The Invesco Senior Income Trust (NYSE:VVR) is a closed-end fund that income-focused investors can purchase as a method of achieving a very high level of income from the assets in their portfolios. This fund has been very good at the provision of income over the past few years due mostly to the types of assets that it holds in its portfolio. This fund holds mostly senior leveraged loans that have floating interest rates with a 4% to 6% spread over the secured overnight financing rate, which is typically pretty close to the federal funds rate. As the federal funds rate has been rising over the past few years to its current level of 5.33%, this has resulted in most of the securities held by this fund delivering a double-digit yield. When combined with the effects of the leverage employed by this fund, we can quickly see how it would end up being very attractive to any investor who is seeking to earn a high level of income.

The Invesco Senior Income Trust yields 11.83% at the current share price, which compares reasonably well to its peers. This is shown in this chart:

|

Fund Name |

Morningstar Category |

Current Yield |

|

Invesco Senior Income Trust |

Fixed Income-Taxable-Senior Loans |

11.83% |

|

BlackRock Floating Rate Income Trust (BGT) |

Fixed Income-Taxable-Senior Loans |

11.22% |

|

Eaton Vance Senior Floating-Rate Trust (EFR) |

Fixed Income-Taxable-Senior Loans |

9.87% |

|

First Trust Senior Floating Rate Income Fund II (FCT) |

Fixed Income-Taxable-Senior Loans |

11.26% |

|

Nuveen Floating Rate Income Fund (JFR) |

Fixed Income-Taxable-Senior Loans |

11.55% |

|

Pioneer Floating Rate Fund (PHD) |

Fixed Income-Taxable-Senior Loans |

11.13% |

As we can immediately see, the Invesco Senior Income Fund has the highest yield currently available among its peer group. With that said, there is very little difference between the yields of any of these funds (with the exception of the Eaton Vance Senior Floating Rate Trust). This is mostly because floating-rate securities do not ordinarily fluctuate very much in price, which makes it very difficult for a fund to find mispriced securities and generate capital gains. Most of the returns come from the coupons paid out by these securities, and in most cases, a security’s coupon yield will be fairly similar to others that have similar risk characteristics. Thus, it is pretty difficult for any fund to pay a yield much higher than its peers.

As regular readers might remember, we previously discussed the Invesco Senior Income Trust in late October of 2023. That article was published right around the time that bond yields peaked and equity prices bottomed out following the somewhat disastrous summer of 2023. The market for both fixed-income and equity securities has generally been stronger since the date that my previous article on this fund was published. Bonds have been somewhat more volatile than common stocks, though, as the market was predicting aggressive interest rate cuts at the start of 2024 that never materialized. Overall, bonds still never fell back to their October 2023 lows. However, it is worth noting that floating-rate securities, such as the ones in this fund, are not affected by interest rate changes due to the fact that they always pay the market yield. The share price of this fund also might not trade perfectly in line with the value of floating rate securities, and many closed-end funds have delivered share price performance exceeding the performance of their underlying portfolios over most of this year. As such, we can probably expect that the Invesco Senior Income Trust has delivered a reasonable performance since last October.

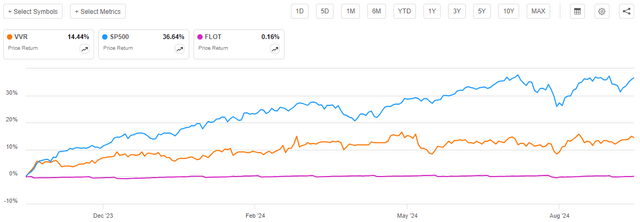

This is indeed the case, as shares of this fund have appreciated by 14.44% since the date that my previous article was published:

Seeking Alpha

As we can see, the fund’s share price performance was not nearly as good as that of the S&P 500 Index (SP500) but that is largely expected. It is very rare for fixed-income securities to keep up with common stocks, after all, and such strong performance for fixed-income securities usually only occurs during a recession. The more interesting thing to note here is that the shares of the Invesco Senior Income Trust substantially outperformed the U.S. Floating-Rate Note Index (FLOT), which was flat as expected. This could be a sign that the fund’s shares have greatly outperformed its underlying portfolio, and that could have a negative impact on the fund’s valuation. We will want to have a closer look at this over the remainder of this article.

As I stated in a recent article:

Closed-end funds typically pay out most to all of their investment profits to their shareholders in the form of distributions. The basic goal is to keep the investment portfolio relatively stable and give the investors all of the investment returns in excess of the amounts needed to cover the fund’s expenses. This is the reason why many funds, including this one, tend to have very high yields. These distributions result in the actual return received by investors being significantly higher than might otherwise be assumed simply by looking at the share price performance. As such, we need to consider the distributions that are paid by the fund in any performance analysis.

The Invesco Senior Income Trust has a substantially higher yield than that of the S&P 500 Index or the domestic floating rate note index:

|

Index |

TTM Yield |

|

S&P 500 |

1.33% |

|

U.S. Floating Rate Note Index |

5.96% |

As such, we can expect the fund’s total return performance to receive a larger boost from the distributions than either of the two indices. This is indeed the case, which we can see by looking at the total return of each of the assets over the same period as the previous chart:

Seeking Alpha

As we can see, the Invesco Senior Income Trust has delivered a 26.70% total return to its investors over the roughly eleven-month period shown above. This is far better than the meager return offered by the floating-rate note index, but it still was not able to keep up with large-cap domestic stocks. In most circumstances, we would expect this fund’s total return to be between those two asset classes, so this is not particularly surprising.

As eleven months have passed since our previous discussion on this fund, we can expect that a great many things have changed. One of the most important things that could have changed in the macroeconomic environment is that the Federal Reserve has become much more dovish and is widely expected to begin reducing interest rates later this week. If that occurs, it will cause the securities held by this fund to have lower coupon yields and likely reduce the fund’s distribution. In addition, the fund has released a few updated financial statements since our previous discussion, so we should have a look at those to make sure it is still covering its distribution appropriately. The remainder of this article will focus on these tasks.

About The Fund

According to the fund’s website, the Invesco Senior Income Trust has the primary objective of providing its investors with a high level of current income. This is a very reasonable goal for a fixed-income fund, as fixed-income securities deliver the bulk of their returns through direct payments to their owners. It makes even more sense for a floating-rate fund due to the fact that floating-rate securities deliver all of their returns through direct payments to their owners. We can see this by looking at the Bloomberg U.S. Floating Rate Note Index. There are two exchange-traded funds that track this index:

- SPDR Bloomberg Investment Grade Floating Rate ETF (FLRN)

- iShares Floating Rate Bond ETF

Here is the ten-year price chart for both index funds:

Seeking Alpha

We can see that, with the exception of a few weeks surrounding the outbreak of COVID-19, the index funds were largely flat. The majority of the price movement that we see was due to timing between when the funds received the coupon payments from the bonds and when they paid out the money to the investors. Overall, we can see that the assets themselves were pretty much flat regardless of any movement in interest rates.

Admittedly, those indices primarily track investment-grade floating-rate notes. Leveraged loans are generally below-investment-grade securities because they are made to companies that have limited cash flow or a lot of debt already. However, the prices of these bonds should generally move pretty similarly to that of investment-grade bonds. The real difference in returns between investment-grade floating-rate securities and speculative-grade floating-rate securities comes from the yield offered by each type of security. Obviously, leveraged loans are going to have a substantially higher yield than investment-grade floating-rate securities.

The Invesco Senior Income Trust invests primarily in below-investment-grade floating-rate securities, as explained in the most recent annual report:

The Trust invests primarily in floating or variable rate senior loans to corporations, partnerships, and other entities which operate in a variety of industries and geographical regions (including domestic and foreign entities). Senior loans hold a senior position in the capital structure of U.S. and foreign corporations, partnerships or other business entities that, under normal circumstances, allow them to have priority claim ahead of (or at least as high as) other obligations of a borrower in the event of liquidation. Senior Loans generally are arranged through private negotiations between a Borrower and several financial institutions represented in each case by one or more such Lenders acting as agent of the several Lenders. The Trust may invest in participations in Senior Loans, may purchase assignments of portions of Senior Loans from third parties and may act as one of the group of lenders originating a Senior Loan.

In normal market conditions, at least 80% of the Trust’s total assets are invested in Senior Loans of domestic Borrowers or foreign Borrowers. In complying with this 80% investment requirement, the Trust may invest in derivatives and other instruments that have economic characteristics similar to the Trust’s direct investments that are counted towards the 80% investment requirement.

…

In normal market conditions, the Trust may invest up to 20% of its total assets in any combination of (1) equity securities, (2) junior debt securities or securities with a lien on collateral lower than a senior claim on collateral, (3) high quality short-term debt securities, (4) credit-linked deposits, and (5) Treasury Inflation Protected Securities and other inflation-indexed bonds issued by the U.S. government, its agencies or instrumentalities. Warrants, equity securities and junior debt securities will not be treated as Senior Loans and thus assets invested in such securities will not count toward the 80% of the Trust’s total assets that normally will be invested in Senior Loans.

This description makes it very clear that the Invesco Senior Income Trust primarily invests in senior loans, which are typically floating-rate securities. This is evident in the fact that the fund is mandated to have at least 80% of its assets invested in such securities. However, as of right now, it appears that the fund has more than that percentage invested in these securities. The fund’s first-quarter 2025 holdings report provides the following asset allocation as of May 31, 2024:

|

Asset Type |

% of Net Assets |

|

Variable Rate Senior Loan Interests |

137.73% |

|

Common Stocks and Other Equity Interests |

7.88% |

|

U.S. Dollar-Denominated Bonds and Notes |

4.66% |

|

Non-U.S. Dollar-Denominated Bonds and Notes |

3.34% |

|

Preferred Stocks |

1.65% |

We can very clearly see that the overwhelming majority of the fund’s assets are invested in variable-rate senior loan interests. This is pretty much what we expected to find, and as such the discussion that we just had about the performance of floating-rate securities should apply to this fund. The common stocks as well as the fixed-rate bonds and preferred stocks might add a bit of volatility compared to what we would see from a straight floating-rate securities index, but overall, the portfolio should prove relatively stable.

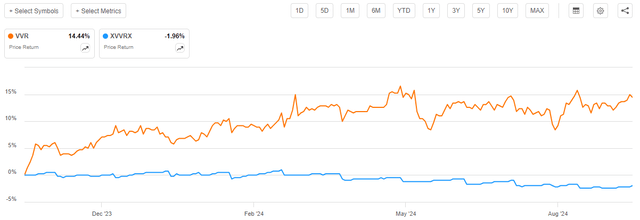

This makes it a bit difficult to explain the share performance of this fund. As we saw in the introduction, the fund’s share price has risen by 14.44% since our October 27, 2023, discussion. The fact that this fund’s portfolio is primarily invested in floating-rate securities strongly suggests that the assets comprising the portfolio should not have appreciated to that extent. In fact, this is exactly the case, as we can clearly see by looking at this chart comparing the fund’s share price to its portfolio:

Seeking Alpha

The portfolio itself is actually down by 1.96% since our previous discussion. This is a very substantial disconnect between the share price performance and the underlying portfolio. When we consider that the fund’s net investment income will begin to decline once the Federal Reserve reduces short-term interest rates in earnest, this could potentially represent a risky situation for anyone buying the fund today. Potential investors or even current investors should certainly take this into consideration when determining their next move.

Below-Investment-Grade Focus

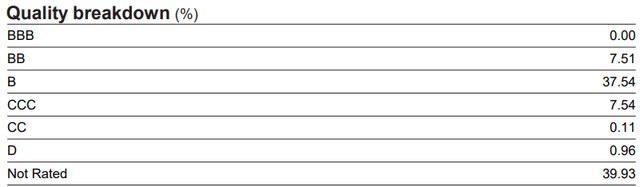

As mentioned in my previous article, as well as earlier in this one, the Invesco Senior Income Trust primarily invests its assets in below-investment-grade securities. We can see this by looking at the credit ratings assigned to the securities in the fund’s portfolio. Here is the breakdown as of June 30, 2024:

VVR Fact Sheet

An investment-grade security is anything rated BBB or higher, so it appears that the fund is not holding any investment-grade debt assets. This is a decrease from the last time that we discussed this fund, as it did have 0.16% of its portfolio invested in investment-grade credit at that time. We do see a few other changes as well, and they generally point to the fund’s portfolio being a bit riskier than it was the last time we looked at it:

|

Credit Rating |

% of Total Assets Today |

% of Total Assets Previously |

% Change |

|

BBB |

0.00% |

0.16% |

-0.16% |

|

BB |

7.51% |

10.09% |

-2.58% |

|

B |

37.54% |

35.73% |

+1.81% |

|

CCC |

7.54% |

6.93% |

+0.61% |

|

CC |

0.11% |

0.15% |

-0.4% |

|

D |

0.96% |

0.00% |

+0.96% |

|

Not Rated |

39.93% |

39.44% |

+0.49% |

We generally see decreases in the weightings of the highest-rated securities and increases in the weightings of lower-rated securities. This suggests that the fund is increasing the risks that it takes on in an attempt to get higher yields. However, it is possible that some of this might be due to the financial pressure that the most indebted companies have been under over the past year. Back in June 2024, the Associated Press made the following observations:

They are called zombies, companies so laden with debt that they are just stumbling by on the brink of survival, barely able to pay even the interest on their loans and often just a bad business hit away from dying off for good.

An Associated Press analysis found their numbers have soared to nearly 7,000 publicly traded companies around the world – 2,000 in the United States alone – whiplashed by years of piling up cheap debt followed by stubborn inflation that has pushed borrowing costs to decade highs.

The decade-long period of low interest rates from the financial crisis until 2022 allowed a lot of companies with very limited business prospects to survive simply by borrowing money. After all, money during that era was basically free and all they needed to do was produce the small amounts of money needed to cover their tiny loan payments. This has been cited as one reason why the S&P 500 Index outperformed the Russell 2000 Index (IWM) over the 2010 to 2020 period, as the significant number of these zombie companies in the Russell 2000 dragged down the performance of small-cap stocks relative to financially strong large-caps. Once interest rates started rising, these zombie companies could no longer eke out a meager profit due to a growing proportion of their limited cash flow having to go to debt service. This pushed down their credit ratings from higher levels of speculative-grade to deep junk territory.

It is possible that this is one of the reasons why this fund’s portfolio credit allocation appears to have weakened over the past year. It has simply gotten more difficult for the companies in the fund’s portfolio to carry their debt loads and their credit ratings have declined as a result.

In my previous article, I made the following observation:

This is something that may concern some investors, particularly those of a more conservative nature, such as retirees. This is due to the fact that junk debt has a considerably higher default rate than traditional investment-grade debt. The fund’s fact sheet states that it has had a default rate of 5.05% over the past twelve months, which is considerably higher than would be found in an investment-grade credit fund.

Interestingly, the fund’s default rate has declined significantly over the past eleven months. The fact sheet states that the fund had a default rate of 2.29% over the July 1, 2023 to June 30, 2024 period. This reduction in the default rate comes despite the fund’s apparent increased exposure to lower-rated securities. There was only one increase in interest rates over that period, whereas there would have been several more during the twelve-month period ending in September 2023. Thus, it is possible that the worst-financed companies were pushed into default during the rapid rise in interest rates during 2022 and early 2023, while the ones still in existence are better equipped to handle it. It is also possible that the fund’s management is being a bit more careful about avoiding the weakest companies today than a year ago.

In any case, the fund’s default rate currently appears to be low enough that any money lost through defaults will quickly be offset by the coupon payments that come from the remaining securities in the fund. This fund has 523 holdings, and nothing accounts for more than 2.69% of the portfolio, so a single default should not hurt it too much.

Leverage

As is the case with most closed-end funds, the Invesco Senior Income Trust employs leverage as a method of boosting the effective yield that the fund earns from the assets in its portfolio. I explained how this works in my previous article on the fund:

In short, the fund borrows money and then uses that borrowed money to purchase floating-rate securities. As long as the interest rate that the fund pays on the borrowed money is less than the yield that it receives from the purchased assets, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably cheaper than retail rates, that will usually be the case.

Unfortunately, the use of leverage in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much debt because that would expose us to an excessive amount of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Invesco Senior Income Trust has leveraged assets comprising 32.12% of its portfolio. This is pretty similar to the 32.45% leverage that the fund had the last time that we discussed it. It is also pretty similar to the 32.19% leverage that the fund had when we discussed it in August of 2023. Thus, it does not seem that this fund is really changing its leverage very much. It might be borrowing a small amount of money from a revolving credit line or something similar, but it does not appear to be issuing any long-term debt.

As we saw earlier in this article, the Invesco Senior Income Trust’s net asset value declined slightly from the last time that we discussed it. This would normally cause its leverage to increase slightly, but that was not the case here. That suggests that the fund paid back a bit of the money that it had borrowed against a revolving line of credit at the time of our previous discussion. This makes sense, as the fund’s investment income is likely to start declining in the near future so it may want to be a bit more cautious.

The fund is below the one-third of assets leverage level that we normally consider to be reasonably acceptable for a closed-end fund. However, that is just a general rule and may not apply to every possible strategy, so we should compare the fund’s leverage to that of its peers to make sure that it is acceptable for its strategy. Here is a comparison chart:

|

Fund Name |

Leverage Ratio |

|

Invesco Senior Income Trust |

32.12% |

|

BlackRock Floating Rate Income Trust |

23.49% |

|

Eaton Vance Senior Floating-Rate Trust |

33.50% |

|

First Trust Senior Floating Rate Income Fund II |

10.95% |

|

Nuveen Floating Rate Income Fund |

38.00% |

|

Pioneer Floating Rate Fund |

32.00% |

(all figures from CEF Data)

We can see that two of the funds in this peer group have substantially lower levels of leverage than the others. However, there are still four of them with more than 30% leverage. The Invesco Senior Income Trust is not at all out of line with these four higher-leverage funds, so it does not appear as though it has too much leverage compared to its peers. This is a good sign from a risk-management perspective, and it tells us that investors should not need to worry too much about the fund’s leverage right now.

Distribution Analysis

The primary objective of the Invesco Senior Income Trust is to provide its investors with a very high level of current income. To this end, the fund pays a monthly distribution of $0.0430 per share ($0.516 per share annually). This gives it an 11.83% current yield, which is reasonably in line with the fund’s peers.

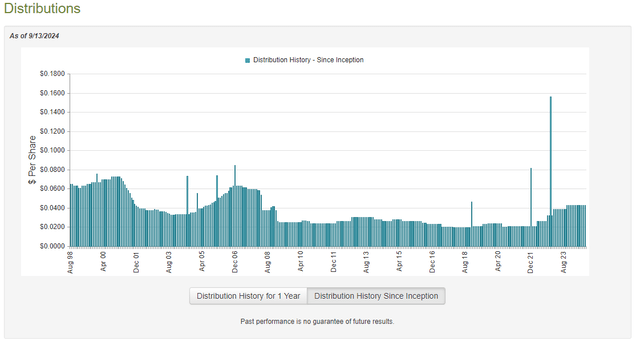

Unfortunately, this fund has not been especially consistent with respect to its distribution over the years:

CEF Connect

As I stated in the previous article:

This is something that may not inspire much confidence into those investors who are seeking to earn a safe and sustainable level of income from the assets in their portfolios. That goal could be necessary for retirees and others who are dependent on their portfolios to generate the income that they need to pay their bills or finance their overall lifestyles.

The fund has managed to keep its distribution steady at $0.0430 monthly since our last discussion, following a series of distribution increases over the twelve-month period preceding that article. The fluctuations are due to the fact that the fund’s income and total investment return depend on short-term interest rates, as already discussed. Thus, we can expect its distribution to generally move alongside such rates.

The fund has released a new financial report since our last discussion, so let us take a look at it and see how well the fund is covering its current distribution. As of the time of writing, the most recent financial report is the annual report for the full-year period that ended on February 29, 2024. A link to this document was provided earlier in this article.

For the full-year period that ended on February 29, 2024, the Invesco Senior Income Trust received $98,294,599 in interest along with $3,819,735 in dividends from the assets in its portfolio. When we combine this with a small amount of income from other sources, we get a total investment income of $102,115,374 for the full-year period. The fund paid its expenses out of this amount, which left it with $69,690,876 available for shareholders. That was not sufficient to cover the $74,683,461 that the fund paid out to its investors during the period.

Unfortunately, the fund was not able to make up the difference through capital gains. For the full-year period, the Invesco Senior Income Trust reported net realized losses of $42,147,690 that were almost perfectly offset by $42,842,426 in net unrealized gains. Overall, the fund’s net assets declined by $4,012,153 after accounting for all inflows and outflows.

Thus, it appears that this fund overdistributed during the full-year period. This appears to be a recurring problem for it, as its net assets also declined by $70,947,400 during the full-year period that ended on February 28, 2023, due to its net investment income falling short of the amount distributed.

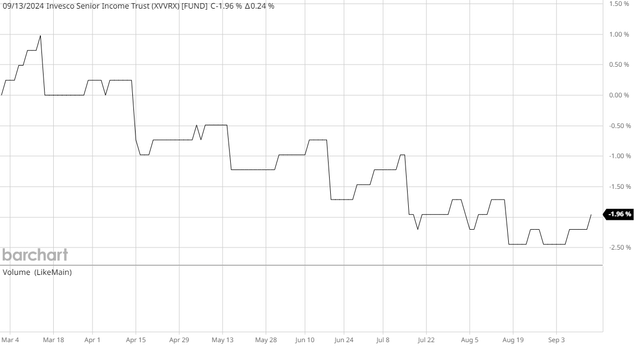

The fund’s net assets have been declining fairly consistently since the closing date of the most recent financial report. This chart shows the fund’s net asset value since February 29, 2024:

Barchart

As we can immediately see, the fund’s net asset value has declined by 1.96% since the start of the fund’s current fiscal year. This tells us that this fund continues to make distributions in excess of its actual investment profits. That is not sustainable over any sort of extended basis.

It seems almost certain that the Invesco Senior Income Trust will have to cut its distribution in the very near future. The fund is paying out more than it earns today, and its income will start declining once the Federal Reserve starts cutting interest rates. That will make the distribution even more sustainable and almost certainly force it to cut.

Valuation

The Invesco Senior Income Trust currently trades at a 9.00% premium on net asset value. This is substantially higher than the 7.77% premium that the shares have been averaging over the past year.

There is no reason at all to purchase this fund at a premium, and there could be a very good argument for selling it right now given this price. First, the fund is almost certainly going to have to cut its distribution in the near future due to the very high probability that the Federal Reserve will cut interest rates at its meeting later this week. Furthermore, the fund will probably have to cut even if the Federal Reserve does not cut interest rates because it is overdistributing and destroying its net asset value. With these fundamentals, it is probably best to take the profits that the fund has delivered over the past year and then evaluate the fund again after the distribution cut.

Conclusion

In conclusion, the Invesco Senior Income Trust is one of the few assets that has done extremely well ever since the current monetary tightening cycle began. However, it appears as though it will begin getting weaker going forward as a combination of falling investment income and net asset value destruction pressures the distribution. This fund’s shares have substantially outperformed the underlying portfolio and are now trading at a very large premium on net asset value. There is nothing here that justifies a large premium, and it seems likely that the shares will decline once the distribution cut is imposed.

Read the full article here