-pit grades. Second, Black Cat being in better financial shape means it can direct more exploration dollars to its higher priority operation, Paulsens Gold, where Vox has a 0.75% royalty on Merlin and a 1.75% royalty on Electric Dingo which are two mid-grade near-surface satellite opportunities that could provide feed for its ~450,000 tonne Paulsens Mill down the road.

Merlin & Electric Dingo Location vs. Paulsens Operation (Ownership Since Changed On These Assets) – Northern Star Filings

In summary, this deal not only provides contribution almost immediately to Vox from Myhree/Boundary which should see mining start next quarter, but it could also unlock two royalties (Merlin/Electric Dingo) I was assigning zero value to at Paulsens previously, given that an improved financial position for Black Cat and higher gold prices ultimately improves the outlook for these royalties as well. As further evidence of Vox’s disciplined capital allocation and ability to acquire at very attractive prices, the Bulong royalty was purchased for ~$0.49 million in June 2020 with the view that one of the five mills nearby might eventually want some of this above-average grade open-pit ore. As it stands, this deal looks like it will be fully paid back by next year, with all the upside from the other open-pit deposits and underground potential as gravy.

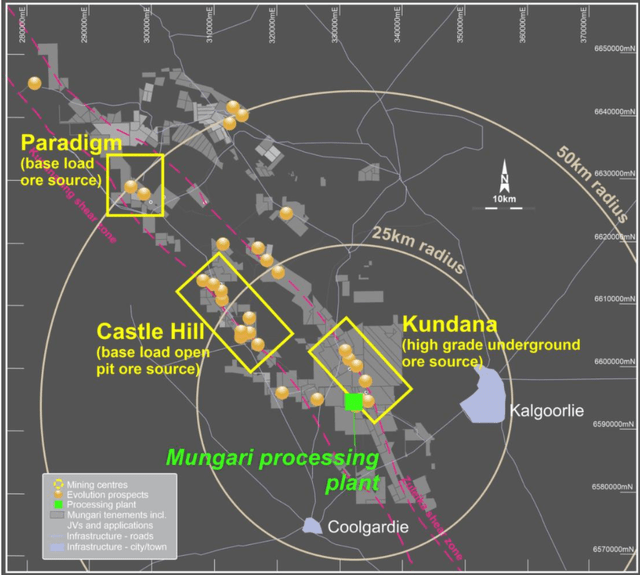

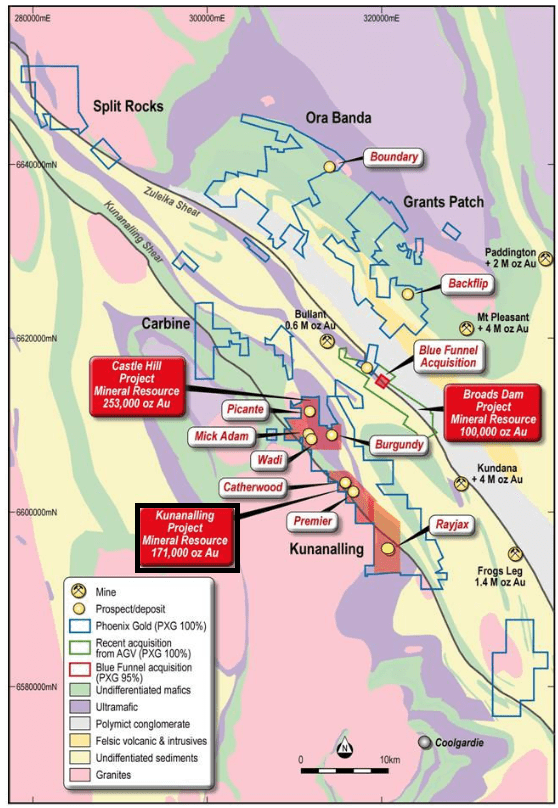

5. Castle Hill / Kunanaling [Evolution Mining]

Moving over to Castle Hill, Vox Royalty recently completed a deal for five royalties, with three held by Australia’s #3 gold producer, Evolution Mining. This included a payment of ~$30/oz up to 75,000 ounces of gold on Castle Hill, a ~$1.3 million payment following the recovery of 140,000 ounces of gold from Castle Hill and a 2% royalty on Kunanalling at Evolution Mining’s Mungari Mine, and there are numerous reasons to be excited about this deal.

Mungari Operations – Evolution Mining

For those unfamiliar with these assets, Castle Hill is a nearby open-pit reserve base with ~21.4 million tonnes at 0.89 grams per tonne of gold or 615,000 ounces that sits next to the Mungari Mill. This is expected to start production in 2026 and become one of the more significant contributors to gold revenue in Vox’s portfolio. And while there is a cap on this production, the milestone payment and production up to 75,000 ounces cover the purchase price of the deal, with it getting royalty exposure to the past-producing Kunanalling project adjacent to Castle Hill which covers ~150,000 ounces of gold resources. In addition, Vox picks up longer-term upside with a 1.5% NSR on a VMS copper deposit (Halls Creek) with modest capex that could produce ~38,000 tonnes of zinc and ~110,000 tonnes of copper according to a recent scoping study.

Mungari Operations – Evolution Mining

So, why is this ~$3 million deal so exciting?

Regarding Mungari, this is one of Evolution’s most important gold assets, and it’s currently undergoing a massive plant expansion to more than double throughput to 4.2 million tonnes per annum. This is expected to push production to ~200,000 ounces and extend Mungari’s mine life closer to 2040. This expansion came on the back of the ~$260 million acquisition by Evolution of Northern Star’s Kundana assets, consolidating the land package surrounding Mungari. So, Vox now has royalty coverage on a high-priority deposit next to Australia’s largest producer’s operation (Northern Star’s KCGM) which is doubling its mill capacity, but it also has royalty coverage on the region surrounding Australia’s second-largest gold producer’s operation (Evolution’s Mungari) which is also doubling mill capacity.

While not directly related to Mungari, there’s no question that Evolution’s Red Lake has been a disappointment (with the recent seismic event putting a further dent in planned production at Red Lake). However, even before recent seismic events that have impacted production in FY2024, Evolution Mining’s CEO Lawrie Conway stated last year that “Red Lake has got to earn the right to get capital.”

In my view, this is excellent news for Mungari which is an asset that is consistently generating net mine cash flow and has greater flexibility/synergies with the Kundana acquisition and the major plant upgrade. So, with leverage rapidly reducing for Evolution, much stronger net mine cash flow from Cowal UG and two steady gold-copper assets, I would think that Mungari is becoming a high priority to grow group gold production and stealing any dollars that might have otherwise gone to Red Lake.

Kunannaling Project Location – Phoenix Gold (now owned by Evolution Mining) – Phoenix Gold Website

Digging into the new royalty assets a little closer, Castle Hill will be a near-term contributor to Vox, but Kunanalling is also exciting with the past-producing Catherwood home to ~100,000 ounces at 2.0 grams per tonne of gold and previously/mined by Norton/Zijin in 2013 and transported to its Paddington Mill. And given the attractive open-pit grades here and proximity to the Mungari Mill, this certainly looks like a potential future feed source for its Mungari Mill, with this royalty essentially acquired for free given that Castle Hill (near-term producer) should pay for the acquisition price.

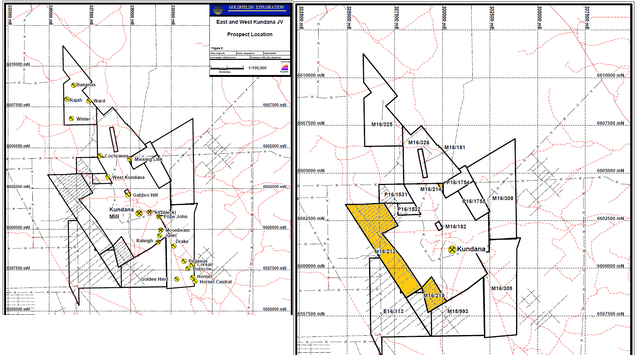

6. West Kundana [Evolution Mining]

Staying on the topic of Mungari, Vox also holds a 2.5% royalty on West Kundana which has been producing since 1988 and sits less than 1 kilometer from Kundana Underground operations (previously mined by Northern Star but sold to Evolution). As noted above, having royalty coverage on the third-largest gold producer’s #2 gold asset undergoing a major expansion provides enviable exposure, especially when its balance sheet is improving materially because of higher gold/copper prices.

Mungari Operations & Mill + West Kundana Location [WKJV] – Evolution Mining Website![Mungari Operations & Mill + West Kundana Location [WKJV]](https://wealthbeatnews.com/wp-content/uploads/2024/06/45984866-17185376542197795.png)

As highlighted above, Vox’s royalty coverage on West Kundana lies directly west of where Evolution is currently mining underground with royalty coverage on four mining leases (M16/213, M16/214, M16/218 and M16/310), highlighted in the below map. And while there’s no guarantee that Evolution delineates a significant resource and starts producing from this royalty ground, this is certainly close enough to care about when this ground is held by a large gold operator and this is its #2 gold operation with growing processing capacity right nearby. In fact, drilling is heading west of the Centenary Main Vein towards Vox covered ground. Recent highlight drilling west of its Genesis resource and underground workings hit 1.02 meters at 11.2 grams per tonne of gold.

Mining Areas & Vox Royalty Coverage WKJV Ground – Goldfields Exploration, GeoDocs

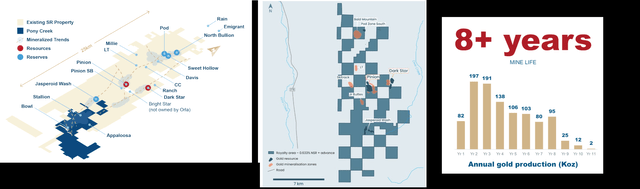

7. South Railroad [Orla Mining]

Moving to Nevada, Orla Mining (ORLA) has proven itself to be one of the best operators in the gold sector and one of only two producers to trounce the top end of its guidance the past two years. However, while the company’s current operation is a low-strip and mid-grade heap-leach asset in Mexico, recent acquisitions (Gold Standard/Contact) suggest it would like to expand into Nevada, and it has a commanding position along the Carlin Trend. Fortunately, Vox has royalty coverage on the South Railroad Project through a 0.633% royalty (in addition to advanced royalty payments of ~$80,000/annum) covering a portion of the highest-grade Dark Star deposit, a large portion of the main Pinion deposit (including the Pinion southern extension) as well as Jasperoid Wash and several other gold targets.

South Railroad Reserves/Exploration Targets, Vox Royalty Coverage (Blue – 2nd Image) & Production Profile – Orla Mining, Vox Royalty

Given Orla’s strong operational execution and backing (Fairfax, Pierre Lassonde), I don’t think there could be a better operator on this asset for Vox, with Orla being a producer hungry to grow on a prolific gold trend in Nevada that’s home to tens of millions of ounces of oxide/sulphide gold, including ~3.0 million ounces of gold resources in Orla’s inventory. Plus, Orla has proven that it’s an aggressive driller that is focused on growth, suggesting this could be a consistent $0.5 million per annum contributor for Vox over 10+ years given it has coverage on the Pinion Extension and I wouldn’t be shocked by mine life extensions and or expansions down the road with a goal of getting a Nevada premium.

Recent Developments & Longer-Term Optionality

As for other recent developments, Vox noted that it is leveraging its proprietary database that could result in excess contributions to its bottom line outside of royalty assets/advance payments with a deal to provide its database for coal royalties to a private royalty company – Perpetual Royalty IP Holdings LLC. If any deals are completed using Vox’s database, this would result in a cash transaction fee of up to 3% on the asset acquisition price, including any future earn out payments or contingent payments associated with any applicable coal royalty assets acquired.

I see this as a positive as it allows Vox to leverage its extensive database while not competing with its core commodities of interest, where it continues to work to acquire new royalties.

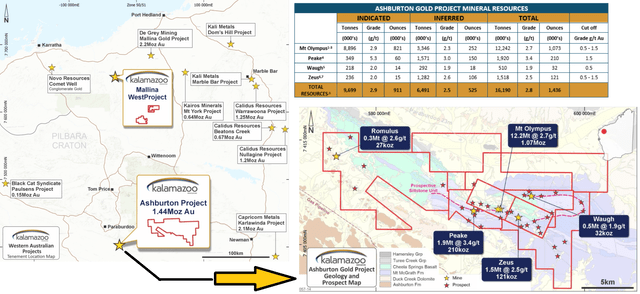

Ashburton

Outside this development, we’ve seen some other positive developments on its royalty assets. This includes De Grey Mining (DEG.ASX), which is one of the largest developers in Australia, executing an option agreement where it could acquire 100% of Kalamazoo’s Ashburton Project, which is home to ~1.43 million ounces at 2.8 grams per tonne of gold. This was a tough asset to place value on because of the bulk of the resource being refractory, which requires specific processing capabilities. However, with De Grey financing itself to build a massive 10 million tonne per annum operation at Hemi (with a 0.80 million tonne per annum pressure oxidation circuit), De Grey noted that it’s exploring the possibility of producing a high-grade sulphide concentrate at Ashburton and trucking the concentrate north to Hemi for further processing at its autoclaves.

Ashburton Project – Kalamazoo Resources – Kalamazoo Presentation

I would not expect this to come into production for the next few years at a minimum, but the potential to have Ashburton in the hands of a billion-dollar future producer (De Grey) with refractory processing capabilities is a massive upgrade from in the hands of a junior. That said, this could be a solid contributor for Vox next decade with its 1.75% royalty on Ashburton with significant royalty coverage across the 200+ square-kilometer land package that covers all the current resource base at Ashburton (Zeus, Romulus, Peake, Waugh, Mt. Olympus).

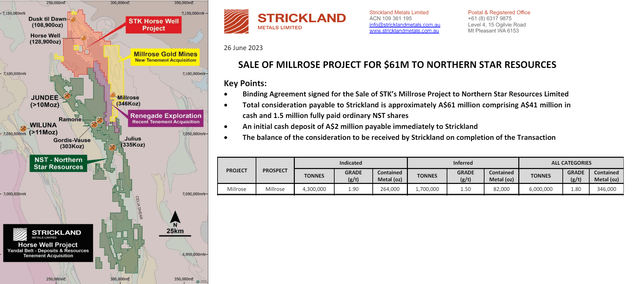

Millrose

The last asset worth touching is on the Millrose Project which lies just northeast of the producing Ramone Mine at its Jundee Operations which produced ~320,000 ounces last year at an industry-leading AISC of $900/oz. Just last year, Northern Star acquired the Millrose Project where Vox holds a 1.0% royalty for ~$40 million and while the royalty doesn’t cover the ~600,000 ounce mid-grade resource, it does surround the deposit to the north, east, and south, according to Vox. Northern Star plans to drill this asset this year, which lies 35 kilometers from the Jundee plant and Northern Star stated that Millrose remains open to the north and down-plunge.

Obviously, it’s early to put much value on this royalty, but Millrose certainly looks like it could be an important part of Jundee’s future at Northern Star’s #2 production center. So like Ashburton switching to stronger hands potentially, this is another upgrade in terms of this potentially contributing to Vox’s bottom line longer-term.

Millrose Project – Strickland Metals, Northern Star

Financial Results & Medium/Long-Term Outlook

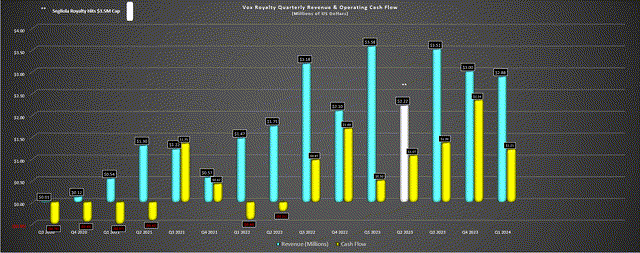

As for Vox’s financial results, the company generated ~$2.9 million in revenue in Q1 2024 which was down slightly year-over-year, but solely due to the Segilola royalty (cap has since been hit) not contributing. This was achieved at an 84% gross margin with operating cash flow of ~$1.2 million, and the company is guiding for up to $13 million in revenue this year. Notably, revenue has grown from $0 in 2019 to $12.3 million last year, and if not for Segilola rolling off would have been closer to $15.0 million this year, but this is a minor headwind in 2024 due to lapping revenue from this asset last year.

Vox Quarterly Revenue & Cash Flow – Company Filings, Author’s Chart

As for the medium-term outlook, revenue should increase year-over-year in 2024 despite lapping the Segilola royalty cap and I wouldn’t be surprised to see revenue increase to over $19.0 million in 2026 and closer to $28.0 million in 2027. However, 2026 could be stronger depending on the timing of initial production at Red Hill (I’ve assumed Q4 2026) and production levels at Castle Hill which will also kick in during 2026, as well as Bowdens which is getting closer to a potential full investment decision. Looking out to 2028, I would not be surprised to see revenue upwards of $30 million ($2,250/oz gold price assumption).

Vox Royalty Annual Revenue & Medium-Term Revenue Estimates – Company Filings, Author’s Chart & Estimates

However, one of the more important points that I don’t think the market appreciates is that this is a company consistently generating $1.00 in future revenue for $0.30 or less in sought-after jurisdictions for royalties and doing so with industry-leading NAV/share growth. Hence, if the previous constraint on growth was capital and not deal availability, I see significant upside to 2027 estimates if it can land a new deal or two in the next 12–18 months on near-term or producing assets. And with the ability to use cash flow and its balance sheet to transact, this could translate to accelerated growth in NAV/share and potentially an even lower cash flow multiple looking out to 2027/2028.

Valuation

Based on ~50 million shares and a share price of US$2.45, Vox trades at a market cap of ~$122 million and an enterprise value of ~$112 million. This makes it one of the smallest royalty companies in the sector today, with a market cap well behind that of its closer peers like Metalla (~$300 million), Gold Royalty Corp (~$260 million). However, Vox generated considerably more revenue and cash flow than Metalla and Gold Royalty Corp last year and will continue this pace in 2024, and it will also generate similar cash flow to both companies in 2026 despite trading at roughly one-third the enterprise value of these companies. This is because Red Hill has the potential to come online in late 2026 and generate over $10 million in contribution per annum, effectively doubling Vox’s annual revenue at the same time as other smaller assets come online and start contributing.

Vox Royalty Valuation vs. Peers (2026 EV/FCF Estimates) & 2027 Estimates – Company Filings, Author’s Chart, Author’s Estimates

The above quality score goes from 0 (weakest) to 10 (highest) and is weighted across multiple factors including track record of per share growth/overall capital allocation, competitive advantage, i.e., lower cost of capital, royalty generation, proprietary database), jurisdictional risk, diversification and scale, overall asset quality, strength of pipeline, quality of operators, and balance sheet strength/liquidity, with Vox ranking very well across several of these factors.

To better illustrate this undervaluation, we can look at the chart above, which shows multiple royalty companies with their estimated 2026 enterprise value to free cash flow multiples. As shown above, Vox trades at a massive discount to its smaller royalty peer group average. And even if you use multiples of 12x-15x vs. the peer average that sits closer to 20x EV/FCF (2026), Vox Royalty has an upside of ~45% to a multiple of 12x EV/FCF and ~75% upside at 15x EV/FCF on 2026 estimates from its current multiple of just over 8x EV/FCF estimates. Meanwhile, looking out to 2027 when we could see a full year of production from Red Hill, Vox has over 140% upside to fair value if it were to trade at 12x, given that it currently trades at ~5x 2027 EV/FCF estimates.

Importantly, the above chart and cash flow estimates assume that Vox does no new deals in the next two years that contribute cash flow to its 2026 estimates (~$12 million) even though it’s in the best position to date to transact with over $30 million in liquidity with its new BMO credit facility ($25 million), no debt, and nearly $10 million in cash. And while significant cash will build on its balance sheet over the next 30 months if it doesn’t do any transactions and contribute to this ultra-low EV/FCF multiple when combined with growing GEO sales, I’d obviously prefer to see cash deployed given the high IRR deals it’s been able to execute and potential for this to contribute to top-line growth later this decade.

2023 Revenue Vs. Capital Deployed vs. Peers – Vox Presentation, Company Filings

Some investors might argue that a multiple of 15x is too high for a small-scale royalty company (even if the multiples on other small-scale peers would suggest that clearly isn’t the case, as they trade at high double-digit FY2026 cash flow multiples). And to bake in conservatism, I have purposely looked at Vox using lower multiples (12-15x) than its peer group because it is not as diversified as some of its other names yet and its portfolio obviously doesn’t have the depth of its mid-tier peers. That said, Vox does have one thing that its peer group doesn’t have, and one thing that many of its peers lack, and it’s difficult to put a price on the value of either of these attributes. Both are worth a premium multiple in my view, but for the purposes of being conservative, I have still assumed a discounted multiple vs. where its junior peers trade for, highlighting its re-rating potential.

The first tangible benefit is a proprietary royalty database that has allowed the company to consistently purchase royalties at over triple the IRR of its peer group, with an incredible sub-3-year average payback to date. This is a massive competitive advantage that is challenging to put a price on because while there is little its peers from growing to the 50,000 GEO mark if they have access to capital, the benefit to shareholders will be considerably less compared to Vox, given that Vox is generating multiples of the returns on capital deployed. And in an environment that is only getting more competitive, I believe it’s a must to have a database to source deals from that doesn’t include battling in competitive auction processes, with the winner of these deals often walking away with low single digit IRR deals.

The second intangible benefit that cannot be overstated is shareholder alignment with over 18% insider ownership, a laser-focus on per share growth and extreme discipline when putting new capital to work. In fact, Vox’s capital discipline is inspiring not only among its smaller-cap peer group but across the sector – evidenced by a track record of low-risk transactions that are in line with their business model and consistently generate excess value for shareholders when they acquire.

As it stands, Vox has trounced its peers in terms of deal IRRs, and it’s not even close. Plus, this hasn’t been accomplished by venturing into high-risk jurisdictions or acquiring royalties on assets that will never head into production and making Hail Mary type transactions. In fact, the bulk of its NAV is tied to Tier-1 ranked jurisdictions (Western Australia, Ontario, Quebec, Nevada) with well over a dozen royalty assets held by large and/or very reputable operators (Alamos, Zijin, Northern Star, MinRes, Evolution, Develop Global).

The last point worth making is that while most investments in the small-cap royalty space require having a bullish view on a commodity or group of commodities to generate excess returns, I see Vox Royalty differently. In Vox’s case, I see an investment in the stock as investing alongside a team of highly disciplined and experienced individuals working to source deals with the help of a proprietary database that isn’t available to me. This is a far superior investment thesis vs. many companies in this sector that find a way to destroy value whether in bull/bear markets because they don’t have sitting power, they lack a competitive advantage, and the result is often sloppy acquisitions that don’t result in per share growth.

And when one invests alongside a team that puts shareholders first, is willing to be bold and acquire counter-cyclically and takes well-calculated risks like the Warren Buffett methodology of “don’t lose money,” these teams often command premium multiples, attract patient and supportive capital and the returns take care of themselves – like investors have seen with Agnico Eagle (AEM) and Alamos Gold (AGI).

Balance Sheet, Share Structure, Technical Picture

The last point worth noting is that while Vox Royalty has done an incredible job given its shoestring budget to date, it’s now in the best position it’s ever been in to transact with over $30 million in liquidity. This stems from its new BMO credit facility ($25 million), no debt, and nearly $10 million in cash. And when you have a company regularly creating a dollar out of $0.20 to $0.30 invested like Vox, it’s certainly an exciting time to be a shareholder, given that we should see accelerated growth in NAV/share with any new deals able to be funded without any share dilution.

Second, while some of its royalty peers have convoluted share structures, Vox has an extremely clean share structure and balance sheet with no debt, no warrants, and no converts. This is a superior setup relative to most of its small-ca peers that have shown little hesitation issuing shares at a deep discount to NAV (including full warrants in some cases) in the past year. This is another reason that Vox stands out vs. peers and could see share price outperformance vs. its peer group, outside the multiple other superior attributes addressed already.

Vox Royalty Shares & Share Structure + Insider Ownership – Company Presentation

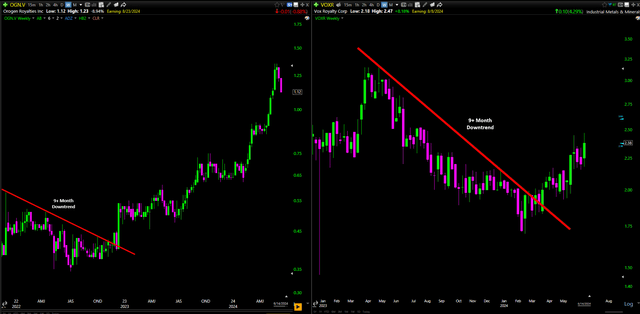

Finally, looking at the technical picture, Vox has a similar look to Orogen Royalties before its major move, recently breaking out of a 9+ month downtrend and seeing strong follow-through to this downtrend break. And while history doesn’t have to repeat, it often rhymes, with the fundamentals for both companies quite similar. This is because as noted earlier, AngloGold’s (AU) enormous resource growth and development upgrade (higher likely of being developed and accelerated) was a major catalyst for a re-rating in Orogen with its Upper Silicon royalty, with the stock undervalued given that it had a key royalty held by a gold major in a Tier-1 ranked jurisdiction that had suddenly piled on significant NAV upside.

And as discussed earlier, I believe Vox’s Red Hill is akin to Orogen’s Silicon in terms of significance from a re-rating standpoint, with Red Hill actually set to go into production earlier with the potential to start cash-flowing by H2 2026 (already in reserves and near a fully constructed and operating mill).

Vox Royalty Chart vs. Orogen Royalties – TC2000.com

Overall, I see Vox Royalty as the most attractive opportunity in the royalty/streaming space today, especially if this team can keep up its remarkable track record of transacting at industry-leading IRRs. In fact, I think Vox Royalty today is the closest thing to investing in a name like Royal Gold (RGLD) over twenty years ago ahead of what’s been a 20x return because Vox Royalty has the massive benefit of a lack of competition – a headwind to generating per share growth in the royalty/streaming space today.

So, for investors that missed Royal Gold in the 1990s, an investment in Vox today is similar to pulling the lever on a time machine and getting a second chance at the two major royalty companies before competition got fierce and average IRRs reverted to far less attractive levels. Co-founder of Mineral Royalties Online (acquired by Vox) and the current Chief Investment Officer of Vox Royalty, Spencer Cole, goes into more detail on their proprietary royalty database and its competitive advantage below:

“So, what does it actually mean ? Identifying high-quality royalties that our competitors are blind to. So, you know I’ll give you a few real examples. We bought a gold royalty from a hearing-aid technology company. We bought an iron-ore royalty from a telecommunications company. These are such strange owners of mining royalties that our competitors would never knock on their door, but we could see in our database that these non-mining companies that used to be a listed mining shell company, we could see they still held these interesting royalty contracts.

We often approach these holders of royalties and we say ‘We see you own a gold royalty – we’d like to buy it’. They say ‘No, no, no, we’re an automotive company, we don’t own mining royalties’. And we actually have to convince them – ‘No, you do still own in your legal shell, you still own a royalty and we’d like to buy it’. It’s like buying a house – if there’s no other buyers knocking on the sellers’ door, you’re obviously going to get a better price as the buyer.”

– Vox Royalty Interview, Invertir Como Un Professional, Draco Global (emphasis added).

Summary

Vox Royalty has a superior business model with a clear competitive advantage vs. its royalty/streaming peers. Just as importantly, it has a leadership team that’s aligned with shareholders (~18% insider ownership) and has done an exceptional job deploying capital to date, with an average payback of less than three years.

So with growing exposure to precious metals royalties owned by some of the largest operators in safe jurisdictions, a significant undervaluation and a peer-leading 2% dividend yield, I see Vox as one of the most attractive ways to add precious metals exposure to one’s portfolio.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here