The banking sector has recovered overall after the early 2023 meltdown, but there are still some banks in clear trouble. Washington Trust (NASDAQ:WASH) is certainly among them; in fact, the stock is far from SVB’s pre-bankruptcy levels.

The current dividend yield is well above 8%, and dividend-hunting investors are wondering whether this is a good opportunity or not. After all, this bank has demonstrated a good track record in terms of dividend issuance over the past decades.

In my opinion, the answer to this question is rather complex, as there are several variables to take into account, some of which do not depend on management’s performance.

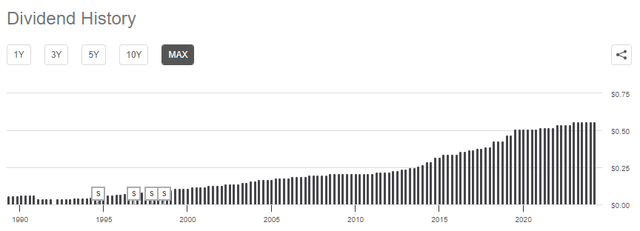

Brief summary of WASH dividend history

WASH is one of the oldest banks in the United States; in fact, it was founded back in the very distant 1800s. Without going too far into the data, it has proven to be a reliable bank in recent decades at least from a dividend standpoint; as for capital appreciation, there has been none since the current price per share is the same as it was 20 years ago.

Seeking Alpha

Returning to the dividend characteristics, we can note a number of interesting aspects:

- The first is that WASH has been paying a dividend for 30 years in a row.

- The second is that since Q1 1992 it has never cut the dividend, which is quite surprising. In times of distress, as happened during Covid-19 and the great financial crisis, management suspended dividend growth but did not cut it.

This is certainly a positive factor, however, thinking that the future will necessarily be like the past may prove to be a mistake. In the case of New York Community Bancorp, the unexpected dividend cut resulted in a strong feeling of distrust from investors, and a similar situation could occur with WASH.

Even though this bank has two centuries of history and has faced any financial crisis, it does not mean that it will once again be able to keep the dividend intact. As of today, we cannot say that we are in a recession, after all, the labor market is strong and consumption is not depressed, but the sudden change in the macroeconomic environment is generating cracks in the financial system. In the case of WASH, they are more evident than in other banks, and high interest rates are weakening its soundness.

Since the price per share is still depressed, I don’t doubt that the market has already discounted a negative scenario for this bank, but I don’t think the same applies to a dividend cut. Currently, there are no conditions for this to happen, but we cannot rule it out in the coming quarters.

WASH’s difficulties

Such a high dividend yield is anomalous, which is why it needs to be carefully analyzed. To assume that the dividend will not be cut just because that is how it has been since 1992 is frivolous reasoning that can be easily disproved. There is a reason this bank is cheap today, and it is mainly due to declining profitability, as well as a rather limited scope of operations.

Washington Trust Bancorp, Inc. (WASH) Q1 2024 Earnings Call

From Q1 2023 to the present, both net interest margin and ROE have deteriorated quarter by quarter, and it is likely that this trend may continue.

Washington Trust Bancorp, Inc. (WASH) Q1 2024 Earnings Call

Due to high money market yields, non-interest-bearing deposits continue to be replaced by expensive interest-bearing deposits. At the same time, on the asset side, there is no significant improvement since the demand for credit is not the same as it was a few years ago. But there is more.

Even if demand were thriving, WASH still could not meet it since the current Loan to Deposit ratio is 106%. The room for maneuver is very narrow, and until there is a boost in deposits, the bank cannot issue a significant amount of new loans.

Washington Trust Bancorp, Inc. (WASH) Q1 2024 Earnings Call

As you can see, total loans have virtually stalled since late 2023, and the only hint of growth comes from commercial real estate loans. In any case, the latter represents a risky option as commercial property prices are struggling.

In short, total assets are static and deposits continue to be increasingly expensive.

We think it’s been our number one priority for as long as I’ve been here. It continues to be our number one priority to get our funding mix better. And so everyone, including all the commercial lenders, are focused more on deposit gathering than they are on lending. Our cash management team is focused even more on commercial cash management, but also our municipal group within the cash management team are focused on growing our municipal deposits.

We want to grow the deposit base. And, I think from an expectation standpoint, we’re basically flat so far this year. I think 1% or 2% growth would be a great target for the year, but we’ve got much bigger hopes than that in the long run. We really need to turn the funding of the company more towards deposits away from borrowed funds.

CEO Ned Handy

Given the CEO’s words during the last conference call, I think management is aware of the situation and is working to improve it, but it is clear that things are not going as planned. Certainly, a few underwhelming quarters is not enough to put the dividend in question, but if profitability deteriorates further we could not rule it out.

Seeking Alpha

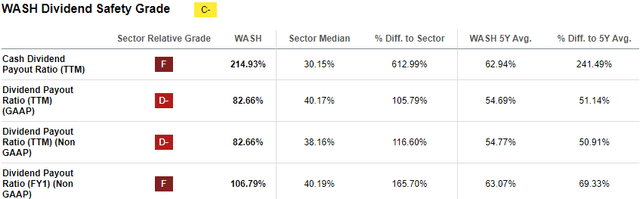

The data speak for themselves, and the Dividend Payout Ratio is heading toward 100%; this threshold has already been exceeded for Non-GAAP data. The average for the past 5 years is significantly lower, which signals how quickly the situation is worsening.

Washington Trust Bancorp, Inc. (WASH) Q1 2024 Earnings Call

In addition, Capital Ratios are among the lowest in the banking sector: the CET1 is only 10.42% and does not consider unrealized losses amounting to 24% of equity. WASH cannot last long with a Payout Ratio above 100%. Otherwise, it would risk taking its Capital Ratios to dangerously low levels. Since no improvement is expected in the short term, there is a risk that this could happen.

Regardless, at least for the time being, cutting the dividend to preserve capital is not a viable option for management:

So I would say that we consider the dividend to be a key component of our shareholder return. We don’t believe that the current level of revenue is permanent. We do believe that revenues will recover at some point. We probably need some help with interest rates and no one knows what the timing of that would be. If we were to cut the dividend, that would really have a very modest impact on capital accretion in my view. We do have the earnings and the capital to sustain the dividend and our intention is to maintain the dividend.

CFO Ron Ohsberg

In other words, the money saved from the dividend would not change the situation much and the current difficulties should be temporary. If so, the choice not to cut the dividend would be correct, but I would urge investors to think about how dependent this bank is on a variable it cannot control, namely interest rates.

In the case of a higher-for-longer scenario, this bank will continue to suffer, and I doubt it will be able to sustain the dividend. The leeway would be really tight because of the high Loan to Deposit ratio, as well as a lower degree of capitalization than peers.

CDs’ maturities are quite short, which will encourage rapid refinancing at a lower rate once the Fed Funds Rate is reduced. At that point, the actual recovery of WASH will begin, but we do not know when this will happen. Much will depend on inflation and not on management. The more time that passes without cuts, the more complicated the situation becomes.

On the other hand, assuming a quick rate cut, I would not be so sure that WASH would benefit. Typically, when that happens, it is a signal that something is broken in the economy and that recession is upon us. In a sense, to invest in this bank, you have to support the “no landing” scenario or at most the “soft landing” scenario.

Conclusion

WASH is a secular bank based in Rhode Island and is experiencing a time of great stress. A series of issues have followed since the Fed Funds Rate increased and are still weakening the financial structure today.

Since the dividend is dependent on the Fed’s monetary policy choices, I personally am not interested in investing in this bank. The risk factor is too high for me, and if there is a dividend cut, I expect a strong negative reaction from the market. History is on WASH’s side, but the future looks complicated.

The only reason I don’t consider this bank a sell is because it is currently quite cheap compared to its historical values: the Price/TBV per share is 1.12x, the 10-year average is 2.08x. It is difficult to assume that it will collapse further in the short term, but I also do not see the conditions for it to regain lost ground. There is too much uncertainty, and the Fed’s words will probably count more than those of management itself.

Read the full article here