Introduction

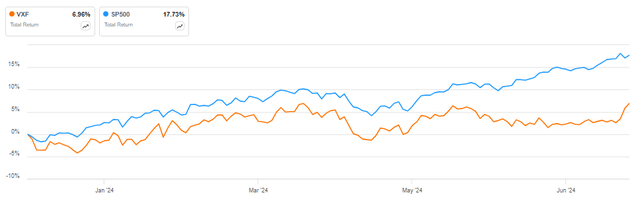

The Vanguard Extended Market Index Fund ETF (NYSEARCA:VXF) has lagged the SPDR S&P 500 ETF (SPY) so far in 2024, delivering a 7% total return against the almost 18% gain achieved by the S&P 500 ETF:

VXF vs SPY in 2024 (Seeking Alpha)

I think this has created a buying opportunity as VXF holdings trade at a cheaper valuation relative to large-cap peers. Furthermore, small-and-mid cap companies will likely benefit more from FED rate cuts compared to large-cap peers. Given the current valuation and future prospects, I expect the VXF to achieve a high single-digit return in the long term.

ETF Overview

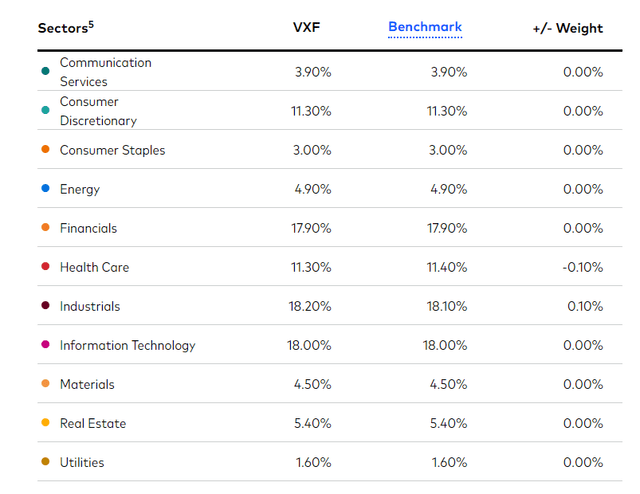

You can access all relevant VXF information on the Vanguard website here. The ETF tracks the investable U.S. stock market universe outside the S&P 500 index, which is why the median market capitalization of VXF holdings is $7.1 billion, well below the $35.3 billion median market capitalization of S&P 500 constituents. VXF’s portfolio of small and medium capitalization stocks is allocated primarily in Industrials (18.2% of net assets), Information Technology (18%), and Financials (17.9%):

Portfolio allocation across sectors (Vanguard website (Accessed July 2024))

The Vanguard Extended Market Index Fund ETF invests in 3 568 separate stocks, implying that the portfolio is exceptionally well diversified, with the top 10 holdings accounting for just 7.43% of all fund net assets.

Holdings valuation

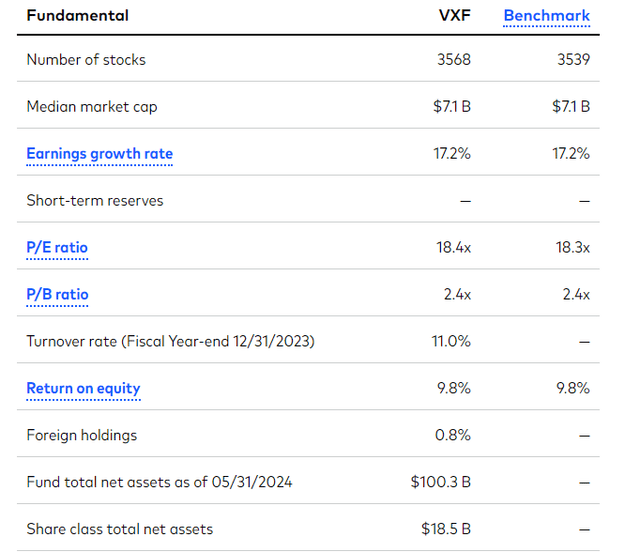

The Vanguard website reports a P/E ratio of 18.4 for VXF holdings, below the 23.24 reported by State Street for SPY. Likewise, the P/B ratio stands at 2.4 for VXF holdings, versus 4.79 for SPY holdings. While I would make the caveat that Vanguard data is from May 2024 while State Street data is from July, clearly small caps trade at a significant valuation discount relative to large-cap peers.

Portfolio characteristics and valuation (Vanguard website (Accessed July 2024))

Future Federal Reserve Policy

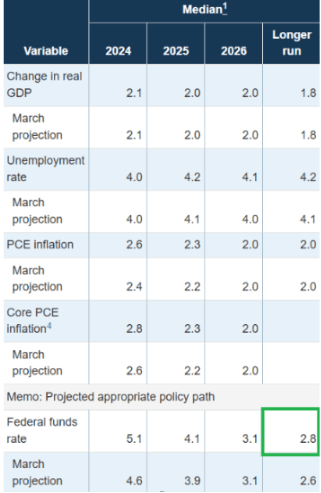

Futures pricing indicates the FED is likely to bring rates to 3.75-4.00% in July 2025, 1.5% lower than current levels. Furthermore, in its June 2024 summary of economic projections, FED officials signaled they expect further cuts post 2025, to a level of about 2.8% in the long term:

Outlook for macroeconomic indicators (Federal Reserve June 2024 Summary of economic projections)

These rate cuts will be highly positive for small and medium-cap companies since:

- They tend to have more floating rate debt compared to large caps (since they rely more on bank financing).

- They tend to have more debt-financed capital structures overall (in contrast to the cash piles held at many large caps).

These benefits will be partially offset by the 17.9% allocation the ETF has to financial stocks, which will be a net loser from lower rates. Nevertheless, for VXF as a whole, lower rates will be a net positive.

Distributions and expenses

The fund distributes quarterly dividends, though the current dividend yield is quite low, at only 1.25%. The expense ratio however is exceptional, at only 0.06% – a negligible amount for such broad portfolio diversification. Hence if you want a small and medium-cap portfolio allocation without much hassle, VXF is the ETF for you.

Risks

The main risk I would highlight for VXF is that small caps tend to be more exposed to economic dynamics in the United States, while large caps derive a greater proportion of their revenue from overseas. As such, if the unemployment rate keeps increasing (the June U.S. jobs report paints a nuanced picture of the U.S. labor market, with strong payroll gains offset by a jump in the unemployment rate to 4.1%, the highest reading since November 2021) small caps would bear the brunt of the economic damage.

The other risk to highlight is that with such broad diversification, across over 3 500 stocks, it is hard to understand what are the underlying dynamics driving returns of the portfolio. Thus if you prefer to know, at least to some extent, what factors are affecting your returns, perhaps VXF is not the ETF for you.

Long term prospects

As already mentioned above, it is impossible to generalize what are the trends driving such a diverse array of companies as the one held by VXF. Nevertheless, a good starting point to consider would be:

- The earnings yield of about 5.43%.

- The 3.8% long-term nominal GDP growth forecast by the FED.

- The return on equity of VXF holdings of 9.8%.

- The payout ratio of 23%.

I think investors can still expect a high single-digit return, driven by the combination of the 5.43% earnings yield and the 3.8% nominal GDP growth, topped up by a one-off benefit from FED rate cuts as floating rate debt becomes cheaper.

An alternative way to arrive at a similar conclusion is to use the dividend growth rate. VXF’s dividend may grow at about 7.5% annually – the combination of a low payout ratio, a modest return on equity, and a negligible expense ratio. Combined with the current 1.25% yield, investors are again set to receive a high single-digit return.

Conclusion

The Vanguard Extended Market Index Fund ETF has underperformed the broader market as measured by the S&P 500 so far in 2024. This has increased the valuation discount small-and-medium-cap companies trade at relative to large-cap peers. Furthermore, future Federal Reserve policy easing is likely to benefit VXF holdings more compared to large-cap peers. With a high-single-digit return prospect and exceptional diversification, I think the outlook for VXF is bright. Hence I recommend going long the ETF.

Thank you for reading.

Read the full article here