Written by Nick Ackerman.

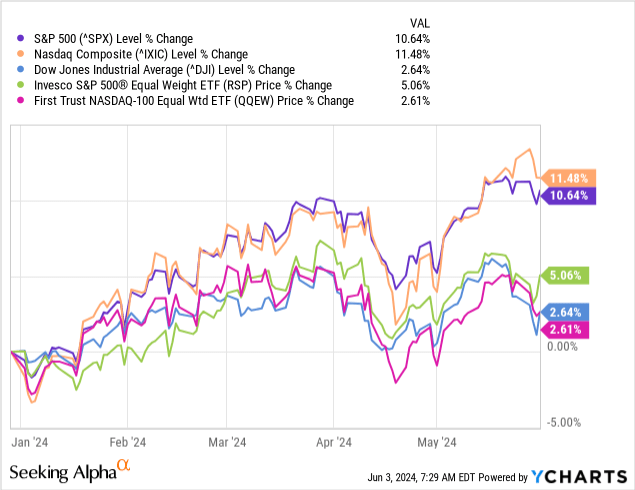

After a brief pullback in April, the market raced back higher and pushed into new high territory for May. This has helped the market, as measured by the S&P 500 Index, which is up double-digits this year, and the Nasdaq Composite Index, which is also up double-digits. Those two indexes have become heavy in technology stocks, more specifically the magnificent 7 names, which continue to drive the markets.

When compared against the Dow Jones Industrial Average and the S&P 500 Indexes’ equal-weighted counterpart ETF (RSP), we see more muted gains-though gains nonetheless.

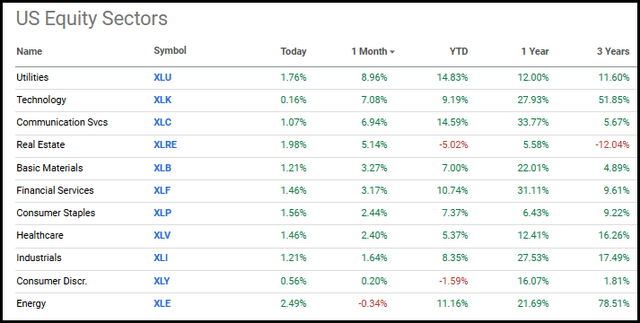

One area of the market that was a laggard was utilities, along with real estate. However, over the last month, utilities have climbed materially. They went from up 1.18% YTD-good for the third worst-performing sector-to up 14.83% YTD and are now the best-performing sector for 2024

U.S. Equity Sector Performance (Seeking Alpha)

Real estate also did well over the last month but has remained down slightly on a YTD basis. Over the last three years, the real estate sector is still negative as well.

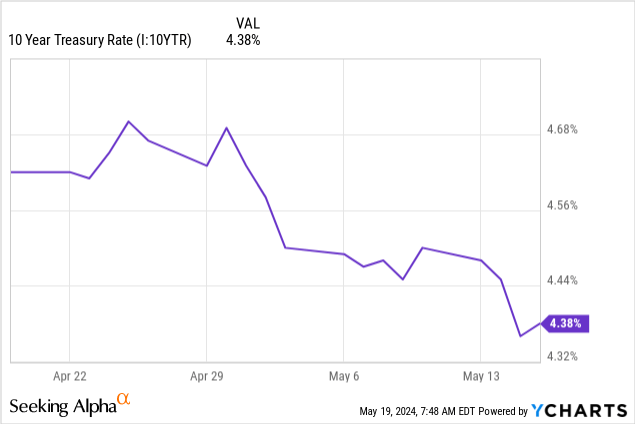

A driving factor for this was the decline in risk-free Treasury rates over the last month, which eased pressure on these interest rate-sensitive sectors. Utilities and real estate/REITs are sensitive to interest rates due to the significant amount of borrowings they utilize.

YCharts

Further, they compete as yield-oriented instruments for income-investor dollars. When risk-free rates can earn ~5%, taking higher risk in utility or REIT names isn’t worth it for some investors. When rates fall, and risk-free rates start to come down, these usually yield-rich companies’ shares start to look more competitive again.

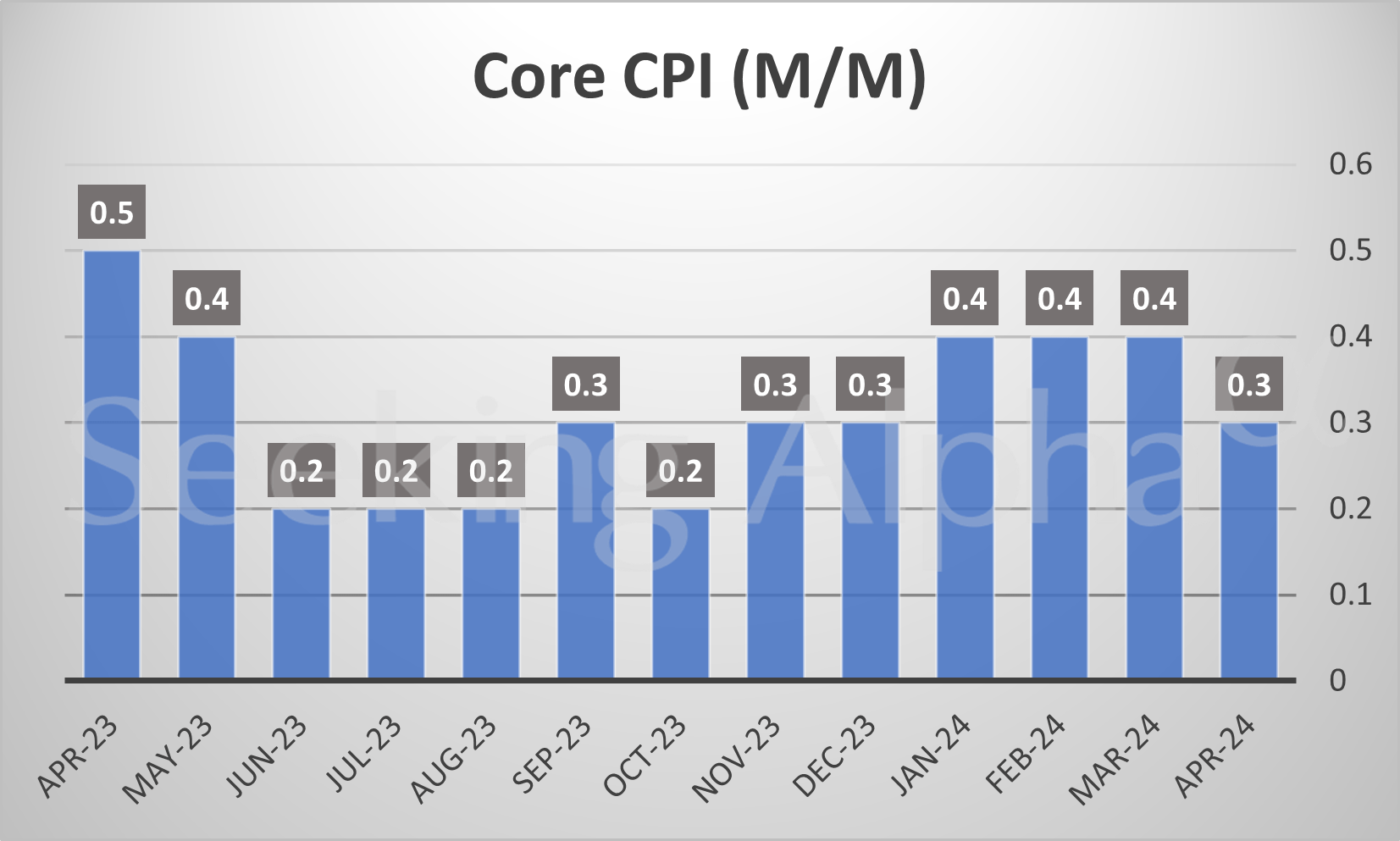

Of course, rates generally need a reason or a catalyst to move in meaningful ways. The risk-free rates retreated on evidence of inflation starting to cool after the last couple of months when it had been coming in hotter than expected.

Monthly Core CPI (Seeking Alpha)

Powell also suggested that he believes the next move in rates will be a cut and not an increase. However, he also mentioned that they intend to keep rates where they are at, in what they believe is restrictive territory, for longer-all depending on how the data unfolds going forward.

With utilities performing so well now, it’s time to take a look at my utility picks for 2024.

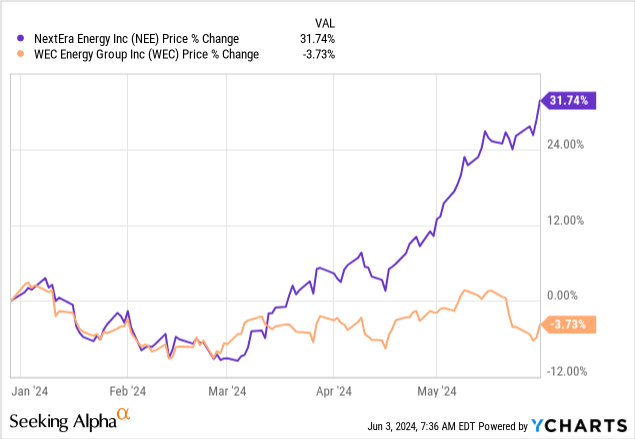

WEC Energy Group (NYSE:WEC) and NextEra Energy (NEE) were two of my four “top 2024 picks.” Though admittedly, I’ve held these names for years and plan to continue holding them for years. It was more that they had started to trade at bargain prices, making them exceptional opportunities.

Both sunk in the first few months of the year as risk-free rates rose and pressured these names. However, utilities surging in the last month have helped to lift these two to see higher share prices after that initial weakness.

That said, NEE has shown the most material climb on a YTD basis by a significant margin. WEC has seen a material lift in its share price from where it was earlier in the year. For price return only, though, it is down a touch for the year. In fact, it was one of the weaker utility performers in the last month when NEE continued to climb higher.

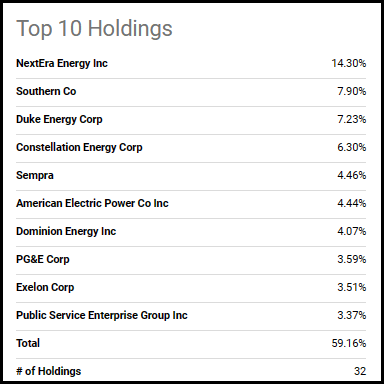

Seeing the utility sector surging as measured by the Utilities Select Sector SPDR (XLU) might not be too surprising after seeing NEE’s performance. This is because NEE comprises over 14% of the XLU ETF. As NEE goes, so goes XLU, for the most part.

XLU Top Ten Holdings (Seeking Alpha)

WEC Energy is also a holding in XLU, but is not a top-ten holding as WEC’s market cap comes in around $27 billion versus NEE’s ~$156 billion market cap. From some perspective, the second-largest holding, Southern Co (SO), has a market cap of ~$87 billion.

I believe these two are still attractively valued despite the latest increases and NEE’s surge. Of course, NEE just isn’t as exceptionally priced these days as it was at the start of the year. Both remain long-term candidates for an income-investor’s portfolio. Thanks to their growing dividends, that’s one of the selling points that risk-free Treasuries can’t offer investors.

WEC Energy

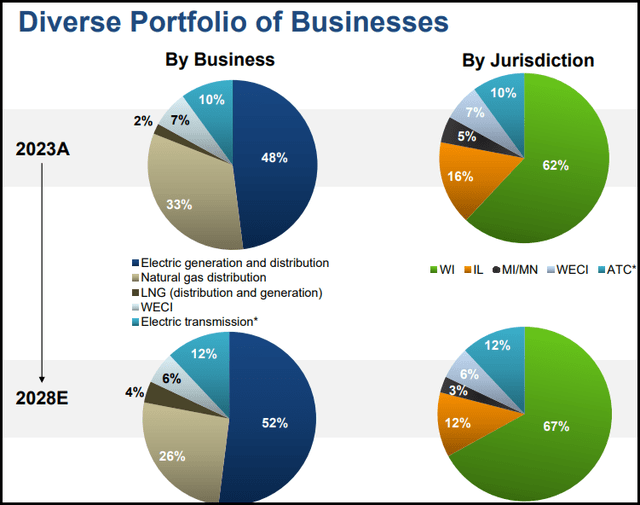

WEC is a multi-utility company in the midwestern United States with operations primarily in Wisconsin, Illinois, Minnesota, and Michigan. Wisconsin is by far the largest part of their business. Electric generation and distribution is also the most significant part of their business over natural gas. However, they plan to take that to an even larger portion of their business and also increase electric transmission over the coming years.

WEC Portfolio of Business (WEC Energy)

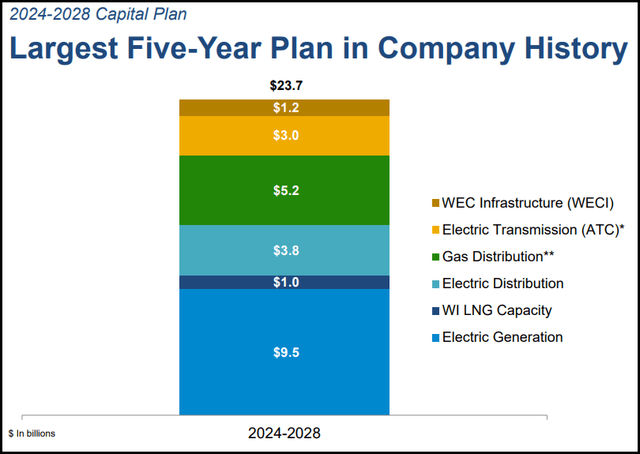

“WECI” is WEC Infrastructure, and “ATC” is the electric transmission.

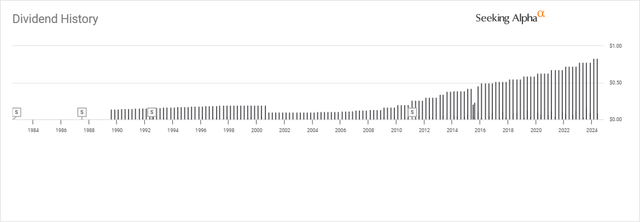

The company has delivered steady EPS growth for the last couple of decades, at an 8.7% EPS CAGR going back to 2004. That has also helped to push the dividend higher during this time. The latest dividend increase was good for a 7% bump-in line with the latest anticipated earnings growth. That increase also was the 21st consecutive annual increase that they have been able to deliver.

WEC Dividend History (Seeking Alpha)

In the early 2000s, they cut their dividend to focus on putting more capital into growth projects. That’s interesting to note because they haven’t had plans to cut their dividend again-at least not hinting at it as they continue to reiterate their dividend growth plans-despite noting that they are making the largest “five-year plan in company history” deploying capital into new projects.

WEC Capital Plan (WEC Energy)

To finance this capital plan, they will issue equity and take on some new debt.

The good news is that these growth projects are intended to hit their long-term EPS growth of 6.5 to 7%. That’s where we could expect dividends to grow over time, as we are in the range of their current dividend payout policy. Their policy is to pay between 65 and 70% of their earnings in dividends. Based on this year’s expected earnings, the payout ratio would be around 68.6%. The current dividend yield works out to 3.91%.

Based on the historical fair value range, WEC still looks like an enticing opportunity for income investors.

WEC Fair Value Range (Portfolio Insight)

NextEra Energy

NEE is an electric utility company based in Florida; it operates through several subsidiaries, and its claim to fame is that it is “a leading clean energy company.” Florida Power & Light Company is notable as America’s “largest electric utility,” with NextEra Energy Resources and its affiliated entities being “the world’s largest generator of renewable energy from the wind and sun and a world leader in battery storage.”

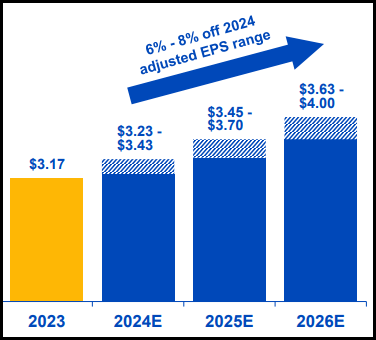

Similar to WEC, the company has been able to provide steady historical earnings growth, and it expects to continue to deliver 6 to 8% growth going forward, which is pretty much in line with what WEC is expecting.

NEE Earnings Estimates (NextEra Energy)

With this earnings growth, they anticipate being able to support a higher dividend. In fact, they expect to continue to grow the dividend by ~10% annually through “at least 2026.” Of course, it doesn’t take a rocket scientist to know that 10% is greater than 6 to 8%, and that would suggest that they anticipate seeing their dividend payout ratio climb a bit higher going forward.

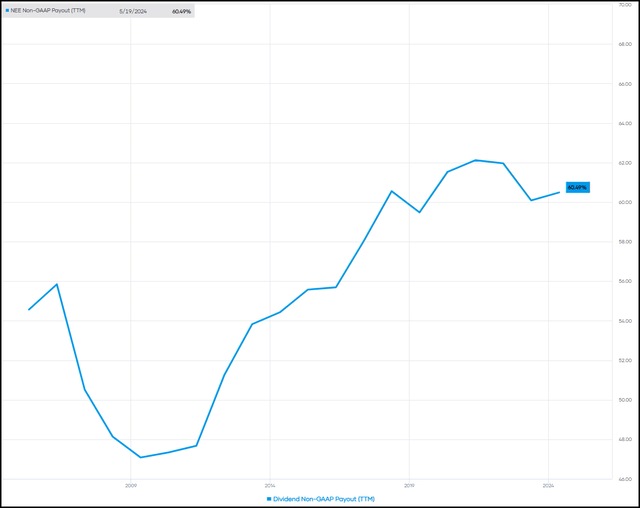

Based on the latest quarterly dividend and this year’s EPS estimates, they are sitting at a healthy 60.5%. That puts them in a situation where they can continue to invest in their underlying business and pay a generous, growing dividend to investors. The current dividend yield comes in at 2.71%.

NEE Non-GAAP Dividend Payout Ratio (Portfolio Insight)

Interestingly, NEE enjoys trading at a richer P/E multiple compared to WEC, even with their growth expectations being similar going forward. NEE has been able to deliver higher earnings growth historically, so this suggests that investors have to anticipate this continuing-where NEE is under-promising but going to overdeliver.

To be fair, that certainly can be the case, with Florida growing at a faster pace in terms of population relative to Wisconsin. According to the U.S. Census Bureau, Florida has seen the third-fastest population growth since 2020.

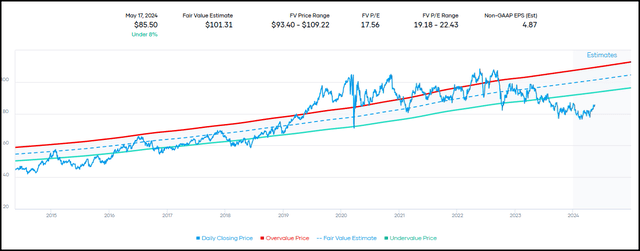

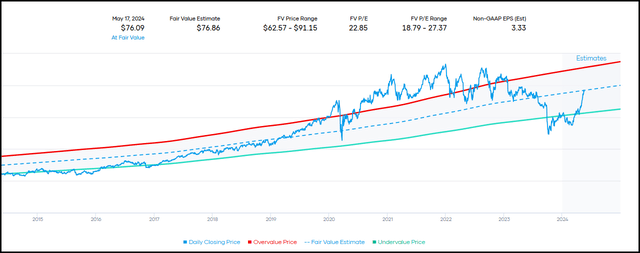

After the price surge in NEE, we are nearly exactly at the mid-point of the fair value range.

NEE Fair Value Range (Portfolio Insight)

That doesn’t mean that NEE isn’t a worthwhile holding, but being a bit more patient here could prove to be a wise move before investing anything significant in this name.

Read the full article here