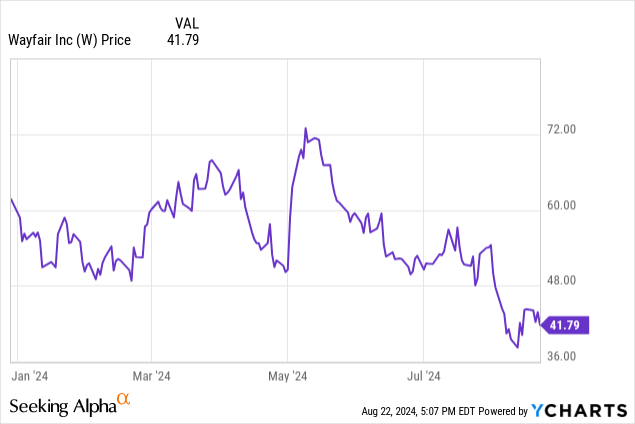

Now hovering in the low $40s, Wayfair (NYSE:W) is trading substantially below where the stock had been prior to the pandemic, which was a major growth catalyst for the company. At that time, buoyed by demand that took revenue growth to ~2x y/y, shares of Wayfair shot up promptly above $300, and in the intervening years since, we’ve seen billions in market cap wiped off this company.

And now, with the prospect of an S&P 500 that continues to ride near all-time highs, I’m keen to find contrarian value plays that have less correlation to the broader market, and Wayfair fits perfectly.

I last wrote a neutral opinion on Wayfair in May, when the stock was trading in the low $60s. Since then, after the company reported Q2 results, shares of Wayfair have crashed in the order of ~30%: which to me opens up a great buying opportunity. With this in mind, I’m upgrading my rating on Wayfair to a buy.

Long-term bull case drivers amid the current rut

Let’s be clear about one thing: Wayfair did raise our hopes earlier this year, only to dash them when Q2 results were printed. The company had initially noted, back in Q1, that Q2 was trending positively and that the company looked set for growth in the back half of the year.

We’ll discuss Q2 results in more detail in the next section, but the core takeaway is that while Wayfair’s “Way Day” performance in early May was solid (effectively the company’s equivalent of an Amazon Prime Day shopping holiday, full of discounts and offers), post-Way Day trends weakened, as a clear indicator that customers today are very deal-oriented and have very elastic demand.

But amid this weaker performance, the company noted that it has conducted a study of total spending over the past few years, including the pandemic period. Niraj Shah, Wayfair’s CEO, argued that cumulative spend is less than normal even after accounting for the demand pull-in to the COVID era, which has created an effective “backlog” of people needing to move and furnish new homes. Per his remarks on the Q2 earnings call:

We spent time trying to tease apart the magnitude of the demand pull forward in 2020 and 2021 in an effort to gauge how far along we might be in this period of rationalization. Controlling for inflation, we measured actual spending from 2020 through the first half of 2024 against a hypothetical environment where the pandemic never happened. Using data from the Census Bureau, the analysis shows actual spend volume coming in below that hypothetical no pandemic world.

I want to take a moment to let the magnitude of that sink in. Customers have more than compensated for the overspending during the pandemic and have now underspent in the category compared to historic patterns. This is in spite of the fact that the structural need for products in this category has not changed.

As we said many times in the past, people still need mattresses and tables and chairs. They still need desks and bathroom fixtures and kitchen equipment. And at some point, we expect a reversion to the mean. While we’ve yet to see the housing recovery, replacement for pandemic spending and broader economic upturn, we anticipate these drivers around the horizon. Given how deep we are into the cycle, it’s fair to expect the turnaround to come soon and Wayfair is well positioned to benefit as it does.”

For me, the core takeaway is this: a bullish bet on Wayfair is a bet that backlog on moving and furnishing homes will unwind and re-position this company for growth. Considering a number of tailwinds that may benefit the U.S. housing industry in the back half of this year (lower mortgage rates from coming rate cuts, clarity on the new real estate agency rules that took effect in August as an aftermath of the NAR lawsuit), I consider this is a reasonable bet to make.

Here, in my view, are the longer-term bull case drivers that support Wayfair:

- Furniture is an under penetrated category in e-commerce, and Wayfair is the clear leader in the space. With a multitude of brands from the eponymous Wayfair to higher-end labels like Birch Lane and Joss & Main to cater to all price points, Wayfair is well-positioned to distinguish itself from more generalist e-commerce titans like Walmart (WMT) and Amazon (AMZN).

- Logistics investments. Wayfair has spent much of the past three years improving its logistics network and reducing its freight costs, which has helped to improve its margin profile.

- Branching out into physical showrooms. Wayfair opened its very first retail store in Willamette, IL just recently in late May. While certainly a cost adder for a company that made its name in e-commerce, there’s a chance that having physical store outlets can legitimize Wayfair’s brand in consumers’ eyes, give it further distinction versus Amazon and help it compete with the likes of Home Goods and IKEA.

In my view, it’s finally time to buy here.

Q2 download

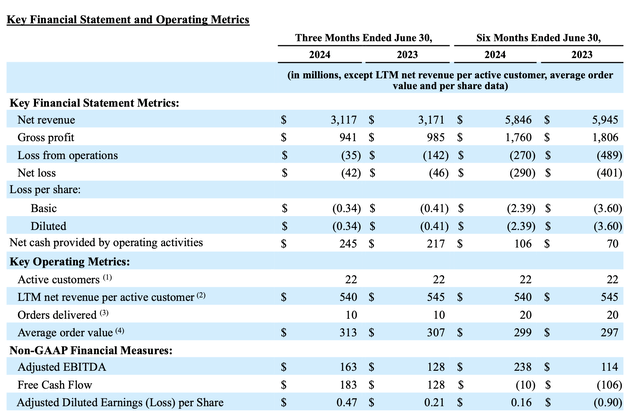

Let’s now go through Wayfair’s latest quarterly results in greater detail. The Q2 earnings summary is shown below:

Wayfair Q2 results (Wayfair Q2 shareholder letter)

Wayfair’s revenue declined -1.7% y/y to $3.11 billion, missing Wall Street’s expectations of $3.18 billion (flat y/y) by a rather wide mark. Again, the company had initially cited that it saw encouraging trends around Way Day in May, but it did not foresee a sharp deceleration in sales after Way Day as the promotions pulled in demand.

Interestingly, the company has picked up on a new sales trend. It noticed that while sales are incredibly strong during promotional peaks, only one-third of the items purchased during those promotional periods are actually on sale. Effectively, promotional windows create a “halo effect” that incentivize shoppers to check out Wayfair regardless of offer strength.

Now recognizing this, the company plans to invest in price over a multi-quarter period, hoping to draw in customers more frequently into the network which may yield sales for full-price items. The company is able to invest in pricing given structural fixed cost improvements, particularly on logistics, that it has achieved. More details on this new pricing strategy from CFO Kate Gulliver’s remarks on the Q2 earnings call:

The results from our price testing in combination with the bifurcation we see in promo versus non-promo periods, present a clear opportunity to optimize gross profit dollars by investing in price over a multi-quarter period. This follows the construct we laid out several quarters ago. Based on what we see today, we believe targeting a gross margin closer to 30% and — gives us the ability to drive higher order capture than a similar investment would have yielded a year ago. Through this strategy, we are maximizing gross profit dollars and driving order capture even if at a slightly lower gross margin. Absolute revenue growth will still be somewhat a function of the category at large. But our ability to take share dollars is very powerful right now and that’s something we aim to capitalize on.

We are comfortable leaning into this construct as we pair this margin investment with the considerable success we’ve had driving fixed cost efficiency in the business which we intend to sustain going forward. With the shifting consumer backdrop over the past several months, we actually began to lean into the price investment as we exited the second quarter and believe it makes sense to continue to do so in the back half of this year.”

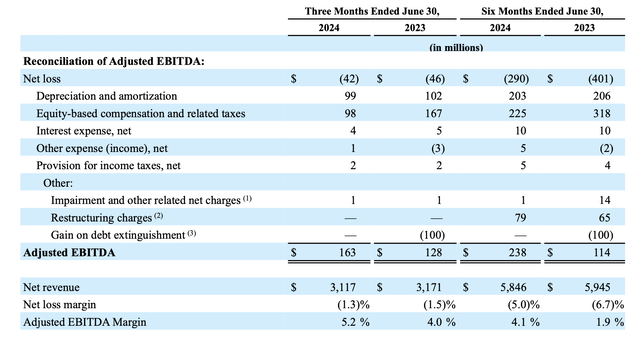

We note that in spite of revenue declines in Q2, the company hit a three-year record for nominal adjusted EBITDA dollars in Q2, which grew 27% y/y to $163 million. Adjusted EBITDA margins also gained 120bps of y/y leverage and landed at 5.2% for the quarter:

Wayfair adjusted EBITDA (Wayfair Q2 shareholder letter)

Valuation, risks, and key takeaways

At current share prices near $41, Wayfair trades at a market cap of $5.16 billion. After we net off the $1.34 billion of cash and $3.06 billion of debt on the company’s latest balance sheet, the company’s resulting enterprise value is $6.88 billion.

Meanwhile, for next year FY25, Wall Street analysts are expecting the company to generate $12.32 billion in revenue, or 4% y/y growth. If we assume the company can generate at least a 5.2% adjusted EBITDA margin on that revenue profile (conservative when we consider that this quarter’s 5.2% margin reflected heavier investments into Way Day promotions), adjusted EBITDA would be $641 million, putting Wayfair’s valuation at a reasonable 10.7x EV/FY25 adjusted EBITDA (note as well that at roughly ~0.5x next year’s revenue, Wayfair trades substantially below the ~1x revenue multiple it commanded in its pandemic heyday). Considering potential top-line tailwinds if the company’s prediction of a backlog in the housing/furniture industries prove correct, I’d consider this to be quite an opportunistic entry point when the S&P 500 continues to trade at multi-year P/E multiple records.

There are risks here, of course. The company’s plans to invest in more frequent promotional periods to drive traffic may start to impact gross margins if more of the company’s sales mix tilts toward discounted products. In addition, low housing supply and an unwillingness of homeowners to sell amid high interest rates may continue to depress home sales and movers, even if we get a percentage point or two of mortgage rate relief.

That being said, there are enough long-term bull case drivers here to support an entry point for Wayfair in the low $40s. Buy here and wait patiently for a rebound.

Read the full article here