Investment thesis

Our current investment thesis is:

- WOSG has a strong market position in the UK and US, with an unrivaled range of brands and national reach through its various boutique brands.

- The watch industry has become more lucrative in recent years, as watches are increasingly seen as investments. With strong demand for Rolex and Patek, WOSG is using this to drive greater sales in its other brands and Jewelry. Although the industry has faced a sharp correction, we expect a continuation of this long term.

- Despite the current economic conditions, WOSG’s growth has been respectable, supporting the resilience and attractiveness of its business model.

- The company’s share price has corrected and is now trading at an FCF yield of 6%, implying a good entry point in our view.

Company description

Watches of Switzerland Group (OTCPK:WOSGF) is a leading luxury watch retailer with operations in the UK and the US. The company offers a wide range of high-end timepieces, jewelry, and associated services.

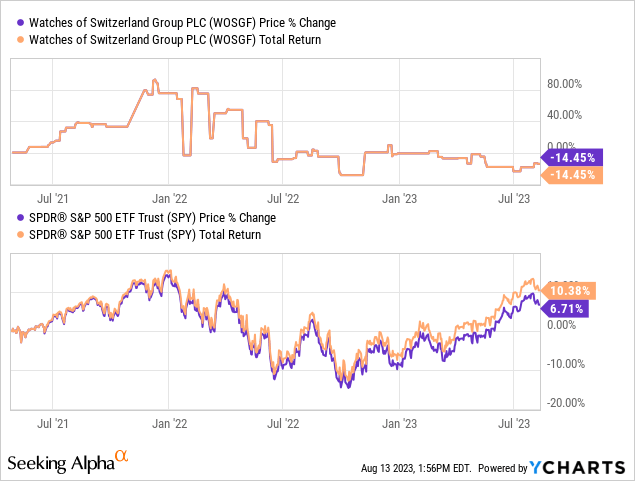

Share price

WOSG’s share price performance has been poor in the last few years, partially due to the timing of its listing, contributing to a small decline. The market was relatively volatile during this period.

Financial analysis

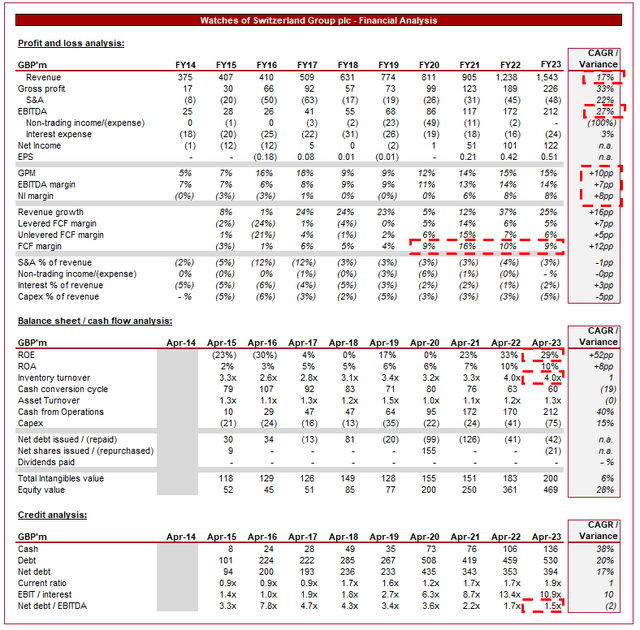

WOSG Financials (Capital IQ)

Presented above is WOSG’s financial performance.

Revenue & Commercial Factors

WOSG’s revenue growth has been incredibly strong since FY14, with a CAGR of 17%. This is unheard of within the retail industry given its maturity, with a supremely consistent YoY rate.

Business Model

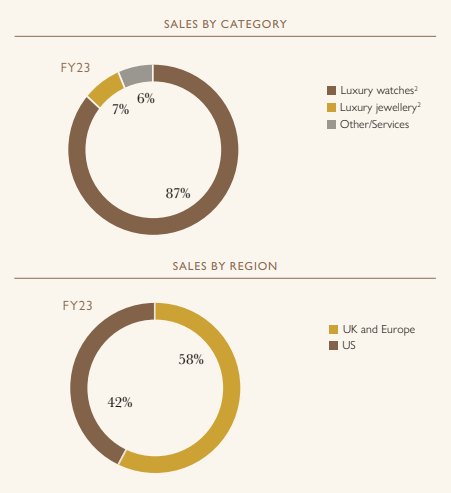

WOSG is focused on the retail of luxury watches (87% of revenue), primarily catering to customers seeking high-quality timepieces from renowned brands. The company operates both physical stores and an online platform to serve its customers. The company currently operates primarily in the UK and the US, with a relatively even split between the two markets.

Revenue profile (Watches of Switzerland Group)

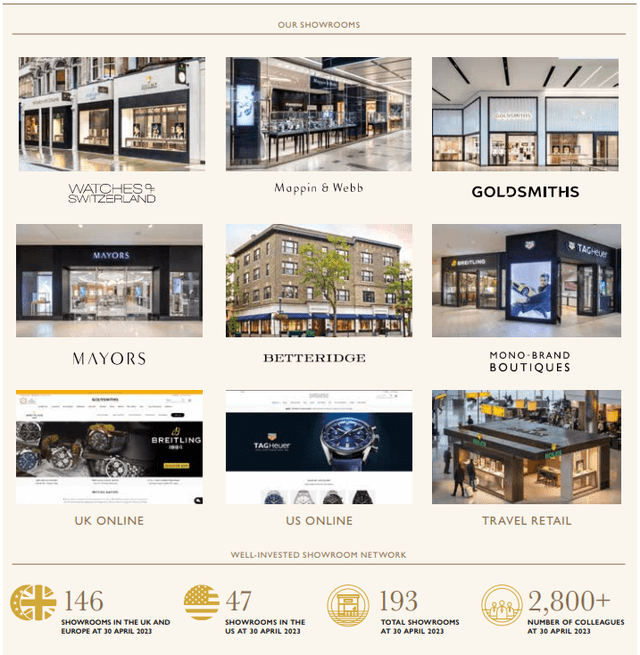

WOSG operates a number of sub-brands, including its namesake, Mappin and Webb, Goldsmiths, mono-brand boutiques, and travel-retail boutiques. This allows the business to operate across the value spectrum, by specializing its services and catering to a specific niche. As an example, Goldsmiths sells many “fashion watches” (sub <£500), as well as Jewelry.

Brands (Watches of Switzerland Group)

The group holds partnerships with a wide range of luxury watch brands, including Rolex, Patek Philippe, Omega (OTCPK:SWGAY), and more. These partnerships enable the company to offer an extensive selection of watches that cater to different customer preferences and price points. This is likely the biggest USP of the business, it has an almost unrivaled retail offering of luxury watches. This is to say, the vast majority of Patek Philippe and Rolex watches sold in the UK are through WOSG, and its only real competitors are small boutiques that lack national exposure (highly fragmented).

WOSG places emphasis on providing a premium in-store shopping experience. Its physical stores are designed to offer customers a luxurious and immersive environment where they can explore and try on watches, with the desire to create a longstanding relationship with clients that involve consistent purchases over an extended period.

Unlike many of its peers, WOSG has a well-developed online platform that allows customers to explore and purchase watches from the comfort of their homes. This digital presence widens its customer base and provides an additional sales channel. Given the luxury focus, the company is not materially under threat from the growth in e-commerce, as many will still prefer to enjoy the watch-buying experience. This said, for more affordable products, a quality online buying experience is critical to sales conversion.

Competitive Positioning

WOSG benefits from the reputation and prestige of the luxury watch/jewelry brands it carries. Further, it has a reputation for stocking the widest variety of luxury watches, increasing the chances that consumers will at least consider WOSG when looking for a luxury watch.

The luxury watch market attracts affluent consumers who value exclusivity, aesthetics, and craftsmanship. This is the most lucrative segment of the industry, as demand is generally more robust and less cyclical, as economic conditions have a far smaller financial impact. This is observed with the likes of LVMH (OTCPK:LVMHF), which has consistently grown while affordable retail begins(/continues) to struggle.

As disposable income rises and economic development continues in emerging markets, consumers will likely be more inclined to invest in high-end luxury goods like watches. This is specifically in the middle east, with significant demand for watches translating into a hot market in the UK, where many from the region regularly visit.

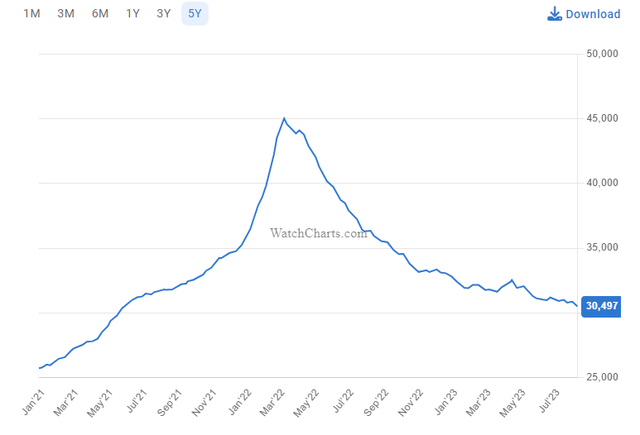

Many luxury watches are considered collectible items, with potential for value appreciation over time, particularly following the rapid increase in watch prices post-pandemic (see graph below). This aspect can attract investors and collectors to the group’s offerings, as well as encourage the purchase of less desirable brands due to the inability to get an allocation of the desirable models.

Grey market watch price index (WatchCharts)

The industry has significantly softened since the peak (of the madness) in 2022. This has primarily been due to a change in economic conditions. With rising interest rates and high inflation, the “everyday” consumer has experienced a decline in wealth, with many facing financial issues. This has inevitably contributed to a decline in demand. Wealthier individuals are being less aggressive with purchases given the rise in the cost of capital and the softening of price appreciation in the grey market, contributing to a negative price spiral.

Over the long term, however, we believe this will continue to contribute to strong demand. The reason for this is controlled supply. Brands such as Rolex and Patek are able to change supply based on demand, allowing them to maintain their reputation of exclusivity, keeping demand and grey-market prices strong. This will support the perception of watches as an investment and thus demand. WOSG will not face many issue selling all of the Rolex and Patek watches it gets, with strong demand across a range of other brands such as Omega, Tudor, Cartier, IWC, and JLC (OTCPK:CFRHF).

Margins

WOSG’s margins have been on a strong upward trajectory in the last decade, reaching an EBITDA-M of 14% and a NIM of 8%. Margin growth is likely to slow in the near term, as increased discounting will be required in order to generate sales. We consider the current level highly attractive when considered in conjunction with its attractive commercial profile.

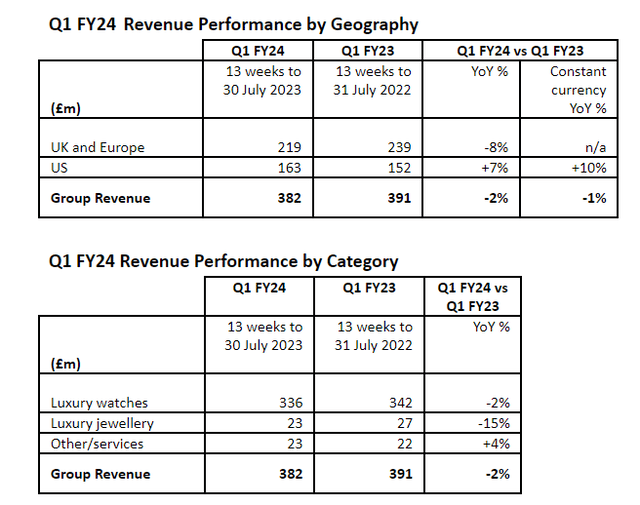

Q1 results

Q1 (WOSG)

Presented above is WOSG’s most recent quarterly results.

The key takeaways from Q1 are:

- Luxury watch sales (2)% to £336m, which given the economic conditions, is an impressive performance. Demand for luxury watches remains robust and continues to exceed supply, and importantly, average selling prices continues to increase.

- Luxury jewelry sales (15)%. This reflects reduced “cross-selling” ability due to the softening in the watch market. WOSG, and other retailers, will expect customers to purchase other products before being afforded the luxury of buying a Rolex or Patek. We believe jewelry will continue to struggle till the market reaches a normalized level.

- Expansion in the US continues, with new store openings and refurbishments.

- Ongoing improvement in airport business as traffic recovers.

- Successful launch of the “Rolex Certified Pre-Owned Programme” in the US, increasing the earning potential of the business by partaking in the grey-market success.

Balance sheet & Cash Flows

Inventory turnover has consistently increased, underpinning the strength of demand relative to supply. This has flatlined in 2023 but again, in the context of economic conditions, is a strong performance. Further, the business has brought its CCC down considerably, allowing for an impressive FCF margin.

Further, WOSG is conservatively financed, with a ND/EBITDA ratio of 1.5x. This positions the business well for debt-led growth is required, such as through the acquisition of boutiques/ retail brands. This is part of a critical long-term strategy in our view, as a growth opportunity following a slowdown in the expansion across the US is to target new markets and geographies.

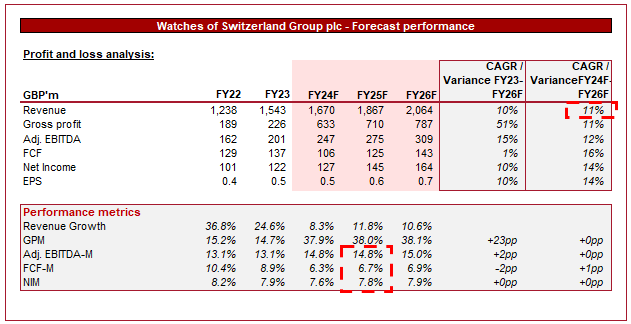

Outlook

Outlook (Capital IQ)

Presented above is Wall Street’s consensus view on the coming 5 years.

Analysts are forecasting a continuation of its strong growth trajectory, with a CAGR of 11% into FY25F. This is a reflection of its dominant (dare I say monopolistic) market position in conjunction with a resilient demand for watches.

Margins are forecast to improve further, an impressive achievement but reasonable in our view. We are more conservative with our assessment, expecting the improvement to be 1-2ppts into FY25.

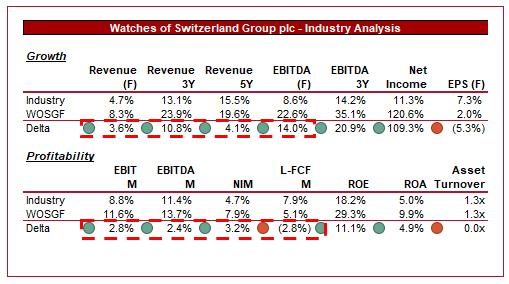

Industry analysis

Broadline retail industry (Seeking Alpha)

Presented above is a comparison of WOSG’s growth and profitability to the average of the Broadline Retail industry, as defined by Seeking Alpha (19 companies).

WOSG performs exceptionally well. The company has achieved consistently strong growth in revenue and profitability, in most metrics exceeding the industry average. This is forecast to continue into FY24. This is an impressive performance given it reflects high-growth and e-commerce/tech-enabled businesses.

Margins are significantly better, with a large ROA and NIM delta. This is enabled by a less cyclical revenue profile and a market-leading position in an industry where supply is not uniform (Rolex/Patek etc do not let anyone sell their watches).

Based on these factors, WOSG should trade at a premium to this peer group.

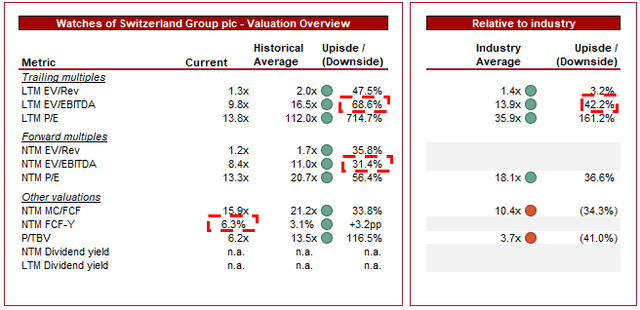

Valuation

Valuation (Capital IQ)

WOSG is currently trading at 10x LTM EBITDA and 8x NTM EBITDA. This is a discount to its historical average.

To a degree, a discount is warranted (mainly on an LTM basis). Primarily due to investors pricing in a continuation of aggressive growth, which has not been the case given the economic slowdown. This said, parity with its NTM average is reasonable in our view, given the first “proper” downturn WOSG has faced resulted in broadly resilient demand and strong relative growth (forward outperformance to peers).

Our view is that a premium to its peer group is justifiable, although this metric is impacted by some noise. This said, the broad discount is clear in the implication that WOSG is undervalued.

Based on both views, WOSG looks cheap. Confirming this for us is the company’s FCF yield, which is over 6%. This yield should theoretically translate to rapid shareholder returns through distributions over time.

M&A

We believe WOSG is a great takeover target for one of the large luxury retailers, namely LVMH or Richemont, for strategic reasons. The reason for this is to improve exposure to the watch industry whilst also increasing control. For this reason, margin dilution is less of a concern, and the reason we believe this is a possibility despite the margin delta.

What we believe is stopping this from occurring, and will likely do so in the next 5 years is the risks facing LVMH/Richemont with this acquisition currently. Richemont has seen its margins decline for most of the decade and has only just improved this. It is unlikely Management will be so foolhardy with dilution immediately.

In the case of LVMH, we believe it will want to own more brands before entering the retail industry. There have been many rumors of LVMH seeking acquisitions, including Patek, but thus far nothing has materialized. If LVMH was to acquire WOSG too early, there is a risk that its peers would pull their brands from WOSG, leaving the business in trouble.

Key risks with our thesis

The risks to our current thesis are:

- Rolex or Patek deciding to open their own stores and eliminating retailers. There is no indication this is happening but could wipe significant value from WOSG should this occur.

- Declining growth. Although demand has remained robust, it is not clear that this is sustainable if economic conditions remain difficult.

- FX. With an increasing US and Global presence, the business faces the risk of converting its earnings to Sterling.

Final thoughts

We are generally not a fan of retail. The industry is notorious highly competitive and difficult to develop a moat within. WOSG is slightly different. It has a strong portfolio of brands and it is almost impossible for new entrants to rival this. In conjunction with this, the business has the expertise and infrastructure to continue its expansion strategy, driving further growth.

Following a share price correction, the shares are trading at a NTM FCF yield of 6%, implying a good entry point in our view.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here