November last year, I wrote an article on Vanguard High Dividend Yield ETF (NYSEARCA:VYM) making a case to avoid investing in this ETF. The reason was simple – elevated risk of incurring an unpleasant opportunity cost by deploying capital into this specific vehicle.

What I mean by opportunity cost is an insufficient yield spread relative to the S&P 500 to compensate investors for de-emphasizing growth names. On top of this, there is also an element of an increased risk that stems from introducing a more pronounced tilt towards higher yielding stocks.

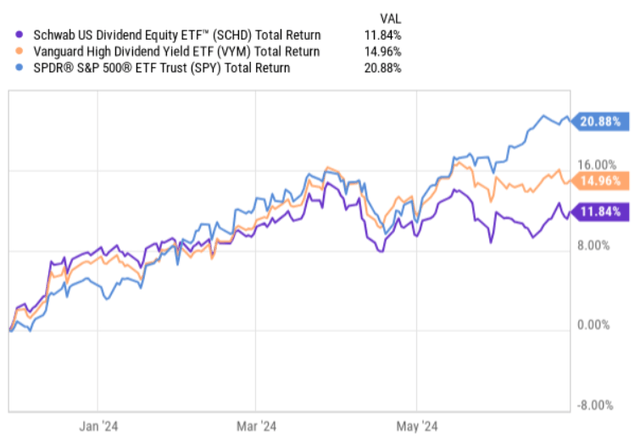

However, since the publication of my article, VYM has delivered rather solid returns, outperforming a widely popular ETF – Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD) -, which has an opposite strategy as VYM (i.e., growth and not yield focused).

Ycharts

Yet, compared to the S&P 500 itself both VYM and SCHD have lagged behind by a relatively decent margin.

With this in mind seeing that VYM has managed to register quite acceptable returns and also taking into account several changes the overall market conditions, let’s review the thesis to determine whether VYM has become a more enticing ETF to consider.

Thesis review

All in all, while VYM has indeed demonstrated a solid performance, I still do not see a justified rationale to invest in this ETF. There are three major points I would like to emphasize in this context.

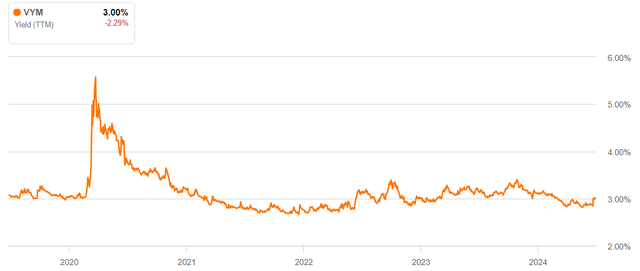

First, if we look at the yield spread between, for example, VYM and SCHD it has turned negative of ~ 60 basis points. Namely, the growth oriented SCHD, which invests in robust businesses that embody strong growth potential currently yields 3.6%, whereas VYM, which is inherently a high yield focused ETF provides only 3% in yield.

In addition to this, the prevailing dividend yield of VYM is almost in line with its 5-year historical average (adjusted for the temporary surge during the early moments of COVID-19).

Seeking Alpha

Given that the interest rates are now materially higher than before 2022 rendering the yields of many high quality names way more attractive, accepting a 3% yield through an ETF, which per design is meant to capture abnormal dividend streams, while not losing the focus on large cap names seems as suboptimal choice.

Second, and this is somewhat of an expansion of the previous comparison to SCHD, we have to understand that by entering into VYM, an element of opportunity cost comes into play. I would divide this into two categories:

- The overarching issue is that there are just too many high quality and higher yielding alternatives out there. For example, depending on the maturity segment we focus on, investing in risk-free rate instruments investors can access much more predictable yields that offer more attractive current income streams of around 120 – 220 basis points.

- The more specific issue is related also to the foregone potential in relation to the underlying dividend growth. Theoretically, one could make an argument that it is worth investing in VYM (and sacrifice some yield) since it provides growing distributions that over time can compensate the investors. However, the historical 5-year or even 10-year dividend CAGR of VYM is only at ~6%, whereas for SCHD (which currently offers higher yield) the relevant figure stands at roughly 12%.

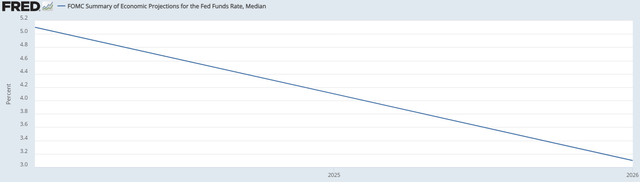

Third, the interest rate outlook has become increasingly more uncertain than compared to the time when my article was issued. Back then, the market had a strong conviction that there will be at least several interest rate cuts in 2024 that would quickly reduce the financing costs and thus relax the pressure on the cash flows of capital intensive businesses. Now we are talking about one or two cuts this year that would then be followed by additional ones in 2025, thereby gradually bringing the overall interest rate level to ~ 3% territory.

FOMC; St. Louis Fed

However, we should take these projections with a grain of salt and appreciate the probability that we will not experience such a normalization in interest rates any time soon (or that it will take place slower than what is currently baked into the cake).

For VYM these kind of dynamics do not bode well.

The major reason is that VMY is heavily tilted towards capital intensive businesses that carry notable amounts of debt on their books without having that significant growth factor in place. This could be easily implied by the fact that there is only 11.7% exposure to technology names, and that the Top 10 is mostly dominated by established pharma, energy and financial companies.

The bottom line

In a nutshell, VYM still remains a suboptimal investment choice that is mostly explained by the lack of clear advantage that would come from being invested in this ETF.

Theoretically, VYM is structured to put a heavier emphasis on high yielding dividend names without stepping out of the S&P 500 universe. The logic tells that the dividend that investors could access here should be relatively attractive, especially considering the significantly reduced exposure towards high growth technology names.

Yet, the actual situation is that the dividend offered by VYM is far from being enticing and even lower than growth focused ETF vehicles like SCHD provide. On top of this, the bias towards value and relatively higher yielding names within the S&P 500 space comes with a meaningful opportunity cost of not being able to participate in the upside that would potentially be driven by the S&P 500 growth oriented companies.

As a result of this, I still do not see a justified basis for going long Vanguard High Dividend Yield ETF.

Read the full article here