Investment Summary

Founded in 1953, WD-40 Company (NASDAQ:WDFC) is renowned for its flagship product of the same name [WD-40]. The brand is a household name that’s attracted share of consumer mind for some 60+ years.

The modern company is as much a global marketing organization as it is a major product innovator. The company’s portfolio includes an extensive array of well-known brands such as WD-40, 1001, Lava, and Solvol [in Australia]. Currently, it moves its products via distribution channels tied to retail stores in the hardware, automotive and industrials domains.

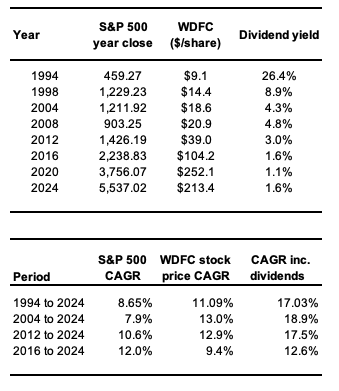

WDFC is a dividend aristocrat that’s unlocked tremendous value for its shareholders, despite being in a terminal growth cycle. The TSR is double-digits on each period measured including dividends. It has clearly offered benchmark advantages, ~60bps of alpha the last 8 years to date. Dividend growth of 14 years is above sector averages (Figure 2).

Figure 1.

Bloomberg, Seeking Alpha

Figure 2.

Seeking Alpha

Being it is this part of the cycle in its maturity, and paying dividends as long as it has been [including the growth and yields, as seen in Figure 1] – the embedded risk profile is inherently low in this business in my view (talking business here, not necessarily investment). It’s at a maturity cycle where 1) the predictability of sales growth is high, 2) reinvestment opportunities are low, and 3) the prospect for ongoing capital returns to shareholders is high.

WDFC displays abnormal persistence in the returns it produces on capital invested into operations. The fade rate of its ROIC to industry avg.’s is almost non-existent. In contrast, the fade rate of growth is high and there is little to growth expected in operating earnings to be expected in owning the business.

But WDFC has hit terminal growth, but not terminal value. Embedded risk is drastically reduced as 1) the growth fade rate is done, meaning 2) cash flows + earnings are buoyant, stable and highly predictable, meaning 3) the rate risk of negative investment return is lowered because there are no expectations of growth in the first place.

I am buy on WDFC for the following – 1) to establish a carry at current + future dividend yields, 2) its high-quality business franchise and superb economics [+20% ROICs, expanding FCFs, continued economic earnings], 3) valuations supportive to $233–$245/share, and 4) ~$20/share expected to FY’28, bringing the potential cumulative value to ~$250-$260/share.

Net-net, rate buy.

History of WD-40

I thought it would be interesting to run our readers through a brief history of the company’s namesake.

The name “WD-40” stands for “Water Displacement, 40th formula.” It reflects the creation process of the product: it was the 40th attempt by the inventing team to formulate a water displacement solution that effectively prevented rust and corrosion. Their persistence paid off when they finally achieved a formula that worked flawlessly.

WD-40’s first major use was a military application. It was designed to protect the outer skin of the Atlas Missile from rust and corrosion [the Atlas was a key component of the US’ intercontinental ballistic missile (“ICBM”) program during the Cold War]. The product of course proved to be highly effective, ensuring that the missile’s outer surface remained free from moisture-induced damage.

The success of WD-40 in the aerospace industry soon piqued the interest of other sectors. By the late 1950s, employees of the Rocket Chemical Company famously began sneaking cans of WD-40 out of the plant to use at home. They discovered that the product was not only effective for rust prevention but also worked wonders for a variety of household applications, from lubricating squeaky hinges to displacing moisture in electrical systems – the list is almost endless. As such, the rest is history.

High-quality business economics

Through my research findings, I have identified several high-quality business characteristics that WDFC possesses in its arsenal. These include the following:

- WDFC’s exceptional brand value gives it pricing power that mitigates the need to grow operating earnings. Sales have increased from $382 million in FY’14 on EBIT of $63 million, to $498 million in FY’18 with EBIT of $87 million, and printed $537 million in sales last year on $89.7 million of EBIT. This is 3.5% CAGR of both lines – thus, the 100% of sales growth has been passed through to pre-tax growth since FY’14.

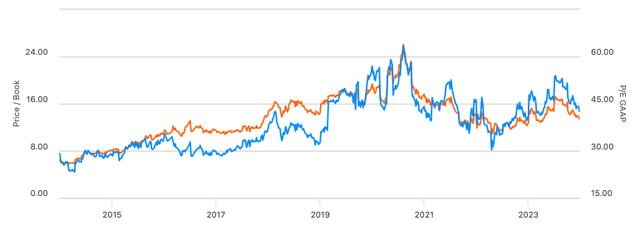

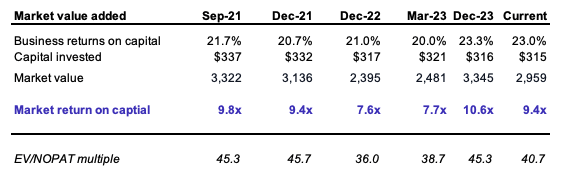

- The brand value of “WD-40” provides immense intangible economic value, measured in the >30x NOPAt and >9-10x EV/IC multiples WDFC has traded on since the 2010s. Investors are happy paying these prices [Figure 3, Figure 4]. Each $1 of capital is valued at ~$9-$10 by the market (market value added = 9-10x) illustrative of the highly intangible nature of the valuation [Buffett dubbed it “economic goodwill]. My opinion is investors will continue paying this spread.

Figure 3. Investors continue to pay >30 trailing earnings and >9x book value, evidence the company is ‘highly valued’. A 9-10x multiple on capital is rare, but indicates 1) its value, 2) exceptional returns on capital [discussed later], and 3) the expectations of these advantages to continue.

Seeking Alpha

Figure 4. Investors are valuing the company based on multiples of capital and earnings in my view.

Company filings, author

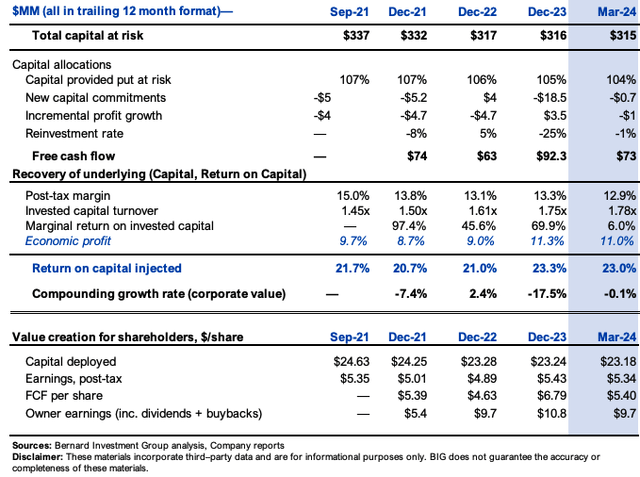

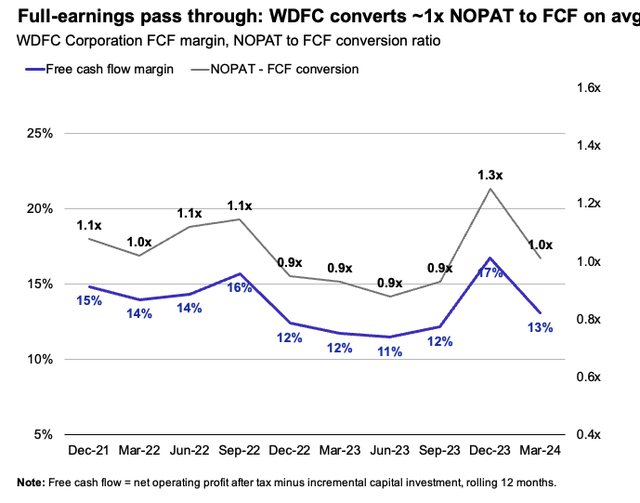

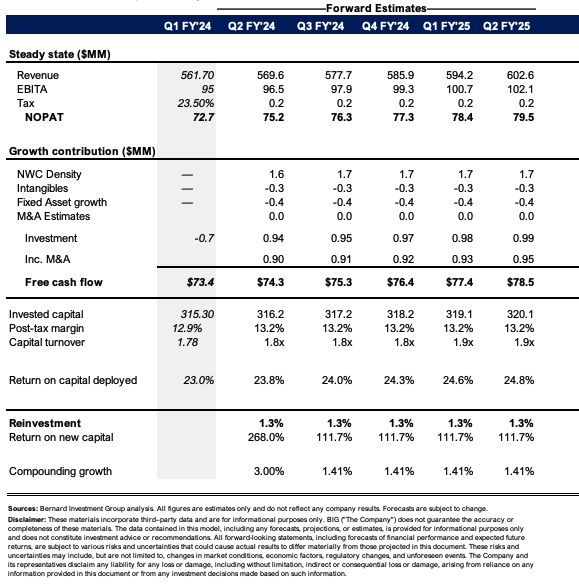

- WDFC requires almost no incremental capital requirements to maintain its competitive position. Growth is not a focus, as mentioned. Pricing power and stable operating leverage do the heavy lifting. Post-tax margins [~12-13%] combine with >1.5x capital turns to throw off >$0.20 in net operating profit after tax per $1 of capital employed in the business. This is clear evidence of the company’s durable competitive advantage that looks to be increasing [discussed later]. This means 1) the marginal returns on incremental investment avg. +50% since FY’21 [Figure 5], 2) returns on existing capital are +270 basis points since FY’21 to 23% in the TTM, and 3) management converts ~1x NOPAT to FCF every rolling 12 months (Figure 6).

- This ~1x pass-through funds dividends and the value is obvious – post-tax earnings of $5.34/share lifts to owner earnings of $9.70 share in Q2 FY’24 including all trailing dividends paid up.

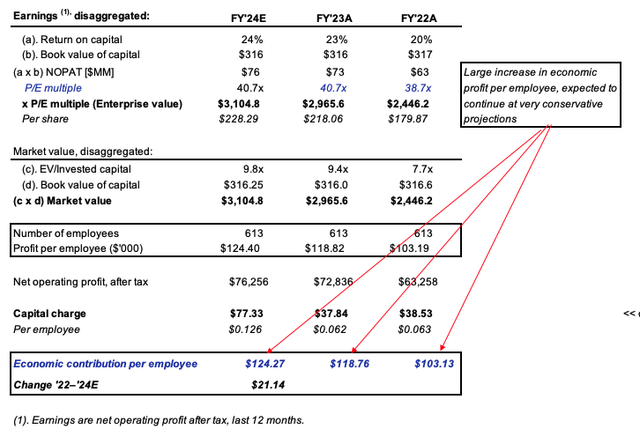

- Further, the business runs on just 613 employees, such that 1) economic profit per employee increased $15,630/employee from FY’22–’23, and 2) my estimates [see: Appendix 1] get me to an increase of $21,140/employee to $124,270 in FY’24, clear indication of the economic goodwill embedded in the 9-10x multiples. This is equal to $63K/$72.8K/$76.3K for FY’22A/FY’23A/FY’24E in NOPAT per employee, respectively (Figure 7).

Figure 5. Returns on business capital required to operate are abnormally high and persistent. This is clear evidence of its competitive advantages. Critically, 1) post-tax margins >12% and 2) capital turns >1.5x drive the returns. Management has achieved efficiencies since FY’21 increasing capital turns by ~0.33x [1.45–1.78x in the TTM]. This is due to (i) its “4×4” strategic framework, (ii) its acquisition of a Brazilian marketing distributor to grow ex-US sales, (iii) shift to a D2M model in Mexico driving~3x revenue growth there, and (iv) general sales growth thanks to pricing advantages in its core portfolio.

Company filings, author

Figure 6. Almost 100% of NOPAT passed through as dividends thanks to 1) >20% ROICs [and increasing], 2) >10% FCF margin [averaging closer to 12%], and 3) almost no incremental capital requirements required in the underlying business.

Company filings, author

Figure 7. The business runs on just over 600 employees driving profit/employee >$72,000, 3rd highest in the household products industry. It is increasing returns on 1) business capital, and 2) human capital.

Company filings, author

Fairly valued

I believe WDFC is fairly valued based on the facts of 1) it commands +9-10x EV/IC on a rolling basis [thus currently in range], 2) The +2.5 years increase in competitive advantage period (“CAP”) implied with its higher ROICs, 3) persistence in its abnormally high business returns, 4) reduced fade rate accompanying this, and 5) earnings stability.

Specifically, my opinion is the market has captured WDFC’s fundamentals well, and that an intrinsic valuation is supported to $233–$245/share.

Valuation insights

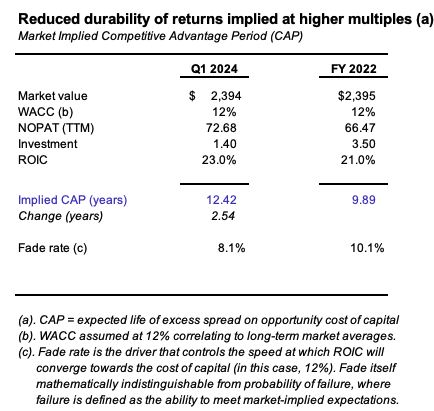

- WDFC now implies a CAP of >12.4 years following 1) +270bps in earnings produced on business capital, 2) double-digit marginal returns on incremental investment, and 3) pricing power in its WD-40 segment. On the Q2 earnings call, management said it “made the strategic decision to actively pursue the sale of our U.S. and UK home care and cleaning product portfolios“. This excludes AUS, where it has large market share. In my view, the divestments will 1) reduce capital employed further [increasing ROICs more], 2) remove sloppy, underperforming assets from the balance sheet, and 3) drive focus to higher-margin segments [thus >ROIC even further].

Figure 8. The CAP indicates the expected life of excess returns above an opportunity cost of capital [in this case = 12% for LT market averages]. The >CAP is supported by 1) the ROIC of 23% vs. ~21% in FY’22, and 2) the reduced implied fade rate of ROIC to the hurdle rate. As WDFC’s ROICs are so persistent, investors expect a ~8% exponential fade rate – i.e., for the 23% ROIC to gradually reduce to the hurdle rate at ~8%/year.

Author estimates

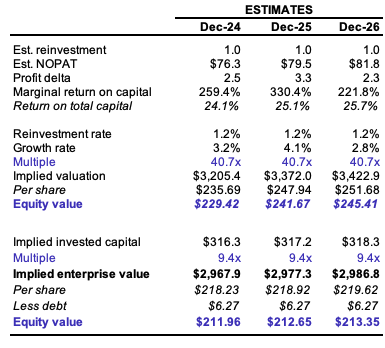

- My opinion is that 1) 9-10x EV/IC is a fair multiple [based on historical avg., >20% ROIC profile, dividend profile, and <5% reinvestment requirements], and 2) an EV/NOPAT multiple of ~40x is equally fair. On my FY’24–’26E estimates [see: Appendix 1] this gets me to $230/share today and ~$245/share by year 3 (Figure 9).

Figure 9. At 9.4x EV/IC estimates the stock is fairly valued today, but the $230-$245/above equates to 10.1-10.8x EV/IC anyway – in line with my band of 9-10x.

Author estimates

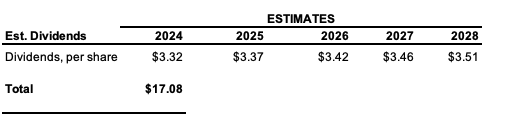

- Dividend payout is ~67% of NOPAT and this is +15 points since FY’21 as management maintains a >1-1.5% rolling yield (Figure 10). My view is ~60% payout is fair to carry forward on my projections getting me to ~$17/share in implied dividends out to FY’28 (Figure 11). The stability of growth enables me to establish a carry in this name, collecting 1) capital gains, and 2) a future stream of increasing dividends that are well supported by the fundamental economics.

Figure 10.

Company filings

Figure 11. Dividends maintained at a 60% payout get the following on forward estimates.

Author estimates

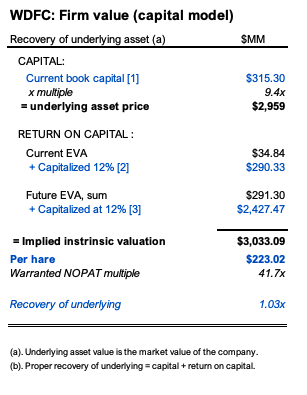

- Being that 1) growth has faded, and 2) cash flows are predictable, future economic profits (“EPs”) are likely in my view [EPs are returns on business capital >12% hurdle rate]. I identify ~$291 million in EPs from my projections getting me to ~$223/share in implied value indicating proper recovery of underlying through (i) capital and (ii) return on capital.

Figure 12. Forward estimates of 1) 1.4% compounding sales, growth, 2) ~17% pre-tax margin, 3) 22% tax rate, 4) each new $1 of sales produced by ~$0.11 of incremental investment get me to an EP stream of $291 million. Combined with (a) current book value, (b) current EP capitalized at 12%, and (c) the est. EP discounted at 12%, this suggests 1.03x recovery on our underlying asset price.

Author estimates

Risks

Downside risks include 1) sharp sales decline of >5% in FY’24, 2) large loss of market share due to product control issues [highly unlikely in my view], sudden increase of capital into the business, skewing the ROIC profile, and 3) any threat to the company’s dividend for the same. The future dividend stream is well supported in the economic data, but does form a large part of the thesis. Investors must know these risks in full before proceeding further.

In short

WDFC is a high-quality company that possesses excellent economic characteristics. The company’s dividend growth is well supported by 1) its abnormally high and persistent ROICs, 2) pricing power on its major labels, 3) minimal incremental capital requirements that see ~1x pass-through of NOPAT to FCF, and 4) Increased CAP that sees management return more capital to shareholders. My view is these trends are set to continue. Rate buy, eyeing price objectives to $245/share by FY’26E.

Appendix 1.

Author estimates

Read the full article here